Download

1 / 23

240 likes | 406 Views

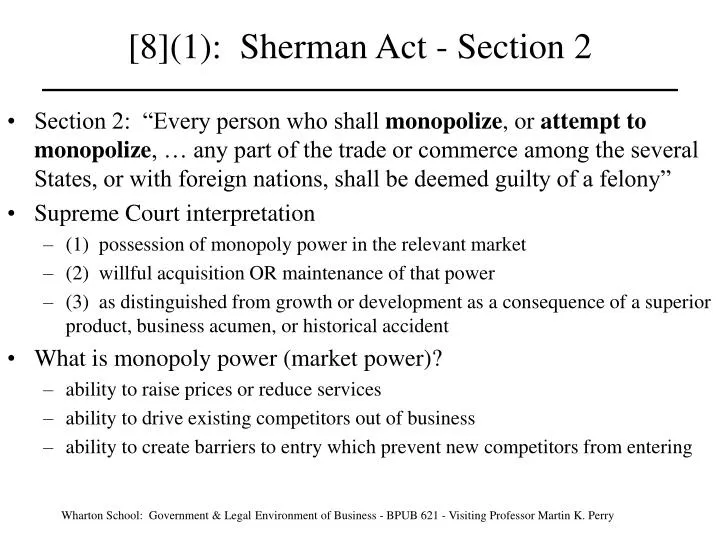

[8](1): Sherman Act - Section 2. Section 2: “Every person who shall monopolize , or attempt to monopolize , … any part of the trade or commerce among the several States, or with foreign nations, shall be deemed guilty of a felony” Supreme Court interpretation

E N D

[8](1): Sherman Act - Section 2 • Section 2: “Every person who shall monopolize, or attempt to monopolize, … any part of the trade or commerce among the several States, or with foreign nations, shall be deemed guilty of a felony” • Supreme Court interpretation • (1) possession of monopoly power in the relevant market • (2) willful acquisition OR maintenance of that power • (3) as distinguished from growth or development as a consequence of a superior product, business acumen, or historical accident • What is monopoly power (market power)? • ability to raise prices or reduce services • ability to drive existing competitors out of business • ability to create barriers to entry which prevent new competitors from entering

[8](2): Monopolization (Section 2) • What must government or private plaintiff prove? • (1) Monopoly Power in a relevant product and geographic market • very high market share, certainly over 60%, often as much as 80% • significant natural barriers to entry for new competitors • (2) Predatory or Exclusionary Practices • predatory practices harm existing competitors, possibly driving them out of business • exclusionary practices are artificial barriers to entry that prevent new competitors • (3) Practices have no legitimate business justification • Different standard to prove attempted monopolization • (1) Current market share can be much smaller, maybe as low as 30% • (2) Dangerous Probability of Success in gaining a monopoly market share • certainly over 60% • (3) Predatory Practice designed to drive existing competitors out of business

[8](3): Microsoft - Market Power • What are the product markets? • Operating systems for Intel-compatible personal computers: Windows • Internet Browsers: Netscape Navigator and Microsoft Explorer • What is the geographic market? • World-wide market, but same as U.S. market • What is Microsoft’s market share? • Operating Systems: Windows had 90% - 95% of new sales throughout 1990’s • As a result, Windows had 80% - 90% of installed base • Browser Shares: Explorer Navigator • 1995: 0% 100% • 1996: 10% 75% • 1998: 50% 50% • 2000: 60% 40%

[8](4): Microsoft - Potential Competition • What is the existing competition in operating systems? • Apple: declining share except in certain niche markets • OS/2: IBM system, died with decline in IBM PC sales • Unix (Linux): popular on networks, but not common on PCs • What is the potential competition? AOL-Netscape-Java • AOL = dominant supplier of Internet access • Navigator (Netscape) = major Internet browser • Java (Sun) = flexible programming language that allows applications software to run on any operating system • What are the barriers to entry in operating systems? • Network externalities (applications barrier to entry) • Designers write new software applications for the dominant operating system • Consumers benefit from standardized operating systems and applications

[8](5): Microsoft - Netscape Negotiations • Microsoft Offers a “special relationship” to Netscape (79-89) • Stop development of Navigator as a platform for applications software • In return, Microsoft will let Netscape have the “solutions” market for special commercial applications within Windows • In return, Netscape could control browser markets for Apple, OS/2, and UNIX • Problem: Joint Venture or Allocation of Markets? • Microsoft withholds technical information from Netscape (90-92) • Applications programming interfaces for Windows 95 were necessary for Netscape to design Navigator to work with Windows 95 • Netscape must postpone release of Navigator compatible with Windows 95 until after Windows 95 is released, and thus Netscape lost holiday sales • Problem: Legitimate Business Reason?

