Download

1 / 51

510 likes | 715 Views

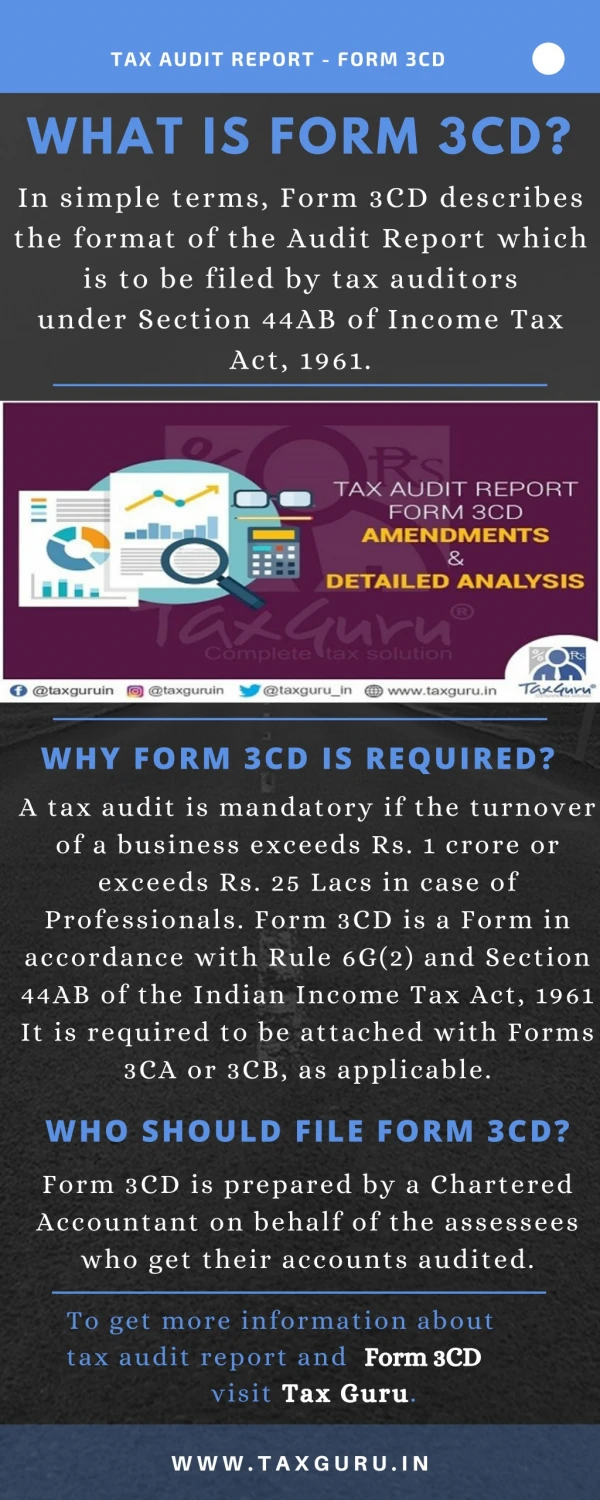

E-filing of 3CD. Download the respective Form(3CA-3CD/3CB-3CD) from “www.incometaxindiaefiling.gov.in” and enable the Macros. Click on launch form 3CA-3CD/ 3CB-3CD. The Fields marked with Asterisk (*) are mandatory to be filled.

E N D

E-filing of 3CD • Download the respective Form(3CA-3CD/3CB-3CD) from “www.incometaxindiaefiling.gov.in” and enable the Macros. • Click on launch form 3CA-3CD/ 3CB-3CD

The Fields marked with Asterisk (*) are mandatory to be filled. • In From 3CB the, Tax Auditor may report Observations/ Discrepancies/ Comments /inconsistencies , If any in Clause 3(a), whereas in From 3CA this option is not available.

Clause 7 (a), • Requires profit sharing ratio to be numeric, non negative and non decimal. In reality it can be in decimal

Clause 8 (a) & (b) • Sector and sub sectors are required to be reported. • Business added or discontinued during the year is required to be reported

Clause 9 (Section 44AA) • Books of accounts prescribed u/s 44AA(3) • Rule 6F prescribes books for Professionals:- • Cash Book • Journal • Ledger • Additional Documents, in case of Medical Profession:- • Daily case register in From 3C. • Inventory under broad heads. • These are not books of accounts and not to be reported in Clause 9(a).

Clause 10 (Section 44AD,44AE,44AF,44B,44BB,44BBA,44BBB,) • Amount as per Statement of Profit or Loss is to be reported. • The Tax Auditor is not required to indicate as to whether such amount corresponds to the amount assessable under relevant sections relating to presumptive taxation.

Clause 11 (Section 145) U/s 145 of Income Tax Act, 1961 Corresponding Accounting Standards issued by ICAI AS IT I AS IT II AS 1 AS 5 Revised in 1997

Clause 12(a) (Section 145A) • Closing stock valuation method to correspond with AS 2. • Space limitation 100 characters, representation made to CBDT • Clause 12(b) (Section 145A) • Section 145A is for computation of income and not for maintenance of books of accounts. • Deviation from 145A does not effect the Profit or Loss. • Stock valuation in books of accounts as per AS 2, deviations to be mentioned in clause 12(b).

