Download

1 / 3

30 likes | 144 Views

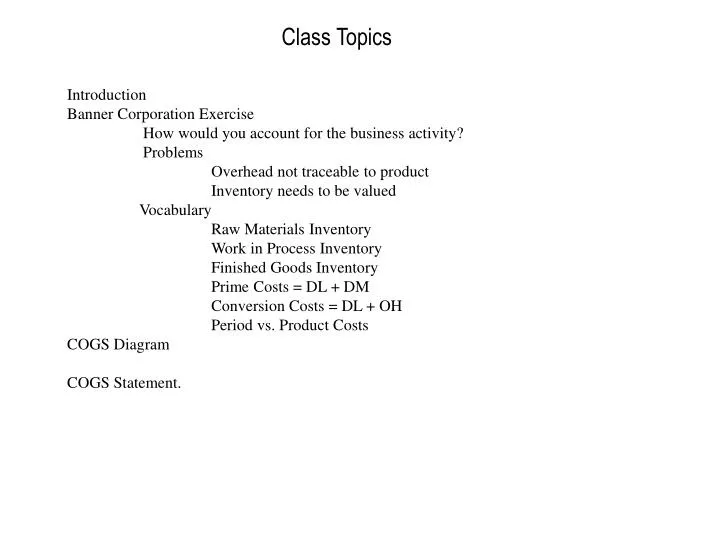

Class Topics. Introduction Banner Corporation Exercise How would you account for the business activity? Problems Overhead not traceable to product Inventory needs to be valued Vocabulary Raw Materials Inventory Work in Process Inventory Finished Goods Inventory

E N D

Class Topics Introduction Banner Corporation Exercise How would you account for the business activity? Problems Overhead not traceable to product Inventory needs to be valued Vocabulary Raw Materials Inventory Work in Process Inventory Finished Goods Inventory Prime Costs = DL + DM Conversion Costs = DL + OH Period vs. Product Costs COGS Diagram COGS Statement.

Vocabulary Product Cost: Any Cost required to get a product to finished goods (Direct Labor, MOH, DM) Period Cost: Anything that can’t be classified as a product cost (e.g. advertising) Conversion Costs: Direct Labor and Manufacturing Overhead (MOH) Prime Costs: Direct Materials and Direct Labor Allocated Costs: Costs not directly traceable to a product, service or department and allocated using some reasonable basis.

Process flow for a Cost of Goods Sold (COGS) statement Direct Labor Cost of Goods Sold (COGS) Raw Materials Inventory (RM) Work-In Process Inventory (WIP) Finished Goods Inventory (FG) Beginning Inventory Direct Materials (DM) Beginning Inventory Beginning Inventory Cost of Goods Manufactured (COGM) Purchases Ending Inventory Ending Inventory Ending Inventory Manufacturing Overhead The Calculus of COGS 1. DM = Beginning RM + Purchases - Ending RM 2. COGM = Beginning WIP + DM + Direct Labor + Manufacturing Overhead - Ending WIP 3. COGS = Beginning FG + COGM - Ending FG