Download

1 / 35

350 likes | 355 Views

This topic covers the concept of cost-volume-profit (CVP) analysis and its application in managerial accounting. Learn how to calculate the break-even point and assess profitability using CVP calculations.

E N D

Topic2BC-V-P ACCT71-014 Managerial Accounting Learning Objectives Demonstrate an understanding of cost-volume-profit analysis Define and describe the breakeven point Apply CVP calculations to a single product Demonstrate an understanding of the use of margin of safety and operating leverage to assess risk. Application of basic cost-volume-profit (CVP) calculations. Chapter 4.

Cost-volume-profit (CVP) analysis Ch 4 Learning Objective 1 • CVP analysis looks at the relationship between selling prices, sales volumes, costs and profits. • CVP analysis provides information about: • products or services to emphasise • volume of sales needed to achieve target profit • revenue required to avoid losses • whether to increase fixed costs • budgets for discretionary expenditures • level of risk related to fixed costs.

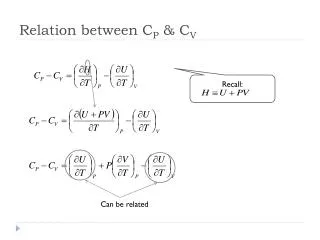

Cost–volume–profit (CVP) analysis • Profit equation and contribution margin: • Basic profit equation: Profit = Total revenue-Total costs • This can be rewritten as: Profit = Total revenue – (Total variable costs + Total fixed costs) • Or: Profit = (Total revenue – Total variable costs) – Total fixed costs

Cost–volume–profit (CVP) analysis • Profit equation and contribution margin: • Contribution margin: • Total revenue minus total variable costs. • Contribution margin per unit: • The selling price per unit minus the variable cost per unit. • Determines how much revenue from each unit sold can be applied towards fixed costs. • When fixed costs are covered, remaining sales becomes profit.

Profit equation and contribution margin • Profit equation and contribution margin: • Profit equation in terms of CM per unit: Profit = [(P – V) × Q] – F Where: P = Selling price per unit V = Variable cost per unit (P – V)= Contribution margin per unit Q = Quantity of product sold F = Total fixed costs

Fixed costs . Contribution margin per unit Units to breakeven = Breakeven point Learning Objective 2 • The breakeven point is where total revenue equals total costs, giving zero profit. • Breakeven point can be calculated in: • number of units • or in total revenues. • To determine breakeven pointin units, the profit equation is restated as:

Contribution margin per unit. .. . Sales price per unit Contribution margin ratio = Breakeven point • To calculate the breakeven point in sales dollars, first calculate the contribution margin ratio. • The contribution margin ratio (CMR) is the percentage by which selling price (or revenue) per unit exceeds variable cost per unit. • Or, it is the contribution margin as a percentage of revenue. • Step 1:

Fixed costs . Contribution margin ratio Total revenue to break even = Breakeven point • The CVP equation is adapted to calculate the breakeven point in total revenue: • the fixed costs are divided by the contribution margin ratio. • Step 2:

CVP analysis for a single product Learning Objective 3 • Let's look at an entity, Mount Dandenong Bikes who want to produce a new mountain bike. • The following information has been forecasted:

Breakeven quantity $5 500 000. ($800 – $300) = = 11 000 bikes CVP analysis for a single product • Calculating breakeven in units and total revenue: • Use the breakeven data to assess the riskiness of the venture, by comparing the sales forecast to the breakeven sales: • For Mount Dandenong Bikes to generate a profit, sales would need to exceed 11 000 bikes.

($800 – $300).) $800 CMR = = 0.625 CVP analysis for a single product • Calculating breakeven in units and total revenue: • The breakeven point can also be calculated to give the total revenue required to cover both fixed and variable costs. • First calculate the contribution margin ratio (CMR): • For Mount Dandenong Bikes to generate a profit, sales would need to exceed 11 000 bikes.

$5 500 000. 0.625 Sales revenue to breakeven = = $8 800 000 CVP analysis for a single product • Calculating breakeven in units and total revenue: • Dividing the fixed costs by the contribution margin ratio enables the determination of breakeven sales revenue: • Revenue of $8 800 000 is required to break even:

Sales quantity Sales revenue (F + Profit)) (P – V) (F + Profit) CM ratio = = CVP analysis for a single product • Achieving a targeted pre-tax profit: • An entity would want to earn a profit to enable funds to be available for working capital and investment. • Both the sales quantity and revenue needs to be calculated.

Sales quantity ($5 500 000 + $300 000) ($800 – $300) = = 11 600 bikes CVP analysis for a single product • Achieving a targeted pre-tax profit: • Mount Dandenong Bikes want to earn $300 000 pre-tax profit. • They need to sell more than the breakeven point of 11 000 bikes. • The quantity of mountain bikes to reach the targeted profit needs to be calculated:

Sales revenue ($5 500 000 + $300 000)0.625 = = $9 280 000 CVP analysis for a single product • Achieving a targeted pre-tax profit: • To generate the $300 000 pre-tax profit, 11 600 bikes need to be sold. • The contribution margin ratio of 62.5 per cent can also be used to determine the sales revenue of the bikes needed for the targeted profit. • Using the contribution margin ratio:

CVP analysis for a single product • Achieving a targeted pre-tax profit: • Mount Dandenong Bikes must increase sales by $480 000 (600 bikes times $800) beyond breakeven sales of $8 800 000 to generate the $300 000 pre-tax profit.