Clause 12(A)( Section 2(47), 45(2), 47(iv),(v) and 47A) • U/s 45(2) conversion or treatment of capital asset into stock in trade is deemed transfer. • Capital gains taxable in the year in which the stock in trade is sold or otherwise transferred. • Fair value on the date of transfer not required to be reported. • Accounting entry should be passed at the time of conversion of asset.

Clause 13 (section 28) • Information under sub clauses (a),(d) and (e) is to be given with reference to books of accounts. • Mere making of claims does not constitute claim accepted. • In cash method of accounting clauses (b) and (c) have no significance.

Clause 14 (CENVAT) • “Allowable” implies depreciation is allowable as per the Act – Auditor to exercise Professional Judgment . • Depreciation rates depend on classification – Auditor to ensure classification is as per Legal Principals. • Adjustment required for • CENVAT Credit. • Change of exchange currency. • Subsidy or Grant for reimbursement. • Section 43A applies were assets are acquired from outside India.

Clause 16(b) (Section 36(1)(ii) & (va)) • Due date of payment includes provision for 5 days of grace period as per PF manual. • Amount paid up to due date of filing the return, held to be allowable in following cases:- • CIT vs. Dharmendra Sharma 297 ITR 320. • CIT vs. P.M. Electronics Ltd. 313 ITR 161. • CIT vs. AIMIL Ltd. and others 321 ITR 508. • Contrary decision in case of CIT vs. Pamwi Tissues Ltd. (2008) 215 CTR 150 (Bom.)

Clause 17(a) – (e) • Amount debited as per books of accounts to be reported. Payment for violation of law to be distinguished from penalty for contractual violation . • Payment to political parties is inadmissible under section 37(2B) but allowable u/s 80GGB/80GGC.

Clause 17(f) (section 40(a)) • Amount inadmissible u/s 40(a)(ia) to tally with particulars of TDS under clause 7. • Copy of Form 26A to be obtained were Auditee claim under second proviso of Section40(a)(ia). • Clause 17(h) (Section 40A(3)) • Tax Auditor to obtain certificate from the assessee. • Inadmissible if any reported. • Presently no disclaimer.

Clause 17(l) (Section 14A) • Auditor should also be aware about sub rule (2) of rule 8D of the Act . • Provision of section 14A will also apply even, no expenses has been incurred to earn income which does not form part of the total income. • Clause 17(m) (Section 36(1)(iii)) • Tax Auditor need to apply professional judgment in determining the applicability of the proviso. • Tax Auditor should also verify treatment like chapter VI A deduction or requirement under other statutes, as well as applicable Accounting Standards.

Clause 17A (Section 23) • The Tax Auditor should take information of the enterprise which is covered under MSME Act. • Auditor should also keep in mind section 16, 22 and 23 of MSME Act. • Clause 18 (Section 40A(2)(b)) • Auditor should verify the list of all persons covered under the section and take all relevant information. • Separate list of payments made to related parties should be obtained. Date wise details to be reported in e - portal.

Clause 19 (Section 33AB,33ABA or 33AC) • The Tax Auditor needs to ensure all necessary conditions are satisfied by the assessee.

Clause 20 (Section 41(1)) • “Liability ceases when it has become barred by limitation and the assessee has unequivocally expressed its intention not to honour the liability, when demanded”. This is a question of fact CIT vs. Chase Bright Steel Ltd. 177 ITR 128(Bom.). • When a liability is shown outstanding for more than 4 years, in case of an assessee company, the amount was not assessable under section 41(1) CIT vs. ShriVardhman Overseas Ltd. (2012) 343 ITR 408(Del).

Clause 21 (Section 43B) • Auditor need to keep in mind clause 16(b) (Section 36(1)(ii) & (va)). • Amount shall be allowed on the basis of actual payment.

Clause 22 • Tax Auditor need to apply professional judgment in determining the applicability of the Accounting Standards.

Clause 24 (Section 269SS) • Tax Auditor need to keep in mind proviso to section 269SS. • Share Application money is neither deposit nor loan if appropriate documentation is available. Rugmuni Ram Ragav Spinners P. Ltd. 304 ITR 417(Madras High Court)

Clause 25 (Section 70 to 79) • The loss will be numeric, non negative and non decimal. • Pending assessment, rectification, revision or appeal proceeding to be disclosed. • The overriding provisions of section 79 do not affect the set off of unabsorbed depreciation which is governed by section 32(2). CIT Vs. Concord Industries ltd. (1979) 119 ITR 458 (Mad), CIT vs. ShriSubbulaxmi Mills Ltd. 249 ITR 795 (SC).

Clause 27 (Chapter XVII-B) • Tax Auditor may exercise his judgment in the light of the applicable law and report accordingly about the compliance of this provision. • Day of delay not to be reported. • PAN of the party should me mentioned in e portal. • Reasons for not making payment to the credit of Central Government is mandatory on e portal. • Due date & Actual date of payment is to be reported.