[8](6): Microsoft - Explorer Marketing • Microsoft starts a crash development of Explorer (133 - 135) • $100 million per year on development of Explorer • Rapid increase in developers from 5 or 6 in early 1995 to 1000 in 1999 • Microsoft includes Explorer for free with a Windows license (137) • Bundling the Explorer Internet application to the Windows operating system • Microsoft negotiates exclusive arrangements for Explorer (139 - 142) • Microsoft allows Internet Access and Service Providers (IAPs and ISPs) to distribute Explorer for free when the enroll new customers • Microsoft provides free services to IAPs and ISPs to promote Explorer exclusively instead of Navigator • AOL adopts and promotes Explorer (until acquisition of Netscape in 1998) • Microsoft pre-installs AOL access software and icon on Windows • Microsoft pays AOL a bounty for converting Netscape customers to Explorer

[8](7): Microsoft - OEMs • Contracts with OEMs for licensing Windows 95 (155 - 159) • OEMs cannot remove Explorer when pre-installing Windows • OEMs cannot remove Explorer icon • OEMs cannot modify boot sequence to load Navigator • OEMs cannot install programs to launch Navigator • Microsoft Threat to Apple Computer • Microsoft developed MAC Office for Apple PCs • MAC Office derived from its Microsoft Office • But Apple was distributing Navigator on its PCs • Microsoft threatens to discontinue development of MAC Office unless Apple exclusively distributes Explorer on its PCs • Apple agrees to distribute Explorer for its PCs

[8](8): Microsoft - Explorer Integration • Microsoft redesigns Explorer for Windows 95 in 1996 (160 - 165) • Explorer shares routines with Windows • Deleting Explorer will delete important aspects of Windows • Microsoft Integrates Explorer into Windows 98 (166 - 174) • Neither OEMs nor users can uninstall or override Explorer • Installing and using Navigator interferes with Windows functions and Microsoft applications • Integration provides no benefits to users • Windows is slower and less reliable for non-browsing applications • Compromises security by making Windows more vulnerable to viruses obtained from browsing on Explorer.

[8](9): Microsoft - Intel and IBM • Microsoft Offer to Intel and Threat (94 - 103) • Offer: Stop software development of NSP for video and graphics applications • In return: Microsoft would speed its development of similar applications • Threat: Microsoft will not support Intel’s next generation of microprocessors • Result: Intel discontinues NSP project • Microsoft Offer to IBM and Retaliation (115 - 130) • Offer: Stop promoting OS/2 and preinstall Windows 95 on at least half its PCs • In return: Microsoft would give IBM an $8 reduction in the royalty for Windows, with a yearly savings to IBM of $40-48 million • IBM rejected the offer, buys Lotus, promotes SmartSuite for office applications • Retaliation: Microsoft refuses to release master code for pre-installing Windows to IBM (until 15 minutes before formal release on August 24, 1995), even though other OEMs had received the master code on June 17, 1995 • IBM loses 1995 back-to-school sales of PCs to the other OEMs

[8](10): Microsoft - Windows Pricing Practices • Discounts and incentives in licensing Windows 95 and 98 • Compaq and Gateway received lower license fees and promotional allowances for promoting Explorer exclusively over Navigator • Other OEMs paid higher license fees for pre-installing and promoting Navigator • IBM paid the highest license fee to pre-install Windows • Pricing by PCs shipped (Settled with JD by prior consent decree) • Microsoft charges its license fee to OEMs for pre-installation of Windows on the basis of the number of PCs shipped, rather than the number of PCs with Windows installed • As a result, Windows becomes free to pre-install on all PCs • OEM is paying the license fee to Microsoft, even if it pre-installs another operating system on the PC • Installing another operating system on the PC requires the OEM to pay a license fee for the other operating system