After-tax profit. (1 – Tax rate) Pre-tax profit = CVP analysis for a single product • Looking at after-tax profit: • Sometimes, profit may be shown as an after-tax amount. • For CVP analysis, the after-tax amount needs to be converted a pre-tax amount. • The formula below can be used to calculate pre-tax profit:

Pre-tax profit $210 000 (1 – 0.30) = = $300 000 CVP analysis for a single product • Looking at after-tax profit: • Mount Dandenong Bikes plans for an after-tax profit of $210 000 and its tax rate is 30 per cent: • This means that the entity needs a pre-tax profit of $300 000 to earn an after-tax profit of $210 000.

CVP analysis for a single product Cost-volume-profit (CVP) graph: shows the relationship between total revenues and total costs. illustrates how an organisation’s profits are expected to change under different volumes of activity.

CVP analysis for a single product • Cost-volume-profit (CVP) graph: • shows the relationship between total revenues and total costs. • CVP graph for the new mountain bike:

Assumptions and limitations of CVP analysis CVP analysis relies on forecasts of expected revenues and costs. Assumptions rule out fluctuations in revenues and costs. Many uncertainties arise: Is desired operating volume achievable? Will selling prices go up or down? Will sales mix remain constant? Will fixed or variable costs change in new relevant range? Will costs change due to unforeseen events? Are revenue and cost estimates biased?

Margin of safety and degree of operating leverage CVP analysis can be used to help manage operational risk. Operational risk relates to risk of loss resulting from inadequate or failed internal processes, people and systems, or external events. Learning Objective 4

Actual or estimated units of activity Margin of safety (units) Units at breakeven point = – Margin of safety (revenues) Actual or estimated revenue Revenue at breakeven point = – Margin of safety and degree of operating leverage • Margin of safety is the excess of a firm’s expected future sales above the breakeven point.

Margin of safety % (units) Margin of safety % (revenues) Margin of safety in units Actual or estimated units Margin of safety in revenue Actual or estimated revenue = = Margin of safety and degree of operating leverage • The margin of safety percentage indicates the extent to which sales can decline before profits become zero.

Margin of safety (revenue) Margin of safety (%) = 1000/12 000 = 8.3% = $9.6M – $8.8M = 800 000 = 12 000 – 11 000 = 1 000 Margin of safety (units) Margin of safety and degree of operating leverage • For example, Mount Dandenong Bikes: • Breakeven point = 11 000 bikes or $8 800 000 in revenues. • Expected sales units = 12 000 • Expected revenue = $9 600 000 • Sales volume could drop by 8.3% before a loss is incurred.

Margin of safety and degree of operating leverage Degree of operating leverage: Measures the extent to which the cost function is comprised of fixed costs. A high degree of operating leverage indicates a high proportion of fixed costs. Firms operating at a high degree of operating leverage: face higher risk of loss when sales decrease enjoy profits that rise more quickly when sales increase.

Margin of safety and degree of operating leverage • Degree of operating leverage: • Formula can be written in terms of either contribution margin or fixed costs:

Margin of safety and degree of operating leverage • The degree of operating leverage can be used to: • gauge the risk associated with cost function • calculate the sensitivity of profits to changes in sales (units or revenues).

Margin of safety and degree of operating leverage • Example for Mount Dandenong: • Degree of operating leverage (using CM): (Total expected CM / Expected profit) • Degree of operating leverage (using FC): • ((Total expected FC / Expected profit) + 1)

Margin of safety and degree of operating leverage • Degree of operating leverage and margin of safety percentage are reciprocals: • Mount Dandenong Bikes: margin of safety percentage is 12 (1 ÷ 0.0833). • Mount Dandenong Bikes: degree of operating leverage is 0.0833 (1 ÷ 12).

Margin of safety and degree of operating leverage Using the degree of operating leverage to plan and monitor operations: Need to consider degree of operating leverage for additional fixed costs. For example purchasing new equipment or hiring new employees. The appropriate strategy can be determined by calculating the point of indifference. An indifference point is the level of activity at which equal cost or profit occurs across multiple alternatives.

Margin of safety and degree of operating leverage • Example of using operating leverage to plan and monitor operations: • Mount Dandenong Bicycles (MDB) is considering restructuring their sales team by subcontracting sales staff and paying a commission of $50 per bike sold. This would reduce payroll by $200 000 each year (and increase VCs by $50). • The new cost function would be: TC = ($5 500 000 - $200 000) + ($300 + $50)Q = $5 300 000 + $350Q • The new CM would be: $800 - $350 = $450 • The new breakeven point would be: $5 300 000 / $450 = 11 778 units; or $9 422 400 sales revenue

Margin of safety and degree of operating leverage • Example of using operating leverage to plan and monitor operations: • Using budgeted assumptions, two cost functions are set as equal and Q is solved. • At 4000 sales level, each strategy incurs the same level of expenditure. • When sales are fewer than 4000, profit will be greater using more variable costs. • When sales exceed 4000, profit will be greater with more fixed costs. • Note that MDB’s breakeven point is considerably higher than 4000, thus, the proposed restructure, to reduce CM and fixed costs, is not recommended.

Summary Cost–volume–profit (CVP) analysis: Profit equation and contribution margin. Breakeven point and contribution margin ratio. CVP analysis for a single product: Calculating breakeven in units and total revenue. Achieving a targeted pre-tax profit. Looking at after-tax profit. Cost–volume–profit (CVP) graph.

Summary Margin of safety and degree of operating leverage: Operational risk. Margin of safety. Degree of operating leverage. Degree of operating leverage to plan and monitor operations