Download

1 / 14

190 likes | 530 Views

Tools of Monetary Policy. Chapter 15: The Market for Reserves and the Fed Funds Rate, i ff. Open market operations Affect the quantity of reserves and the monetary base Changes in borrowed reserves Affect the monetary base Changes in reserve requirements Affect the money multiplier

E N D

Tools of Monetary Policy Chapter 15: The Market for Reserves and the Fed Funds Rate, iff • Open market operations • Affect the quantity of reserves and the monetary base • Changes in borrowed reserves • Affect the monetary base • Changes in reserve requirements • Affect the money multiplier • Federal funds rate—the interest rate on overnight loans of reserves from one bank to another • Primary indicator of the stance of monetary policy

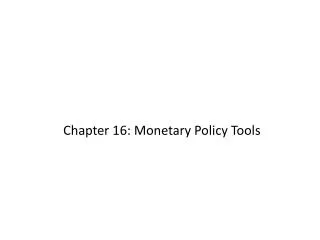

Demand in the Market for Reserves • What happens to the quantity of reserves demanded, holding everything else constant, as the federal funds rate changes? • Two components: required reserves and excess reserves • Excess reserves are insurance against deposit outflows • The cost of holding these is the interest rate that could have been earned • As the federal funds rate decreases, the opportunity cost of holding excess reserves falls and the quantity of reserves demanded rises • Downward sloping demand curve Supply in the Market for Reserves • Two components: non-borrowed and borrowed reserves • Cost of borrowing from the Fed is the discount rate • Borrowing from the Fed is a substitute for borrowing from other banks • If iff < id, then banks will not borrow from the Fed and borrowed reserves are zero • The supply curve will be vertical • As iffrises above id, banks will borrow more and more at id, and re-lend at iff • The supply curve is horizontal (perfectly elastic) at id

Reserves Market iFF SR = Rn + DL iD SR i*FF DR = f {iFF; RR + ER} (-) (rxD) , DDFE iER D1R Rn Reserves

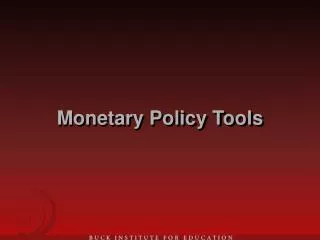

FED RES Assume: r = 20% c = 25% iD = 10% C = 125 GS = 250 R = 125 DL = 0 Conservative Bank Aggressive Bank RR = 50 ER = 50 RR = 25 ER = 0 D = 250 D = 250 DL = 0 DL = 0

Conservative Bank Aggressive Bank

Reserves Market Fed Funds Market iFF iFF 50 100 25 10 8 6 4 2 10 8 6 4 2 115 30 40 125 35 35 165 0 40 10 20 30 40 50 100 115 125 135 145 155 165

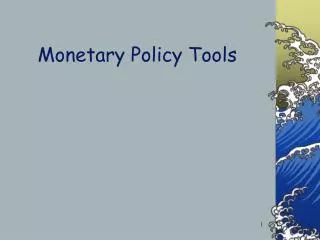

D Reserve Requirements Advantages 1. Powerful effect Disadvantages 1. Small changes have very large effect on Ms 2. Raising causes liquidity problems for banks 3. Frequent changes cause uncertainty for banks 4. Tax on banks

Policy D: r => RRD => DR shifts right => iFF iFF iD SR i2FF i1FF D2R iER D1R Rn Reserves

Open Market Operations Fed 2 Types 1. Dynamic: Meant to change MB 2. Defensive: Meant to offset other factors affecting MB, typically uses repos Advantages of Open Market Operations 1. Fed has complete control 2. Flexible and precise 3. Easily reversed 4. Implemented quickly Currency Gov. Sec.s Reserves

Policy D: Open Market Operation iFF iD S1R S2R OMP: Rn => shift SR right => iFF i1FF OMS: Rn => shift SR left => iFF i2FF DR R1n R2n Reserves, R

Discount Loans 3 Types 1. Primary Credit 2. Secondary Credit 3. Seasonal Credit Lender of Last Resort Function 1. To prevent banking panics FDIC fund not big enough Example: Continental Illinois 2. To prevent nonbank financial panics Examples: 1987 stock market crash and 9/11 terrorist incident

9/11 => DR => iFF => DL => Policy D: iD => iFF => DL iFF iD is safety valve to relieve market pressure S1R iD = 6.25% 1% Spread iD to 5.25% S2R i*FF = 5.25% D2R D1R Rn Reserves, R

Econ 330 Chapter 15 HomeworkDue Friday, March 28 Chapter 15 Questions & Applied Problems 9, 11, 20, 23, 25