Download

1 / 7

0 likes | 24 Views

When it comes to real estate investment, finding innovative financing solutions is essential. One such solution that has gained popularity among investors is the Debt Service Coverage Ratio (DSCR) loan. In this comprehensive guide, we will explore the intricacies of a DSCR Loan, equipping you with the knowledge necessary to navigate the real estate market with confidence.

E N D

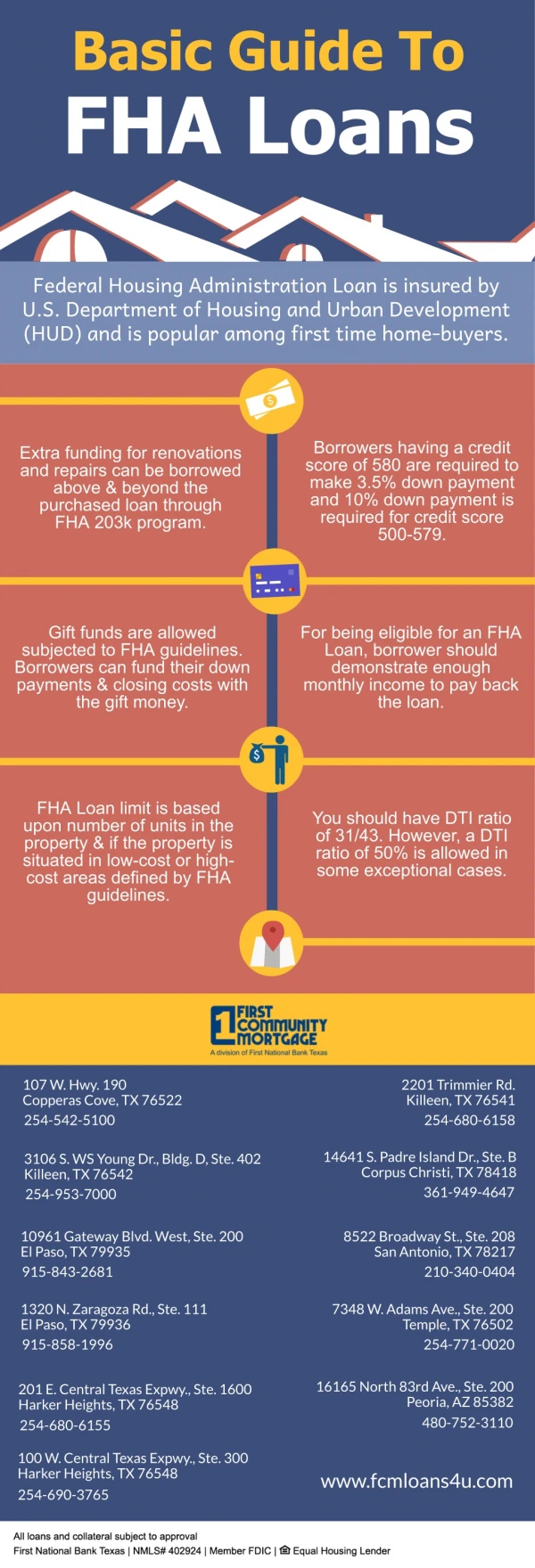

The Ultimate Guide to DSCR Loans: Everything You Need to Know Introduction When it comes to real estate investment, finding innovative financing solutions is essential. One such solution that has gained popularity among investors is the Debt Service Coverage Ratio (DSCR) loan. In this comprehensive guide, we will explore the intricacies of a DSCR Loan, equipping you with the knowledge necessary to navigate the real estate market with confidence. Table of Contents What are DSCR Loans? #what-are-dscr-loans Who are DSCR Loans For? #who-are-dscr-loans-for How to Calculate DSCR #how-to-calculate-dscr DSCR Loan Requirements #dscr-loan-requirements Down Payment #1-down-payment Credit Score #2-credit-score Property Appraisal #3-property-appraisal Debt Service Coverage Ratio #4-debt-service-coverage-ratio The DSCR Loan Application Process #the-dscr-loan-application-process Step 1: Research and Selection #step-1-research-and-selection Step 2: Gather Necessary Documentation #step-2-gather-necessary-documentation Step 3: Submitting the Loan Application #step-3-submitting-the-loan-application Step 4: Underwriting and Evaluation #step-4-underwriting-and-evaluation Step 5: Loan Offer and Acceptance #step-5-loan-offer-and-acceptance Step 6: Closing and Disbursement #step-6-closing-and-disbursement DSCR Loan Interest Rates #dscr-loan-interest-rates Texas Real Estate Market Overview #texas-real-estate-market-overview Is Now a Good Time to Invest inReal Estate? #is-now-a-good-time-to-invest-in-real-estate DSCR Loans for Commercial Real Estate and Other Investment Types #dscr-loans-for-commercial-real- estate-and-other-investment-types Conclusion #conclusion Frequently Asked Questions #frequently-asked-questions What are DSCR Loans? A DSCR loan, or Debt Service Coverage Ratio loan, is a type of mortgage loan specifically designed for residential income-producing properties. Unlike traditional mortgage loans that

