Download

1 / 24

240 likes | 407 Views

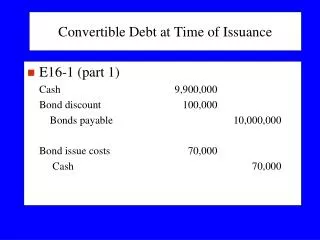

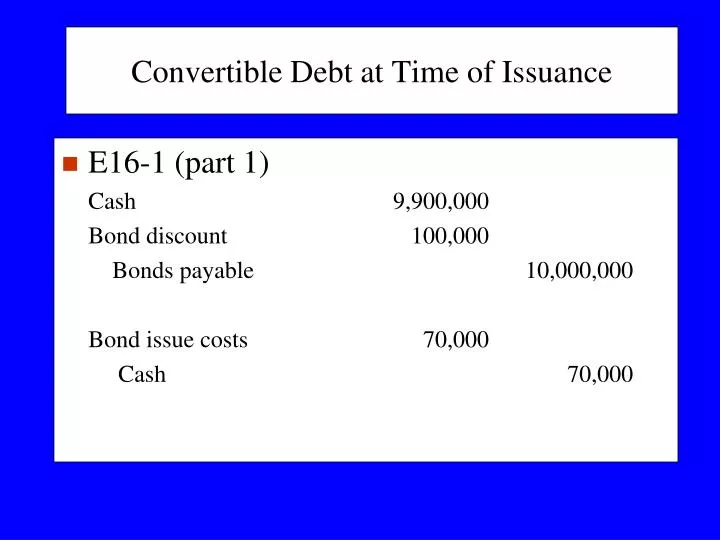

Convertible Debt at Time of Issuance. E16-1 (part 1) Cash 9,900,000 Bond discount 100,000 Bonds payable 10,000,000 Bond issue costs 70,000 Cash 70,000. Time of “Normal” Conversion. Text (p. 797) Carrying amount of bonds (book value): Bonds payable 1,000

E N D

Convertible Debt at Time of Issuance • E16-1 (part 1) Cash 9,900,000 Bond discount 100,000 Bonds payable 10,000,000 Bond issue costs 70,000 Cash 70,000

Time of “Normal” Conversion • Text (p. 797) • Carrying amount of bonds (book value): Bonds payable 1,000 Bond premium 50 1,050

Time of “Normal” Conversion Bonds payable 1,000 Premium on bonds payable 50

Time of “Normal” Conversion Bonds payable 1,000 Premium on bonds payable 50 Common stock (par value) 100 APIC (1,050 – 100) 950

Induced Conversions • Involves a “sweetner” • E16-1 (part 3)

Induced Conversions Book value of bonds: Bonds payable 10,000,000 Discount on bonds payable 55,000 9,945,000 Par value of stock 1,000,000 APIC 8,945,000 9,945,000 Debt conversion expense 75,000 Bonds payable 10,000,000 Discount on bonds payable 55,000 Common stock 1,000,000 APIC 8,945,000 Cash 75,000

Convertible Preferred Stock • Is equity - unless mandatory redeemable • Conversion is an equity transaction -- no gain or loss recognized • Book value of preferred used to record conversion

Conv. Preferred Stock – Text P. 798 Book value of preferred: Preferred 1,000 APIC – preferred 200 1,200 Preferred stock 1000 APIC – preferred 200

Conv. Preferred Stock – Text P. 798 Book value of preferred: Preferred 1,000 APIC – preferred 200 1,200 Preferred stock 1000 APIC – preferred 200 Common stock (1,000 x $2 par) 2,000

Conv. Preferred Stock – Text P. 798 Book value of preferred: Preferred 1,000 APIC – preferred 200 1,200 Preferred stock 1000 APIC – preferred 200 Retained earnings 800 Common stock (1,000 x $2 par) 2,000

Conv. Preferred Stock – Text P. 781 What if convertible into 400 shares of common? Book value of preferred: Preferred 1,000 APIC – preferred 200 1,200 Preferred stock 1000 APIC – preferred 200

Conv. Preferred Stock – Text P. 781 What if convertible into 400 shares of common? Book value of preferred: Preferred 1,000 APIC – preferred 200 1,200 Preferred stock 1000 APIC – preferred 200 Common stock (400 x $2 par) 800

Conv. Preferred Stock – Text P. 781 What if convertible into 400 shares of common? Book value of preferred: Preferred 1,000 APIC – preferred 200 1,200 Preferred stock 1000 APIC – preferred 200 Common stock (400 x $2 par) 800 APIC – common 400

Stock Warrants • Entitle holder to acquire additional shares • within a specified period • at a specified price • Typical uses • “Equity kicker” • Evidence of preemptive right of existing stockholders • Stock-based compensation for executives (stock options)

Stock Warrants (cont.) • Detachable • Proportional method (if FV of both debt and warrant determinable) • Incremental method (if FV of both not determinable) • Nondetachable • No part of proceeds allocated to warrants • See text examples pp. 800-801

Stock Warrants (cont.) • Allocated to warrants: 300,000/10,200,000 x 10,000,000 = 294,118 • Allocated to bonds: 9,900,000/10,200,000 x 10,000,000 = 9,705,882 10,000,000 Cash 9,705,882 Discount on bonds payable 294,118 Bonds payable 10,000,000 Cash 294,118 APIC - stock warrants 294,118

Stock Warrants (cont.) • What if proceeds = $9,700,000? • Allocated to warrants: 300,000/10,200,000 x 9,700,000 = 285,294 • Allocated to bonds: 9,900,000/10,200,000 x 9,700,000 = 9,414,706 9,700,000 Cash 9,414,706 Discount on bonds payable 585,294 Bonds payable 10,000,000 Cash 285,294 APIC - stock warrants 285,294

Stock Compensation Plans • Stock option plans: • incentive plans [qualified for tax purposes] • non-qualified plans • Stock appreciation rights • Performance plans

Grant date Vesting date Exercise date Expiration date Options are granted to employee Date option vests – employee must do nothing else Employee exercises options Unexercised options expire Stock Options - Important Dates Work start date

Stock Option Plans • Accounting method • Now required - fair value method (SFAS 123R) • Previously required - intrinsic value method (APBO 25)

Fair Value Method • Total compensation cost (TCC) • Fair value at grant date of options expected to vest • Allocate TCC over service period • See page 806

Stock Appreciation Rights [SARs] • SARs are designed to mitigate employee’s cash flow problems in non-qualified plans • Employee gets a right to receive any appreciation in share value at exercise date equal to market price less a pre-established amount • Employee receives cash or stock only for the appreciation.

Stock Appreciation Rights (SARs): Example • Given: • SAR program is established: January 1, 2010 • SAR exercise period: any time next five years • Pre-established price per SAR: $10 • Number of SARs granted: 10,000 • Market prices of the stock: • Dec 31, 10: $ 3; Dec 31, 11: $7; Dec 31, 12: $ 5. • Service period: 2 years (2010 - 2011) • The SARs are held for 3 years and then exercised. • Determine the compensation expense for 2010, 11, and 12.

Stock Appreciation Rights (SARs): Entries Debit Credit Dec 31, 2010 Compensation Expense $15,000 Liability for SARs $15,000 Dec 31, 2011 Compensation Expense $55,000 Liability for SARs $55,000 Dec 31, 2012Liability for SARs $20,000 Compensation Expense $20,000 Dec 31, 2012 Liability for SARs $50,000 Cash $50,000 (SARs exercised end of the third year)