Download

1 / 10

110 likes | 464 Views

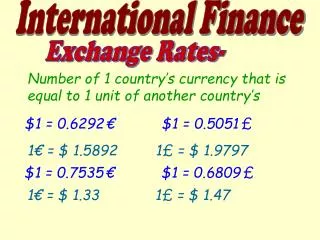

Forward Exchange Rates. Forward Contract. A forward contract in the forex market that locks in the price at which an entity can buy or sell a currency on a future date. Also known as "outright forward currency transaction", "forward outright" or "FX forward". Currency Forward .

E N D

Forward Contract • A forward contract in the forex market that locks in the price at which an entity can buy or sell a currency on a future date. Also known as "outright forward currency transaction", "forward outright" or "FX forward".

Currency Forward • In currency forward contracts, the contract holders are obligated to buy or sell the currency at a specified price, at a specified quantity and on a specified future date. These contracts cannot be transferred.

Example • A U.S. firm is obligated to make a future payment of CHF 100,000 in 60 days. The firm contracts to buy CHF 60 days forward @ 1.7530. The current exchange rate is 1.7799. What is the gain or loss without this contract if the rate after 6 months is 1.6556.

Forward Spreads • A currency is either at a forward premium or a forward discount. • Forward discount = Fr – Sr = -ve number • Forward Premium = Fr – Sr = +ve number

Annualized Spread Forward Premium or discount = [Forward Rate – Spot rate] [ 360 ] Spot Rate no. of forward days

Swap Points Swap Points = Spot rate x Int. diff x days 360 Forward Rate = Spot rate + Swap points

Interest Rate Parity Interest differential ≈ forward differential {Rd – Rf} = [Forward Rate – Spot rate] Spot Rate Forward = 1+Rd Spot 1+Rf

Discounting Discounted rate = Forward Rate 1 + i/365 * days