Download

1 / 77

770 likes | 782 Views

COST ANALYSIS AND BEHAVIOUR. CONTENT. Introduction Meaning & Definition Analysis and Classification of Costs Methods and Techniques of Costing Cost sheet Cost Behavior Advantages of Classifying costs Activity B ased Costing Quality Costing Value Chain Analysis Target Costing

E N D

CONTENT • Introduction • Meaning & Definition • Analysis and Classification of Costs • Methods and Techniques of Costing • Cost sheet • Cost Behavior • Advantages of Classifying costs • Activity Based Costing • Quality Costing • Value Chain Analysis • Target Costing • Life Cycle Costing

INTRODUCTION The term cost has a wide variety of meaning. Different people use this term in different scenes for different purposes. In common use, the word cost means price. But for our purpose cost is not the same as price. In management terminology, the term cost refers to expenditures and not the price. It also refers to something that must be sacrificed to obtain a particular thing.

DEFINITIONS 1. According to terminology of BRITISH INSTITUTE OF COST AND WORKS ACCOUNTANTS, “cost is the amount of expenditure (actual or notional) incurred on or attributable to a given thing” 2. W. M. HARPER says, “cost is the value of economic resources used as a result of producing or doing the thing costed.” 3. In words of CHATFIELD AND NEILSON, “Business cost represents the value of economic resources that are sacrificed to obtain more desirable resources.”

MEANING We now know that meaning and concepts of costs is very broad and flexible. However, there are certain point which need consideration. The cost have also to be distinguished from expenses and losses. Cost refers that portion of the acquisition price of good, property or services which has been deferred or not yet utilized in connection with realization of revenue. Purchase price of fixed assets, material, supplies, etc. are such deferred cost.

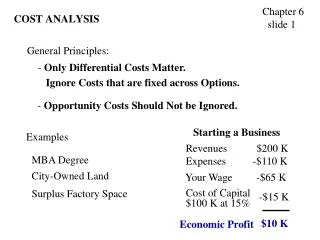

ANALYSIS & CLASSIFICATION OF COSTS In simple words we can say that costing is to ascertain the cost of each product, process, department, service or operation. The ascertainment of cost involves further the study, analysis and classification of costs such as prime cost, works cost, production cost, etc. Cost analysis refers to the break up of total cost into certain elements or sub-divisions. Such analysis is essential for the purpose of accounting and control over costs. Costs may be classified into different categories depending upon the purpose of their classification.

Some of the important basis of cost classification are as follow : • Classification by nature or element. • Functional Classification. • Classification on the basis of behavior. • Classification for managerial decisions and control.

DIRECT COST : Direct costs are the costs which can be conveniently identified with and allocated to a particular unit of final product. Such costs are treated as the cost of the unit produced.

Direct materials include all materials specifically purchased or requisitioned for specific cost unit. All material which become an integral part of the finished product and which can be conveniently assigned to specific physical units are called direct material. • Direct Labour cost consists of wages paid to worker directly engaged in manufacturing or handling a product, job or process. It includes payment of wages to worker engaged in actual production or an operation or an process; or helping such production by way of supervision, maintenance, etc. • All expenses other than the direct material or direct Labour that are specifically incurred for a particular job, product or process are called direct expenses.

INDIRECT COSTS : These are those costs which cannot b assigned to any particular cost unit, i.e., job product or process. Indirect costs are usually, incurred for the business as a whole and are, therefore, apportioned among the various cost units.

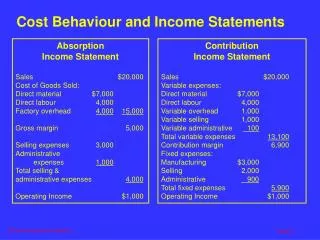

PRIME COST It consists of the costs of direct materials that go into the product, the costs of direct labour and direct expenses. It is also known as direct cost or first cost. • FACTORY COST It consists of prime cost plus factory overhead or work expenses or factory on cost. Factory cost is also known as works cost, production cost or manufacturing cost. Prime Cost = Direct Material + Direct Labour + Direct Expenses

COST OF PRODUCTION Also called office cost, administration cost or gross cost of production, it consists of factory cost plus office and administrative expenses. Office Cost Or Gross Cost Of Production = Factory Cost + Administrative And Office Overheads

TOTAL COST OR COST OF SALES It comprises cost of production plus selling and distribution overheads. Total Cost Or Cost Of Sales = Office Cost + Selling And Distribution Overheads

I. FIXED COSTS A fixed cost is a cost that does not change with an increase or decrease in the amount of goods or services produced or sold. Fixed costs are expenses that have to be paid by a company, independent of any business activity. It is one of the components of the total cost of running a business, along with variable cost.

II. VARIABLE COSTS A variable cost is a corporate expense that varies with production output. Variable costs are those costs that vary depending on a company's production volume; they rise as production increases and fall as production decreases. Variable costs differ from fixed costs such as rent, advertising, insurance and office supplies, which tend to remain the same regardless of production output. Fixed costs and variable costs comprise total cost.

