Download

1 / 18

180 likes | 598 Views

Technical Barriers Facing Philippine Exporters. Case Study of Electronics and Garments Exports. John Lawrence Avila University of Asia and the Pacific, Philippines. Marine Products - 1%. Construction Materials - 0.49%. Forest Products - 10%. Home Furnishings - 1%. Others - 2%.

E N D

Technical Barriers Facing Philippine Exporters Case Study of Electronics and Garments Exports John Lawrence Avila University of Asia and the Pacific, Philippines

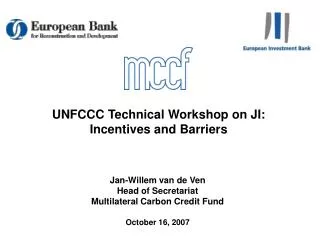

Marine Products - 1% Construction Materials - 0.49% Forest Products - 10% Home Furnishings - 1% Others - 2% Motor Vehicles and Parts - 1.74% Food - 2.9% Giftwares - 0.45% Wearables - 0.16% Organic Products - 0.18% Other Manufactured Products – 10% Machinery and Transport - 4.4% Mineral Products - 2.1% Garments and Textiles - 6% Others - 13% Agro-Based 49% Garments - 7% ELECTRONICS - 3% Mineral Products -18% ELECTRONICS 66% 1976 2005 From coconuts to chips

% TO TOTAL RP EXPORTS TOP 5 EXPORTS 2005 • ELECTRONICS 66 % • GARMENTS 6% • 3.Agro-Based & • Processed Food 6% • 4. Machinery & • Transport 4% • Forest/Mineral • Products 2% • 6. Others 16% Source: BETP/DTI

Exports grew at average 17%, 1995-2005 Electronics exports stood at around USD 27.3 billion in 2005.

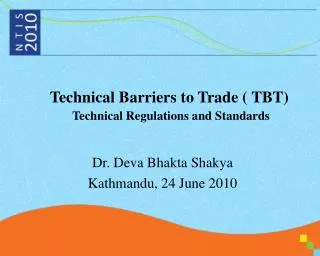

Over 60% goes to East Asian region EUROPE - 19% US$ 5.1 Billion CHINA - 13% US$ 3.5 Billion USA - 13% US$ 3.3 Billion JAPAN - 18% US$ 4.8 Billion OTHER ASIA - 37% US$ 10.6 Billion Hongkong - US$ 2.8 B Singapore - US$ 2.1 B Malaysia - US$ 2.1 B Taiwan - US$ 1.4 B Korea - US$ 1.0 B Others - US$ 1.2 B Source: Bureau of Export Trade Promotion, DTI

CLASSIFICATIONOF THE ELECTRONICS INDUSTRY PHILIPPINE ELECTRONICS INDUSTRY ELECTRONIC DATA PROCESSING Personal Computers, Hard Disk Drives, Floppy & Zip Drives, CD ROM, Motherboards, Software Development, Data Encoding and Conversion, Systems Integration Customization COMPONENTS AND DEVICES (SEMICONDUCTOR) Pentium III, DSPs, Integrated Circuits, Transistors, Diodes, Resistors, Coils, Capacitors, Transformers, Lead Frames, PCB CONSUMER ELECTRONICS TV Sets, Electronic Games, Radio Cassette Players, Karaoke Machines, Radio Cassette, Recorder TELECOMMUNICATIONS Telephones, Pagers, VHF,UHF Radios, Cellular Phones, Scanners, Satellite Receivers OFFICE EQUIPMENT Photocopy Machines and Parts, Electronic Calculators COMMUNICATIONS AND RADAR Pagers, CCTV, Radar Detectors, Marine and Land Mobile Radios, CB Transceivers CONTROL & INSTRUMENTATION PCB Assembly for Instrumentation Equipment MEDICAL AND INDUSTRIAL Spiro Analyzers, Smoke Detectors AUTOMOTIVE ELECTRONICS Electronics Brake Systems (EBS), RC Systems, Car Radios, Wiring Harness Source: Masterplan for Philippine Electronics Industry 1998

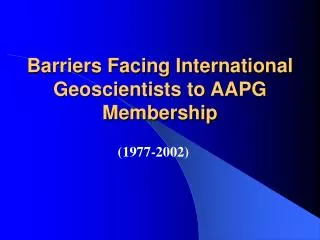

SMS – 74% COMPONENTS AND DEVICES - 74.03% EMS – 26% COMPUTER REL.PROD./EDP – 20.17% CONSUMER ELECTRONICS – 2.07% AUTOMOTIVE ELECTRONICS – 1.45% COMMUNICATIONS AND RADAR – 0.98% OFFICE EQUIPMENT – 0.70% TELECOMMUNICATIONS – 0.59% CONTROL & INSTRUMENTATION – 0.06% MEDICAL AND INDUSTRIAL – 0.03% Exports are mostly parts and components EMS 26% SMS 74% Source: Masterplan for Philippine Electronics Industry 1998

SEIPI Industry Standards ISO 9000 Certified, member of International Electrotechnical Commission (IEC) Observes best known methods in manufacturing (JIT,TQM, 5S, QPIC) Capabilities Range from IC Packaging, PCB Assembly, Full Product Assembly Lead in ASEAN Electronics Forum and ACCI Electronics committee Promotes harmonization of safety and EMC standards in ASEAN Participates in MRAs for Electrical and Electronic products testing and certification

Others Malaysia 8% 2% Singapore 2% 883 Firms Philippines Taiwan 28% 4% NATIONALITY: 72% Foreign 28% Filipino Europe 7% US 9% Korea Japan 10% 30% DOMINATED BY MNCs Exports are mostly intra-industry trade Sources: Philippine Board of Investments (BOI) & Philippine Economic Zone Authority (PEZA)

Garments Exports ASEAN: USD 19m CHINA: USD 4.4m JAPAN: USD 58m KOREA: USD 3.7m EAST ASIA: USD 104m United States: USD 1,737m

Industry profile • Predominantly Filipino-owned SMEs • Import-dependent, sourcing over 80% of their textile requirement (polyester fiber, cotton, rayon, and acrylic) from abroad • Extensive sub-contracting practice stemming from relations fostered by MFA regime (particularly for US market) • Philippine firms part of triangle manufacturing

Standards issues for garments • Subject more to fashion trends and less on government regulations • Standards a function of sub-contracting arrangements and branding • Conformity assessment costs usually assumed by buyer • Social and labor standards imposed on those seeking access to US markets • ROO and licensing issues more prominent

Summary • Standards not a serious trade impediment • Impact on standards is a function of buyer-driven model, i.e. specification of inputs is determined by foreign buyers • Garments and electronics part of global production network • AFTA is not a natural export destination for Philippine garments and electronics