Download

1 / 9

90 likes | 145 Views

There was a time when we use to carry bunch of cash for shopping, watching movies, dining at restaurant and many other things. Thanks to the arrival of Debit/Credit card they made the payment easy, now instead of carrying bunch of cash now we have to just carry a small card.

E N D

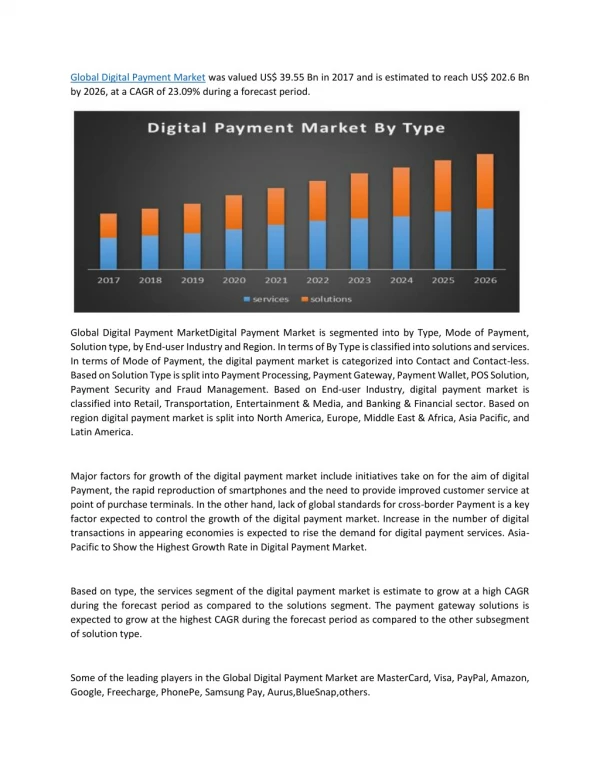

Unified Payment Interface: A new face of Digital Payment? There was a time when we use to carry bunch of cash for shopping, watching movies, dining at restaurant and many other things. Thanks to the arrival of Debit/Credit card they made the payment easy, now instead of carrying bunch of cash now we have to just carry a small card. Then came the digital wallet and they made our smartphone the payment mechanism by storing the Card details virtually and made our smart phone smarter. But a few weeks earlier RBI governor Raghu Ram Rajan announced the arrival of Unified Payment Interface. A new app that will make the payment hassle free and reduce your time for making payment for almost anything and allows you to pay from Rs.50 to Rs.1lac at the tip of your finger. So what is UPI? How will it affect our daily life? Is it a replacement for Digital Wallet? Let’s find out.

What is UPI? Unified Payments Interface (UPI), is the advanced version of Immediate Payment Service (IMPS) — a round-the-clock funds transfer service. Yes we do have NEFT and RTGS but, In National Electronic Funds Transfer (NEFT), money transfers are made via electronic messages. The bank details of the sender and the beneficiary are linked using bank branch name and IFSC code. The process typically takes a little more than an hour and is available only during the bank’s working hours. Unlike NEFT, in Real Time Gross Settlement (RTGS), fund transfers handled on one-to-one basis. Large value transactions, typically over Rs. 2 lakhs, are carried out using this method. This is also done during working hours.

But IMPS is a more recent form of fund transfer in which a user is given a 7 digit MMID (Mobile Money Identifier) whenever one has to make the payment we just need the other persons MMID and registered mobile number. And this service works 24*7. So why UPI? Well everything needs to be upgraded and so does RBI has launched this service to provide flexibility in making payment and removing the cumbersome process of transferring money. For EX: if you need to make online payment you need to add your Card details, IFSC code, than generate OTP. Even if you use digital wallet like Paytm you need to first add the Card details into your phone and then transfer some amount to digital wallet from your bank account. But UPI eliminates all this.

How it works? 1. You need to have a bank account and a smartphone. 2. Download the UPI app of a bank from playstore/appstore. Create a unique ID. 4. Generate a mobile Pin. 5. All set to rock n roll. Imagine you have to pay your Doodhwala’s monthly bill.Instead of handing over the cash, you tell your virtual identity to the Doodhwala. The Doodhwala generates a request through UPI, you approve it using your mobile phone and the payment is made! Simple as it looks!

A virtual identity is just like email, every one’s email is different from each other so no confusion and wrong transfer of payment. It could be your email, phone number, name etc. For example of you choose your phone number as virtual identity than it will be like 1234567890@sbi (If your bank is sbi) or 1234567890@axis (If your bank is axis). You can have multiple virtual address for multiple account in different bank. The UPI can also be used for shopping online instead of entering your debit card number, expiry date, and CVV code, followed by waiting for the OTP, you'd just enter your UPI ID, and get an alert on your phone to verify the transaction.

Ten major banks — Axis, SBI, Canara Bank, BOI, ICICI Bank, HDFC Bank, Punjab National Bank, Bank of Baroda, HSBC, and Citi Bank — are integrating the interface with their mobile apps. “29 banks had concurred to provide Unified payment interface service to their customers. We are confident that several banks will join UPI this year and the number will multiply further,” said A. P. Hota, MD & CEO, NPCI.This will definitely improve the digital economy and will decide the future of cashless payment. A very innovative and great step by the RBI. Well I hope I have covered all the points regarding UPI, but than also if you are confused you can comment below. Till next post stay updated. Source: [http://bit.ly/2jYoNTr]

Follow Us On https://www.facebook.com/axisbank https://plus.google.com/+axisbank http://twitter.com/axisbank https://www.youtube.com/axisbank https://www.instagram.com/axis_bank/ https://www.linkedin.com/company-beta/162609?pathWildcard=162609

Click to know more on“Unified payment interface” https://play.google.com/store/apps/details?id=com.upi.axispay