Download

1 / 25

250 likes | 364 Views

All in the Family? Children’s Public Coverage, Dual-Earner Households and Employer-Sponsored Insurance. Jessica Vistnes (AHRQ) Kosali Simon (Indiana University, SPEA and NBER). Motivation.

E N D

All in the Family? Children’s Public Coverage, Dual-Earner Households and Employer-Sponsored Insurance Jessica Vistnes (AHRQ) Kosali Simon (Indiana University, SPEA and NBER)

Motivation • Dependent health insurance for workers’ spouses and children is an important source of coverage in the U.S. • Roughly half of non-elderly Americans covered by employer-sponsored insurance have that coverage as a dependent (Current Population Survey, 2008).

Employees’ Enrollment Decisions • Two-worker Couples with Two Offers of Insurance: • Without children • 2 single policies vs. 1 family policy? • Employee-plus-one coverage, if available? • With children: • Are eligible for public coverage? • Different sources of coverage to cover everyone?

Employers’ Decisions • Offer coverage at all? • Offer dependent coverage? • How to set employee contributions? • Restrict access to coverage for worker’s spouse? • Offer cash incentives if workers decline coverage?

Prior Literature On effects of coverage through a working spouse: • Dranove, Spier and Baker (2001) • Vistnes, Morrisey, Jensen (2006) On effects of public coverage for children: • Shore-Sheppard, Buchmueller, Jensen (2000) • Buchmueller, Cooper, Simon and Vistnes (2005)

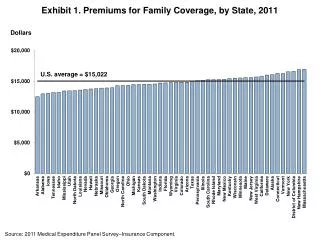

Changes in Dependent Coverage 2000-2008 • Dependent coverage is less likely to be offered at small employers • Employee-plus-one coverage more likely to be offered • Employee premium contributions have risen

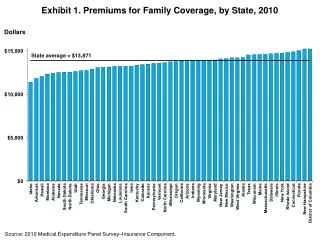

Availability of Dependent Coverage Firms with < 10 workers All Firms Source: Vistnes, Zawacki, Simon and Taylor (2012)

Goals • To re-examine the effects of alternative sources of coverage on a number of ESI outcomes • To take into account rising unemployment rates over our analysis period and investigate whether the effects of alternative sources differ at low and high unemployment rates

MEPS-Insurance Component(MEPS-IC) • 2005-2010 MEPS-IC • Large, annual, nationally representative establishment level survey • Sponsored by AHRQ, conducted by the Bureau of the Census. • Collects information on: • Offers of insurance, establishment/workforce characteristics • Number and types of plans • Total premiums, employee and employer contributions • Deductibles, copayments/coinsurance and other benefit details

Data • Information on full-time workers’ family characteristics • Estimates calculated from the 2005-2010 American Community Survey (ACS) • Merge onto the MEPS-IC by state, detailed industry and year • 2005-2010 Area Resource File: • County Unemployment Rate • Other variables • Estimate models separately by firm size Small : < 100 and Large: >=100 workers

Dependent Variables: Establishment Level • Offers • Any coverage • Any dependent coverage • Take-up rates • Enrollment Shares for single, employee-plus-one, family • Restrictions on spousal coverage • Financial incentives to decline coverage

Key Independent Variables • Proportion of full-time workers (From ACS): • Married • Have children • Have children and are < 200% FPL • In families with two full-time working spouses • Eligibility index for Medicaid/CHIP coverage for children • Unemployment rates • Interaction terms • In families with two full-time working spouses * female • Have children and are < 200% FPL * Medicaid/CHIP Eligibility

Other Explanatory Variables • Establishment Characteristics: • Firm size, industry, age of business, ownership type, non-profit status • Workforce Characteristics: • Proportion of workers that are • Age 50 and older, female, union members • Wage distribution (three wage categories) • Plan type, # plans, single premium in plan equations • State and year fixed effects • County level characteristics from Area Resource File

Offer model with unemployment interactions Small firms Estimated a second model that added the following two variables: Unemployment rate * two-worker-family Unemployment rate * two-worker-family * female

Outcome: Offer Equation with Unemployment Interactions - Small Firms What if the % Two-Worker increases from 0 to 30%? • At establishments that are 50% female

Outcome:Family - Single Contributions Large Firms Increasing % Two-Worker Increasing % Low-Income Children At mean value for public eligibility Increasing proportion with children < 200% FPL: 0 to mean values $142 increase in marginal family contributions • At 50% female • Moving from 0% to 30% for two-worker families: • $508 increase in marginal family contributions

Outcome: Spousal Restriction on Coverage Large Firms Percentage Point Change in Spousal Restriction on Coverage • What if the percent of “workers married” increases from 0 to 50%? • And the percent of “2-worker households” increases from 0 to 25%?

Outcome: Family enrollment shares Large firms • What if we increase “% married” from 0 to 50% ? • 10 percentage point increase in family share • What if we increase “% with children” from 0 to 50? • 10 percentage point increase in family share

Outcome: Enrollment Shares Large firms What if we increase the “% in two-worker families”?

Outcome: Cash Incentives • Large firms: • More likely to offer cash incentive as proportion with children increases • May reflect that these employees are more likely to enroll in expensive family coverage • Less likely to offer cash incentive as the proportion in two-worker families increases • May reflect that these employees are less likely to enroll in family coverage • Small firms: • Positive, significant effects on variables associated with alternative sources of coverage for children and adults

Summary • Alternative sources of coverage affect: • Offers of coverage • Restrictions/incentives by employers • Premium contributions • Enrollment decisions • No distinction can be made between • Employers acting as agents for workers • Strategically encouraging alternative coverage

The Affordable Care Act • The ACA introduced new alternative sources of coverage and new incentives for workers and employers. • Understanding how dependent coverage has changed in recent years helps set the context for changes that will occur under the ACA.