heavily rely on the borrower’s income and creditworthiness, DSCR loans prioritize the property’s cash flow and profitability. This makes them an attractive financing option for real estate investors. DSCR loans offer flexibility and ease of qualification, making them ideal for self-employed individuals, investors with partners or teams, and those pursuing niche investment strategies such as short-term rentals or the BRRRR method (Buy, Renovate, Rent, Refinance, Repeat). With DSCR loans, investors can qualify without the need for W2 forms, tax returns,or extensive income verification. Who are DSCR Loans For? DSCR loans are suitable for a wide range of real estate investors. Whether you are a first- time investor or a seasoned professional looking to scale your portfolio, DSCR loans offer a flexible solution with easy qualification requirements. Here are some scenarios where DSCR loans are particularly beneficial: Self-employed or Freelance Investors Traditional lenders often require steady employment and a history of consistent income for investment property financing. This can make it challenging for self-employed individuals or freelancers to qualify. DSCR loans provide an alternative as they do not rely on W2 income, DTI ratios, or extensive documentation. Instead, eligibility is based on the income potential of the property itself. Investors with Partners or Teams Real estate investing often involves partnerships where individuals with complementary skills and resources come together to maximize returns. DSCR loans accommodate partnerships or LLCs, allowing multiple investors to share ownership and borrow collectively. This flexibility makes DSCR loans an attractive option for investors who prefer to collaborate and leverage each other’s strengths. Investors Pursuing Niche Strategies DSCR loans are not limited to traditional long-term rental properties. Investors pursuing niche strategies such as short-term rentals (e.g., Airbnb) or the BRRRR method can also benefit from DSCR loans. Conventional lenders are often slow to adapt to these newer investment strategies, but DSCR lenders are more flexible and accommodating, making them a preferred choice for investors looking to maximize cash flow and capitalize on emerging trends. How to Calculate DSCR The Debt Service Coverage Ratio (DSCR) is a crucial metric used to assess the financial viability of a property and determine eligibility for a DSCR loan. The DSCR is calculated by dividing the property’s cash flow or net operating income (NOI) by the total debt service, which includes principal and interest payments. A DSCR ratio of 1.00 indicates that the property’s income covers its debt obligations, while a ratio above 1.00 indicates positive cash flow. To calculate DSCR: Determine the property’s net operating income (NOI) by subtracting operating expenses from the total rental income. Operating expenses may include property management fees,

utilities, taxes, insurance, and maintenance costs. Calculate the total debt service, which includes the principal and interest payments on the loan. Divide the NOI by the total debt service to obtain the DSCR ratio. Example: Suppose a property has an NOI of $80,000 per year and a total debt service of $60,000 per year. DSCR = NOI / Total Debt Service DSCR = $80,000 / $60,000 DSCR = 1.33 In this scenario, the property’s DSCR is 1.33, indicating that its income comfortably covers its debt payments. DSCR Loan Requirements While DSCR loans offer more flexibility than traditional financing options, there are still certain requirements that borrowers must meet to qualify. Understanding these requirements is crucial for a successful loan application. Here are the key requirements for obtaining a DSCR loan: 1. Down Payment To secure a DSCR loan, borrowers are typically required to provide a down payment of 20- 25% of the property’s purchase price. The specific down payment percentage may vary depending on the lender and individual circumstances. Having a portion of the property’s value ready as part of your investment strategy is crucial for securing financing. 2. Credit Score A good credit score is essential for qualifying for a DSCR loan. While specific credit score requirements may vary among lenders, a score of 620 or higher is generally considered favorable. Lenders assess the borrower’s creditworthiness to ensure a history of responsible financial behavior. A higher credit score can positively influence loan terms and eligibility. 3. Property Appraisal As a borrower, you must have enough cash to cover the appraisal fees for the property. While these fees can vary, opting for a direct approach can help save up to $200. The direct approach involves an appraiser compiling the necessary form as an appendix to the appraisal report for a single-family investment property. This not only reduces upfront costs but also expedites the accurate valuation process. 4. Debt Service Coverage Ratio Lenders typically require a minimum DSCR of 1 to ensure that the property generates sufficient revenue to effectively manage loan payments. Even if your DSCR falls below 1, some lenders may still finance your investment with higher interest rates and a larger down payment. However, it is generally advisable to aim for a DSCR above 1 to ensure positive cash flow. By satisfying these DSCR loan requirements, you enhance your chances of securing financing for your real estate investment and position yourself for success in the thriving property market. The DSCR Loan Application Process Embarking on the journey to secure a DSCR loan involves a series of well-defined steps. Familiarizing yourself with the application process will help you navigate it with confidence.

