Download

1 / 51

510 likes | 526 Views

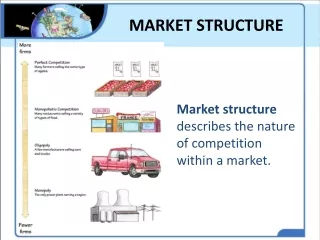

Market Structure. The number and relative size of firms in an industry. Most real-world firms fall somewhere along a spectrum that stretches from one extreme (powerless) to another (powerful). LO-1. Market Structure. Five common types of market structure: Perfect Competition

E N D

Market Structure • The number and relative size of firms in an industry. • Most real-world firms fall somewhere along a spectrum that stretches from one extreme (powerless) to another (powerful). LO-1

Market Structure Five common types of market structure: • Perfect Competition • Monopolistic Competition • Oligopoly • Duopoly • Monopoly LO-1

Competitive Firm • A perfectly competitive firm is one without market power. • It is not able to alter the market price of the good it produces. • It is a price taker. • It competes with many other firms selling homogenous products. LO-1

Competitive Market • A competitive market is one in which no buyer or seller has market power. • No single producer or consumer has any control over the price or quantity of the product. LO-1

Monopoly • A monopoly firm is one that produces the entire market supply of a particular good or service. • It is a price setter, not a price taker. • It has no direct competitors. • It has complete market power; it can alter the market price of a good or service. LO-1

Imperfect Competition • Other forms of imperfect competition lie between the extremes of monopoly and perfect competition. • Duopoly: only two firms supply a product. • Oligopoly: a few large firms supply all or most of a particular product. • Monopolistic competition: many firms supply essentially the same product but each enjoys significant brand loyalty. LO-1

Perfect Competition • Perfectly competitive firms are pretty much faceless. • They have no brand image, no real market recognition. • A perfectly competitive firm is one whose output is so small in relation to market volume that its output decisions have no perceptible impact on price. LO-1

No Market Power • The output of a lone perfectly competitive firm is so small relative to market supply that it has no significant effect on the total quantity or price in the market. LO-1

Price Takers • A perfectly competitive firm is a price taker. • An individual firm’s output decisions do not affect the market price. • An individual firm must take the market price and do the best it can within these constraints. LO-1

Market Demand versus Firm Demand • We must distinguish between the market demand curve and the demand curve confronting a particular firm. • The market demand curve for a product is always downward-sloping. • The demand curve facing a perfectly competitive firm is horizontal. LO-1

The Firm’s Production Decision • Choosing a rate of output is a firm’s production decision: • It is the selection of the short-term rate of output (with existing plant and equipment). LO-1

Output and Revenues • Total revenue is the price of a product multiplied by the quantity sold in a given time period: Total revenue = price x quantity LO-2

Revenues versus Profits • Profit is the difference between total revenue and total cost. • Maximizing output or revenue is not the way to maximize profits. • Total profits depend on how both revenue and cost increase as output expands. • A business is profitable only within a certain range of output. LO-2

Profit Maximization and Price • To maximize profit, the firm should produce an additional unit of output only if it brings in revenue that is greater than the cost of producing it. • Since competitive firms are price takers, they must take whatever price the market has determined for their products. LO-3

Profit-Maximizing Rate of Output • Never produce anything that costs more than it brings in – it boils down to comparing price and marginal cost. • A competitive firm wants to expand the rate of production whenever price exceeds marginal cost. • Short-run profits are maximized at the rate of output where price equals marginal cost. LO-3

Price > MCIncrease output rate • Price = MCMaintain output rate (Profits maximized) • Price < MCDecrease output rate Short-Run Decision Rules for a Competitive Firm LO-3

Total Profit • Total profit can be computed in one of two ways: Total profit = total revenue – total cost OR Total profit = average profit (profit per unit) x quantity sold LO-3

Total Profit • Profit per unit equals price minus average total cost: Profit per unit = p – ATC LO-3