III. SEMI-VARIABLE COSTS (MIXED COST) Those costs which are partly fixed and partly variable are called semi-variable costs. These costs vary with the level of production but not in direct proportion to level of production. The examples of such costs are depreciation of machinery, maintenance of equipment, administrative costs, etc.

D. CLASSIFICATION OF COST FOR MANAGERIAL DECISIONS AND CONTROL

METHODS & TECHNIQUES OF COSTING Several methods or systems of costing have been developed to suit the needs of individual business conditions. The general fundamental principles of ascertaining costs are the same in every system of costing but the methods of analysis and presentation of costs differ from industry to industry. The main consideration which applies to the choice of a particular method of costing is the nature and type of products or service rendered by the enterprise.

JOB COSTING Job costing is system of costing in which costs are ascertained in terms of specific job or order which are not comparable with each other. The unit of costing in this method is a job or a special work order. SUITABLITY - Industries engaged in printing, ship building, engineering, automobile garages, repair shops, made to order articles, building and construction, machine tools, locomotives, etc. Job costing includes the following methods of costing. • Batch Costing • Contract Costing or Terminal Costing • Departmental Costing

A. BATCH COSTING This method of costing is applied to industries where production is carried on in batches. Under this method, a batch of similar products is regarded as one job and the cost of this complete batch is ascertained. The total cost of the batch is then divided by the total number of units in the batch in order to determine the cost per unit. SUITABILITY – Confectionery, Toy Making, Medicines, Readymade Garments, Spare Parts, Processed food, Components manufacture, hardware articles like bolts, nuts, cycle parts, etc.

B. CONTRACT COSTING OR TERMINAL COSTING This method is mostly used in case of big jobs spread over a period of time. A contract is a big job and hence the principles of job costing are applied to contract costing. A separate account is kept for each individual contract. This method is also known as terminal costing as the cost can be terminated at some point and related to a particular job. SUITABILITY - Undertaking Engaged In Building Construction, Ship Building Construction Engineering, Civil Engineering, Mechanical Engineering etc.

C. DEPARTMENTAL COSTING When it is desired to ascertain the cost of operating a department or the cost of products turned out by a department, the method of departmental costing is used. SUITABILTY - Large undertakings that ascertain the cost of a department so as to allocate it among the various jobs turned out by that department.

PROCESS COSTING Process costing is an accounting methodology that traces and accumulates direct costs, and allocates indirect costs of a manufacturing process. Costs are assigned to products, usually in a large batch, which might include an entire month's production. Eventually, costs have to be allocated to individual units of product. It assigns average costs to each unit, and is the opposite extreme of Job costing which attempts to measure individual costs of production of each unit. It is a method of assigning costs to units of production in companies producing large quantities of homogeneous products. Process costing is a type of operation costing which is used to ascertain the cost of a product at each process or stage of manufacture.

CIMAdefines process costing as "The costing method applicable where goods or services result from a sequence of continuous or repetitive operations or processes. Costs are averaged over the units produced during the period". Process costing is suitable for industries producing homogeneous products and where production is a continuous flow. Process costing is appropriate when one order does not affect the production process and a standardization of the process and product exists. However, if there are significant differences among the costs of various products, a process costing system would not provide adequate product-cost information. SUITABILITY - Petroleum, Coal Mining, Chemicals, Textiles, Paper, Plastic, Glass, Food, Banks, Courier, Cement, And Soap.

SINGLE OUTPUT or UNIT COSTING : This method is of costing is applied where production is continuous and uniform and the industry is engaged in the production of single product or a few grades of same product. Total cost is divided by number of units in order to ascertain cost per unit. SUITABILITY - Brick Works, Oil Drilling, Paper Mills, Flour Mills, Cement Manufacturing, Textile Mills, etc. • OPERATING COSTING: This method is suitable for service sector which are indulged in providing services instead of production or manufacturing. SUITABILITY- Railways, Airways, Roadways, Hotels Power Supply, Water Supply.

OPERATION COSTING : Operating costing is a system of costing which is used in industries engaged in repetitive mass production. If the manufacture of a product involves a number of operations and not processes, the cost is ascertained for each operation. SUITABILITY - Engineering Industries, Toy Making, etc.

Cost sheet is a document which provides for the assembly of the estimated detailed cost in respect of a cost unit. It is a detailed statement of the elements of costs arranged in logical order under different heads. It is prepared to show the detailed cost of the total output for a certain period. It is only a memorandum statement and does not form part of the double entry system.

ADVANTAGES OF COST SHEET • Indicates the break-up of the total cost by elements, i.e. material, labour, overheads, etc. • Discloses the total cost and cost per unit of the units produced. • Facilitates comparison. • Helps in fixing selling prices. • Guide to the management and helps in formulating production policy. • Enables to keep control over cost of production. • Helps the management in submitting quotations or preparing estimates for tenders. • Simple and useful medium of communication of costs at various levels of management.