[8](11): Microsoft - Defense • (1) No Market Power • Wider product market (include operating systems for network servers) • Actual and potential competition from existing firms (AOL-Netscape-Sun) • No barriers to entry by new firms (software designers) • Price of Windows is “low” ($89 for Windows 98, up from $49 for Windows 95) • (2) Practices are Normal Business Practices • Exclusive contracts are common for promoting products • Quantity discounts for OEMs are common for selling products • (3) Legitimate Business Reasons for Practices • Economies of integration of Windows and Explorer • Economies from standardization of operating system • compatibility and transportability of software

[8](12): Microsoft - What Remedy? • Criminal Fines: Twice the gain to Microsoft? • What would have been the price of Windows? Price of Explorer was zero!!! • Criminal penalties have been extremely rare in monopolization cases because it is never obvious what will constitute a violation of Section 2 (unlike Section 1) • Structural Remedy: Divestiture? • Horizontal: License or auction Windows source code • Problem: competition may eliminate efficiencies of standardization • Vertical: Divest Windows from all applications software (Explorer) • Problem: eliminate efficiencies from integration of software • Behavioral Remedy: Injunction? • Prohibit Microsoft from making exclusive agreements with OEMs and IAPs • Provide Windows source code for applications programming interfaces (APIs) • Problem: court supervision of a technologically dynamic industry

[8](13): Microsoft - District Court Decision • November 1999: District Court Findings of Fact • Judge defines market and characterizes practices in favor of JD • Judge postpones legal decision and urges settlement (none reached) • April 2000: District Court Conclusions of Law • Microsoft violated Section 2: invites proposals for a remedy • Justice Department proposes a remedy, Microsoft asks for more time • June 2000: District Court Judgment = Vertical Divestiture • Operating System Company (OpsCo): Windows • Applications Company (AppsCo): Explorer, Word, Excel, Office • Goal: eliminate the applications barrier to entry in operating systems • AppsCo will have an incentive to adapt and design applications for other operating systems and platforms • AppsCo will have an incentive to develop other operating systems and platforms

[8](14): Microsoft - Final Judgment • 2001: Court of Appeals Decision • Upheld violation of Section 2 for monopolization • Reversed vertical divestiture as a remedy • Remanded to a new District Court Judge for a new hearing on remedy • November 2002: Final Judgment • New District Court judge approves new settlement between Microsoft and JD • Settlement is a behavior remedy with extensive monitoring by the JD • States lawsuit against Microsoft will continue • Certain states refused to accept the settlement negotiated by the JD • Private lawsuits against Microsoft will continue • EU is also pursuing a case against Microsoft

[8](15): Behavioral Remedy • Microsoft cannot retaliate against OEMs, ISPs, or IHVs for developing or distributing other operating systems or applications software (A and F) • Microsoft must offer uniform licensing agreements to OEMs (B) • Microsoft cannot impose license restrictions on OEMs for pre-installing other software (C) • Microsoft must disclose APIs and Protocols (D and E) • Microsoft cannot enter into a large variety of exclusive contracts (G) • Microsoft must allow OEMs and users to remove and replace Microsoft applications with other competing applications (H)

[8](16): U.S. v. American Airlines (2002) • What is Predatory Pricing? • Dominant firm lowers prices until its competitors go bankrupt and exit • Dominant firm then raise prices to recoup the losses • Predation also deters future entry by other potential competitors • JD sues American Airlines for monopolizing Dallas/Ft. Worth airport • American has 70% of passenger revenue to and from Dallas/Ft. Worth airport • Predatory practices in response to entry by new airlines • AA matches the lower fares of any entrant on the routes served • AA increases the number of flights on these routes to reduce load factors of entrants • Entrants experience low load factors, no profits, so they exit or go bankrupt • AA then raises fares and reduces the number of flights on these routes • American wins at trial, not guilty of monopolization • AA did not lower its fares below its costs, or below the fares of its competitors

[8](17): Kodak Cases • What is an “aftermarket”? • Durable goods often require repair, service, or maintenance • Durable goods often require replacement parts • Durable goods often require consumable goods for their use • Eastman Kodak v. Image Technical Services (Kodak I) (1992) • Kodak refuses to sell replacement parts for its copy machines to independent service organizations (ISOs) • Kodak also prevents OEMs from selling parts to ISOs • Kodak also refuses to sell parts directly to customers who want to use ISOs • Kodak then monopolizes the service on its own copiers • Can an aftermarket be a relevant product market? • Supreme Court says YES!!! • Even if the manufacturer has no market power in the durable good!!!