Here is a step-by-step guide to the DSCR loan application process: Step 1: Research and Selection Begin by researching reputable DSCR lenders specializing in DSCR loans. Explore their terms, interest rates, and track record. This initial phase is vital as it sets the tone for a successful loan application. Consider working with a trusted partner like CambridgeHomeLoan.com, a leading DSCR lender, with a proven track record of funding numerous DSCR loans. Step 2: Gather Necessary Documentation Once you have selected a lender, gather the necessary documentation required for the loan application. This includes property details, financial records related to the property, bank statements, any lease agreements, insurance documents, and entity documents if applicable. While DSCR loans have lighter documentation requirements compared to traditional loans, proper documentation remains crucial to ensure a smooth application process. Step 3: Submitting the Loan Application Submit your loan application through the lender’s designated platform. Many lenders offer online applications for convenience and efficiency, allowing you to initiate the process from the comfort of your workspace. Be thorough and accurate in providing all required information to avoid delays in the evaluation process. Step 4: Underwriting and Evaluation During this phase, the lender will conduct a thorough evaluation of your loan application. They will assess factors such as the property’s potential rental income, operating expenses, and debt service coverage ratio. The outcome of this evaluation will influence the loan offer, including the terms, interest rates, and associated fees. Step 5: Loan Offer and Acceptance Upon successful evaluation, you will receive a loan offer from the lender. This offer will detail the terms, interest rates, and any associated fees. Take the time to carefully review the terms and ensure they align with your investment goals before accepting the offer. If you have any questions or concerns, reach out to the lender for clarification. Step 6: Closing and Disbursement The closing phase involves signing the necessary paperwork and legal documents to formalize the loan agreement. This typically takes place at a title company or with a closing agent. Once the closing process is complete, the funds will be disbursed to facilitate your real estate investment. By following this step-by-step process, you can navigate the DSCR loan application process smoothly and secure financing for your real estate investment. DSCR Loan Interest Rates Interest rates play a significant role in shaping the investment success of DSCR loans. DSCR loan interest rates generally run 1-2% higher than conventional mortgages. However, it is important to note that interest rates can vary among lenders. This highlights the importance of obtaining quotes from multiple sources to secure the best possible rate for

your DSCR loan. To ensure you get the most favorable interest rate, consider the following: Maintain a strong credit score: A higher credit score can help you secure a lower interest rate. Aim to keep your credit score in good standing and address any issues that may negatively impact it. Provide a larger down payment: Offering a larger down payment can demonstrate your commitment and reduce the lender’s perceived risk. This may lead to more favorable interest rate options. Consider buying down the interest rate: Some DSCR lenders offer the option to “buy down” the interest rate by paying points upfront. This can result in a lower interest rate throughout the loan term, potentially saving you money in the long run. To ensure you secure the best interest rate for your DSCR loan, consider working with a reputable DSCR lender like CambridgeHomeLoan.com. They have a deep understanding of the real estate markets nationwide and can guide you through the loan process while helping you secure competitive interest rates. Example: Texas Real Estate Market Overview Before diving into DSCR loans in Texas, it’s important to have an understanding of the current state of the Texas real estate market. Here’s an overview of the market based on recent data: Median Home Prices: Despite economic fluctuations, Texas has displayed resilience in its median home prices. In recent months, median home prices in Texas rose by 0.3 percent, reaching an average of $337,900. This steady increase highlights the stability of the Texas real estate market. Regional Variations: Different regions within Texas experience varying levels of price growth. For example, Austin registered the most significant monthly increase, with a notable gain of 4.2 percent. This surge marked the highest price level in Austin over the past nine months. It’s important to consider regional trends when investing in Texas real estate. Homebuyer Demand: The real estate market has witnessed a decline in homebuyer demand, leading to a decrease in total home sales. In June, total home sales dropped to a level below 28,000 transactions. This decrease in demand can present opportunities for investors to find properties at potentially favorable prices. Understanding the Texas real estate market can provide valuable insights when making investment decisions. Stay up-to-date with market trends and consult with local experts to navigate the ever-changing landscape effectively. Is Now a Good Time to Invest in Real Estate? Given the current market conditions, many investors may wonder if now is a good time to invest in real estate, particularly considering the impact of all-time high interest rates. Here are a few factors to consider when making this decision: Strong Property Appreciation: Real Estate has a history of strong property appreciation, especially in growing cities and states like Austin and Houston, Florida, Maryland and Tennessee. Over time, this appreciation can contribute to significant returns on investment. Rental Income Potential: Many of these cities and states offer favorable rental income potential, especially in areas with high demand and limited supply. This can provide a steady cash flow stream for investors. Refinancing Opportunities: While interest rates may currently be high, investors have the option to refinance when rates go down. This flexibility allows investors to take advantage of lower rates, potentially reducing their overall financing costs.