An analytical study of the behaviour of costs in relation to changes in volume of output reveals that there are some items of cost which tend to vary directly with the volume of output whereas, there are others which remain unaffected by variations in the volume of output. The former class of costs represents the variable cost and the later fixed cost. Besides, there are certain items of cost which are partly fixed and partly variable and are known as semi-variable or semi-fixed cost.

Fixed Cost Fixed costs are non-variable costs, stand-by costs, period costs or capacity cost and are those costs which do not vary with changes in volume of output over a given period of time and within a relevant range of activity. Fixed cost, thus, remain constant in total amount whether there is any increase or decrease in the level of activity or output. There is an inverse relationship between volume of output and fixed cost per unit. When there is decrease in volume of output, the fixed price cost per unit increases. Conversely, fixed cost per unit decreases with increase in volume of output.

Fixed cost can be divided into two categories from the profit planning and control point of view: COMMITTED FIXED COSTS : Committed costs are those fixed costs which are caused by investments in fixed assets, such as building plant or equipment, for providing production facilities. These costs are called committed costs because the firm has committed itself to incur such costs for a long period. Depreciation, insurance, rent, property tax etc. are some examples. Once a firm purchases building, plant or equipment, it commits itself to depreciation charge, insurance charge, property tax, etc. for fairly long period.

DISCRETIONARY FIXED COST : Discretionary costs, also referred to as programmed or managed costs, are those fixed costs, the amount of which is decided by the management. Such costs can be reduced substantially at any period of time at the discretion of the management. Some examples of Discretionary Fixed Cost are Research & Development cost, Advertising costs, expenses incurred on human resource development, public relations, etc. Generally, the benefits of such costs does not accrue in the same period when these are incurred.

Variable Costs Variable costs are those costs which fluctuate, in total, in direct proportion to the volume of output. Such costs increase in aggregate as the output increases and decrease in the same proportion when the output falls. A variable cost, thus, in total, changes in the same direction and in direct proportion to changes in production activity, sales activity or some other measures of volume. The cost of direct material, direct labour, supplies and direct expenses like sales commission are some examples of variable cost.

Semi-Variable cost (Mixed Cost) Semi-Variable costs are a combination of fixed and variable cost and are, thus, also known as mixed costs. Such costs are neither perfectly variable nor absolutely fixed in relation to changes in volume of output. The fixed component of such costs represents the cost of providing capacity and the variable component is caused by using the capacity. Semi variable costs fluctuate in the same direction but not in direct proportion to the changes in volume of output. They go up with volume but not in the same proportion as volume. Hence, these costs should be plotted on a graph as a curved line.

Utility bills, such as power costs, telephone charges, repair and maintenance costs, etc. are some examples of semi-variable costs. For example power costs include a fixed portion of minimum charge that will be charged even if you do not consume power and variable charge based on consumption of power. Thus, power cost increases with increase in production activity but not in the same proportion.

ADVANTAGES OF CLASSIFYING COSTS INTO FIXED AND VARIABLE • PROFIT PLANNING : The primary objective of doing any business is to earn profit. Hence, it is very important to make profit planning. It is concerned with taking series of decisions making and selecting amongst the various alternatives available. Thus, it is very important to study the behaviour of cost and profit in relation to change in volume of output. • EFFECTIVE COST CONTROL : Profits can also be increased through effective cost control and cost reduction. Classification of costs into fixed and variable elements helps management to control costs effectively as fixed costs are incurred by management decisions and can be controlled only by the top management. Further, variable cost may be controlled even at the lower levels of management.

FIXATION OF SELING PRICES : Profits could be maximized either by reduction and control over costs or by increasing the sales value through increase in sales volume or prices. Fixation of proper selling price is thus important for management. Segregation of costs into fixed and variable elements enables to adopt most appropriate selling price policy as sometimes one may have to sell even below total cost. However, it should not be below variable cost. • PROPER ABSORPTION OF OVERHEADS : The analytical study of the behaviour of costs also helps in proper absorption of overheads as the method to be adopted for the absorption depends upon the nature of overheads.

HELPFUL IN DECISION-MAKING : The classification of cost into fixed and variable elements helps management in taking many decisions such as make or buy decisions, selection of a product mix, capacity decision, operate or close down decisions, etc. • BUDGETARY CONTROL : For the preparation of flexible budgets and effective budgetary control, this classification is a pre-requisite. The flexible budget is designed to change in accordance with the level of activity and hence the cost behaviour is very important. • MARGINAL COSTING & BREAK-EVEN ANALYSIS : Basic assumption for marginal costing and breakeven analysis is that all elements of cost can be segregated into fixed and variable. Hence, for the use of marginal costing and breakeven techniques, the classification of cost is very essential.