[8](18): Pricing in Aftermarkets • Suppose you are trying to sell a durable good (car) • Potential customer asks about the costs of consumable goods (gas and tires), replacement parts (engine parts), and service (tuneups) • What do you want to tell him? There are cheap!!!! • Now suppose the customer has already bought the durable good • And suppose you are the only supplier of the aftermarket goods and services • What prices do you want to charge? High prices!!! Why? • Customer is “locked in” because it is costly to switch to another durable good • Now think about installed base versus new sales • How does this affect your pricing of the aftermarket goods and services? • Low prices if the new sales are much larger than the installed base • High prices if the installed base is much larger than the new sales

[8](19): Why Monopolize Aftermarkets? • Suppose you did not control the aftermarket goods and services when you introduced the durable good • You would be happy to have competitive suppliers provide them at low prices • But once the installed base of the durable good is large relative to the new sales • Revenue and profits from new sales are declining • If you controlled the aftermarkets, you could charge high prices for the aftermarket goods and services to the installed base of the durable good • Incentive to monopolize the aftermarkets in whatever way possible • Since the manufacturer often produces the replacement parts, this is a typical mechanism for monopolizing the other aftermarkets • Even if the manufacturer does not produce the parts, he often has control over the OEMs who do

[8](20): Red Lion v. Ohmeda - Markets • What is the relevant product market? • Plaintiffs argue “service on Ohmeda machines” • Defendant argues “anesthesia systems”: system include machines, consumables, parts, service, and even related monitors • What does Court decide? On summary judgment • Definition of the product market requires a trial on the facts • But court clearly indicates that it is disposed to defining a service aftermarket • film (for cameras), software (for computers), and tires (for cars) are markets • Does Ohmeda have market power in service on its machines? • Yes, Ohmeda does 71% of the service on its machines • Biomeds service another 20% and ISOs only 10% • But only 46% of service on all anesthesia machines because there is another major manufacturer of machines (Drager)

[8](21): Red Lion v. Ohmeda - Practices • Service Restricted Parts are the major parts of the anesthesia machines • Ohmeda Policy prior to 1997 • Ohmeda would not sell service restricted parts to ISOs • Ohmeda prohibited OEMs from selling service restricted parts to ISOs • Ohmeda required a “waiver of liability” from the hospital if a service restricted part was going to be installed by an ISO • ISOs could only provide service with non-service restricted parts • Ohmeda Policy after 1997 - after the lawsuit was filed • Ohmeda defined “qualified ISOs” as ISOs with a trained employee • Training for all Ohmeda machines costs at least $30,000 • Training classes are infrequent and often full (with biomeds) • Qualified ISOs receive no discounts on the parts and cannot advertise

[8](22): Red Lion v. Ohmeda - Justifications • Does Ohmeda have Legitimate Business Justifications? • (1) Protect patients from breakdowns or accidents • Does this justification require a restrictive policy toward ISOs? • Not really, it only requires training OR certification • Ohmeda could offer the training classes more often at a lower cost • ISO employees are former service employees of Ohmeda • (2) Preserve the reputation of its machines • Does this justification makes sense? • Not really, because anesthesiologists make the decisions about which machines to buy (Ohmeda or Drager) and it would usually be a simple matter to identify the cause of any accident

[8](23): Defenses in Kodak Cases • Manufacturer cannot increase the prices of aftermarket goods because he will lose sales of the durable good to other manufacturers • Customers compare “life-cycle” costs in making purchase decisions • New customers will purchase from the other manufacturers • Installed base of old customers can costlessly switch to other manufacturers • Counter arguments • Installed base is too large relative to new sales • Stronger incentive to charge high aftermarket prices • Installed base of Ohmeda machines was 10 - 15 the yearly sales • Switching by the installed base customers is not easy • Anesthesiologists have strong preferences for Ohmeda or Drager • No market for used machines - most used machines sold to developing countries • Drager has similar incentives to charge high aftermarket prices