Long-Term Outlook: Investing in real estate is a long-term strategy. Despite short-term fluctuations, the real estate market has historically shown resilience and steady growth over time. Ultimately, the decision to invest in real estate should be based on your individual financial situation, investment goals, and long-term plans. It’s important to conduct thorough market research, analyze potential risks and rewards, and consult with experts before making any investment decisions. DSCR Loans for Commercial Real Estate and Other Investment Types While DSCR loans are primarily associated with residential income-producing properties, they can also be utilized for commercial real estate and other investment types. Here’s an overview of how DSCR loans can apply to different investment scenarios: Commercial Real Estate: DSCR loans can be used to finance commercial properties such as office buildings, shopping centers, industrial properties, and more. Lenders evaluate the property’s income potential and operating expenses to determine loan eligibility, similar to residential DSCR loans. Short-Term Rentals: Investors involved in short-term rental properties, such as Airbnb or vacation rentals, can also benefit from DSCR loans. Lenders consider the property’s rental income and calculate the DSCR ratio accordingly. This allows investors to secure financing based on the property’s revenue-generating potential. BRRRR Method: The BRRRR method (Buy, Renovate, Rent, Refinance, Repeat) is a popular investment strategy that involves purchasing distressed properties, renovating them, renting them out, and then refinancing to repeat the process. DSCR loans can be utilized during the refinancing stage to unlock the property’s increased value. By understanding the versatility of DSCR loans, investors can explore various investment avenues and leverage the benefits of this financing option beyond traditional residential income properties. Conclusion Securing a DSCR loan can open doors to opportunities in the thriving real estate market. By familiarizing yourself with the requirements, calculations, and application process outlined in this guide, you are better equipped to embark on your investment journey with confidence. Remember, DSCR loans prioritize the property’s cash flow and profitability, making them an attractive financing option for a wide range of real estate investors. To apply today DSCR Rental Loan Application. Frequently Asked Questions Q: What is the minimum down payment required for a DSCR loan? A: The minimum down payment for a DSCR loan is typically 20-25% of the property’s purchase price. However, this percentage may vary depending on the lender and individual circumstances. Q: Do I need a good credit score to qualify for a DSCR loan? A: Yes, having a good credit score is important for qualifying for a DSCR loan. While specific credit score requirements may vary among lenders, a score of 620 or higher is generally considered favorable.

Q: Can I use a DSCR loan for commercial real estate investments? A: Yes, DSCR loans can be used to finance commercial real estate investments in Texas. Lenders evaluate the property’s income potential and operating expenses to determine loan eligibility, similar to residential DSCR loans. Q: Is now a good time to invest in real estate, given the current interest rates? A: The decision to invest in real estate should be based on various factors, including your financial situation and long-term plans. Despite high interest rates, Most Southern States have a history of strong property appreciation and rental income potential, making them an attractive market for investors. Q: Can I refinance a DSCR loan to take advantage of lower interest rates in the future? A: Yes, refinancing is an option for DSCR loans. When interest rates go down, investors can explore refinancing options to potentially reduce their financing costs and improve their cash flow. Please note that this information is intended as a general guide and should not be considered financial or investment advice. Consult with a qualified professional at CambridgeHomeLoa.com for personalized guidance and recommendations regarding your specific situation. NOW LENDING NATIONWIDE! DSCR Loan Florida DSCR Loan Maryland DSCR Lender Texas DSCR Loan Ohio DSCR Lender Tennessee https://www.cambridgehomeloan.com/dscr-loan-florida/ Call Now! 800-826-5077 Best Home Loan rates and terms in Tampa Florida Cambridge Capital 4830 West Kennedy Blvd Suite 600, Tampa, FL 33609 Home Loan Programs FHA Loans, VA Loans, USDA Loans, Zero Down Home Loans, Fix & Flip Loans, Commercial Lending, Mezz Financing