Total Profit • Total profit equals profit per unit times quantity: Total profit = (p – ATC) x q LO-3

Total Profit • The profit-maximizing producer doesn’t seek to maximize per-unit profits. • The profit-maximizing producer has no particular desire to produce at that rate of output where ATC is at a minimum. • Total profits are maximized only where p = MC. LO-3

Supply Behavior • How firms make production decisions helps explain how the market establishes prices and quantities. • Supply is the ability and willingness to sell specific quantities of a good at alternative prices in a given time period. LO-4

A Firm’s Supply • Competitive firms adjust the quantity supplied until MC = price. • The marginal cost curve is the short-run supply curve for a competitive firm. LO-4

Supply Shifts • Marginal costs determine the supply decisions of a firm. • Anything that alters marginal cost will change supply behavior. LO-4

Supply Shifts • Important influences on marginal cost (and supply behavior) are: • The price of factor inputs • Technology • Expectations LO-4

Market Supply • Market supply is the total quantity of a good that sellers are willing and able to sell at alternative prices in a given time period, ceteris paribus. • The market supply curve is the sum of the marginal cost curves of all the firms. LO-4

Competitive Market Supply • Determinants of the market supply of a competitive industry: • The price of factor inputs • Technology • Expectations • The number of firms in the industry LO-4

Industry Entry and Exit • To understand how competitive markets work, we focus on changes in equilibrium rather than on a static equilibrium. • The number of firms in a competitive industry is not fixed. • Industry entry and exit is a driving force affecting market equilibrium. LO-5

Entry • Additional firms will enter the industry when profits are plentiful. • Economic profits attract firms. • More firms enter the industry. • The market supply curve shifts to the right. • The price decreases. • Industry output increases and price falls when firms enter an industry. LO-5

Tendency Toward Zero Economic Profits • New firms continue to enter a competitive industry so long as profits exist. • Once price falls to the level of minimum average cost, all economic profits disappear. LO-5

Tendency Toward Zero Economic Profits • Entry is the force driving down market prices. • Price falls until there are no economic profits. • At that point, average total cost is at a minimum. LO-5

Exit • Firms exit the industry when profit opportunities look better elsewhere. • Firms leave the industry if price falls below average cost. • As firms exit the industry, the market supply curve shifts to the left. LO-5

Exit • Price rises until there are no economic losses. • At that point, average total cost is at a minimum. LO-5

Equilibrium • The existence of profits in a competitive industry induces entry. • The existence of losses in a competitive industry induces exits. LO-5

Long-Run Equilibrium • In long-run competitive market equilibrium: • Price equals minimum average total cost. • Economic profit is eliminated. • As long as it is easy for existing producers to expand production or for new firms to enter an industry, economic profits will not last long. LO-5

Low Barriers to Entry • There are no significant barriers to entry in competitive markets. • Barriers to entry are obstacles that make it difficult or impossible for would-be producers to enter a market, like patents. LO-1

Characteristics of a Competitive Market • Many firms • Identical products • Low entry barriers • MC = p • Zero economic profit • Perfect information LO-1

The Relentless Profit Squeeze • The unrelenting squeeze on prices and profits is a fundamental characteristic of the competitive process. • The market mechanism works best in competitive markets. • Market mechanism – the use of market prices and sales to signal desired outputs. LO-1

Maximum Efficiency • Competitive pressure on prices forces suppliers to produce at the least possible cost. • Society gets the most it can from its available scarce resources. LO-1

Zero Economic Profits • All economic profits are eliminated at the limit of the competitive process. LO-5

The Social Value of Losses • Economic losses are a signal to producers that they are not using society’s scarce resources in the best way. LO-5

Policy Perspective • Competitive markets present a strong argument for laissez faire. • Government should promote competition because markets do a good job of allocating resources. • This means keeping markets open and accessible to new entrants by dismantling entry barriers. LO-1