Download

1 / 23

230 likes | 235 Views

INTERNATIONAL MONETARY FUND Jordan: Fiscal Sustainability and Debt Dynamics. Ahsan Mansur Advisor Middle Eastern Department June 18, 2003. I. Introduction. Twin perspectives on fiscal policy:

E N D

INTERNATIONAL MONETARY FUNDJordan: Fiscal Sustainability and Debt Dynamics Ahsan Mansur Advisor Middle Eastern DepartmentJune 18, 2003

I. Introduction Twin perspectives on fiscal policy: • To provide vital public services and social safety net while limiting distortions to the real economy through efficient and equitable taxation and non-interference with price signals; and dampening economic cycles through countercyclical policies • To ensure fiscal and public debt sustainability and, thereby, support and build sovereign creditworthiness and market confidence

II. Measures of SustainabilityA. Theoretical Perspectives Fiscal policy may be viewed as sustainable if it can be maintained indefinitely without leading the government into insolvency: • The current stock of debt must be offset by the net present value of future budget surpluses • Requires a medium-term framework in which primary surpluses finance interest costs given growth, inflation, and exchange rate assumptions ******* Two key conditions for debt sustainability: • Primary fuscal balance—defined as the fiscal balance excluding interest payments-- to be in surplus; or • Nominal GDP growth rate higher than the effective nominal interest rate on the public debt over the long run

II. Measures of SustainabilityA. Theoretical Perspectives We can calculate the level of primary balance, p, needed to hold the net debt ratio, d, constant given actual rates of real GDP growth, y, inflation, , and the effective interest rate on public debt, i: where is the velocity of base money (nominal GDP divided by base money).

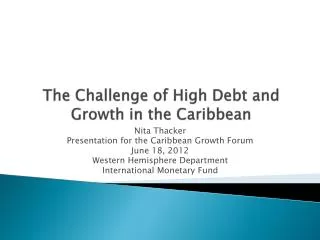

International Comparaison:Summary Indicators of Fiscal Policy 1990–2001

II. Measures of SustainabilityB. Market Perspectives The markets generally view fiscal policy as sustainable based on (i) whether debt ratios are in line with those of peer sovereigns; (ii) capacity to pay; and (iii) debt dynamics i.e., stable or falling debt and debt service burden: • The time horizon for credit ratings is three-to-five years, which is much shorter than that of the theoretical long-run solvency criterion • Capacity to pay is often measured by determining debt service in relation to GDP; revenue; and exports of goods and services (for external debt). Rollover issue is also important for cetain countries. • The market approach reflects difficulties in predicting economic and fiscal performance over the long run, and relies on stress testing

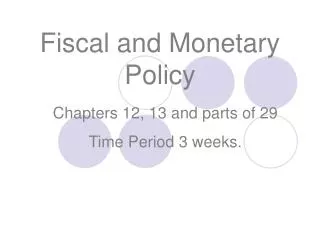

International Trends in Debt Burdens Average 2001

International Trends in Debt Burdens Average 2001

III. The Case of JordanA. Achievements in Review Jordan has halved its central government debt ratios in the space of a decade: • The debt-to-GDP ratio has been brought down from 200 percent in 1990 to 101 percent in 2002 • The debt-to-exports ratio has been brought down from 317 percent in 1990 to 222 percent in 2002

III. The Case of JordanA. Achievements in Review Four factors have contributed to the substantial debt reduction: • Sustained fiscal consolidation, with the overall deficit (after grants) having been constrained to an average of 3.4 percent of GDP in 1993–2002 • Ongoing economic growth, with the annual growth rates of real and nominal GDP having averaged 4 percent and 6.2 percent, respectively, in 1993–2002

III. The Case of JordanA. Achievements in Review • Active below-the-line debt operations under the aegis of: • six Paris Club agreements; • Brady bond buybacks; debt-for-development swaps; • debt write-offs having contributed a cumulative 24 percent of GDP toward debt reduction in 1992–2002 • Privatization, which has raised cumulative proceeds equivalent to 8 percent of GDP in 1998–2002, most of which has been used for debt reduction

III. The Case of JordanA. Achievements in Review Public debt servicing poses no problems now: • External debt service (commitment basis) amounted to 19 percent of exports in 2002, while total interest payments amounted to 13 percent of budgetary revenues (including grants) • The absence of short term external debt (by original maturity) precludes external rollover risk • Jordan’s July 2002 Paris Club agreement provides for the rescheduling of about $1.3 billion of debt service obligations on pre-cutoff date bilateral debt falling due in the period to end-2007; so, debt service on a cash basis was much less

III. The Case of JordanB. Challenges for the Future Jordan’s medium-term debt strategy aims to build on progress already made, and will continue to have six key elements: • Zero recourse to short term external borrowings • Zero recourse to external market borrowings of any sort • Accelerated privatization, with the bulk of the proceeds to be earmarked for debt reduction

III. The Case of JordanB. Challenges for the Future • Further fiscal consolidation, with the fiscal deficit (after grants) to be maintained in the range of 3–4 percent of GDP, supported by ongoing tax reforms and expenditure control • Greater reliance on domestic borrowing, in order to accelerate the reduction of external debt, soak up excess domestic liquidity, and create a domestic bond market and yield curve • Avoid macroeconomic crises through proper macroeconomic management

IV. Conclusion Fiscal and public debt sustainability is hard won but easily squandered: • Jordan has made good progress in fiscal consolidation and debt reduction, and debt servicing is now not a problem • But the public debt burden, and its external component in particular, remains high, constraining Jordan’s sovereign credit ratings to within the speculative grade • Meeting the debt-reduction targets under the Public Debt Management Law 2001 (80 percent of GDP for total debt and 60 percent of GDP for external debt by 2006) will require sustained fiscal effort, but the payoffs can be substantial