Download

1 / 18

180 likes | 186 Views

This article explores how inflation affects existing and new development real estate differently. It covers the short-term impact on financing costs and the costs of goods and services, as well as the long-term impact of excess demand and new incentives to develop. It also discusses the three elements that protect real estate parcels from cyclical vagaries: strength of the market, nature of lease contracts, and financing rates and terms.

E N D

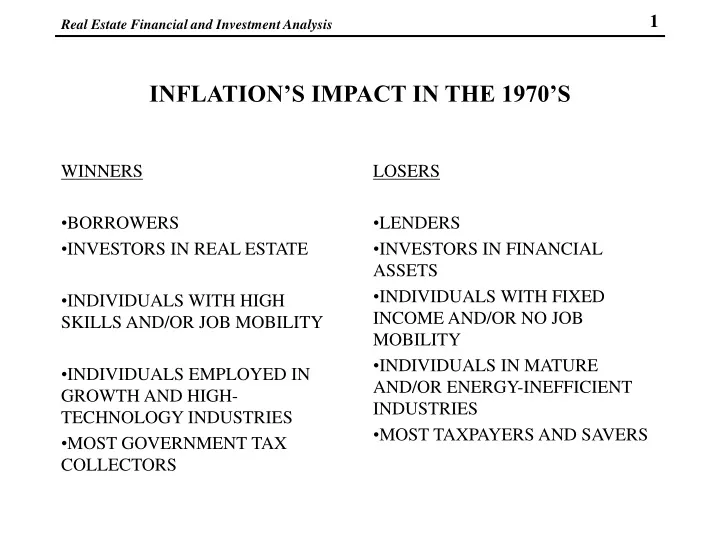

WINNERS BORROWERS INVESTORS IN REAL ESTATE INDIVIDUALS WITH HIGH SKILLS AND/OR JOB MOBILITY INDIVIDUALS EMPLOYED IN GROWTH AND HIGH-TECHNOLOGY INDUSTRIES MOST GOVERNMENT TAX COLLECTORS LOSERS LENDERS INVESTORS IN FINANCIAL ASSETS INDIVIDUALS WITH FIXED INCOME AND/OR NO JOB MOBILITY INDIVIDUALS IN MATURE AND/OR ENERGY-INEFFICIENT INDUSTRIES MOST TAXPAYERS AND SAVERS INFLATION’S IMPACT IN THE 1970’S

WHY MAY INFLATION AFFECT EXISTING AND NEW-DEVELOPMENT REAL ESTATE DIFFERENTLY? • SHORT-RUN IMPACT • COSTS OF FINANCING • COSTS OF GOODS AND SERVICES • INTERMEDIATE IMPACT • VACANCY RATES FALL • RENTS INCREASE • LONGER RUN IMPACT • EXCESS DEMAND • NEW INCENTIVES TO DEVELOP • CYCLICAL SWING BACK (MAY OCCUR)

THREE ELEMENTS TO PROTECT REAL ESTATE PARCELS FROM CYCLICAL VAGARIES: • STRENGTH OF REAL ESTATE MARKET • NATURE OF LEASE CONTRACTS • FINANCING RATES AND TERMS

IMPACT OF INFLATION, BY LAND USE • URBAN LAND • AGRICULTURAL AND FOREST LAND • RESIDENTIAL PARCELS - OWNER - OCCUPANT UNITS - MULTI-FAMILY PARCELS • COMMERCIAL SPACE

INFLATION AND MACRO-CYCLES AND REAL ESTATE INVESTMENT STRATEGIES • LONG CYCLES • WENZLICK • CASE • SHORT CYCLES • CONSTRUCTION CYCLES • MORTGAGE AVAILABILITY CYCLES • OTHER CYCLES • URBAN AREA / CITY CYCLES • NEIGHBORHOOD CYCLES • PROPERTY-SPECIFIC CYCLES • NEW CONCEPT / OVERKILL • HOT MARKET / OVERKILL

ECONOMIC RISKS RELATE TO THE EXTENT INFLATION IS PROPERLY ANTICIPATED VERSUS UNANTICIPATED

IMPORTANT INFLATION RELATED CONCEPTS • ANTICIPATED VS. UNANTICIPATED INFLATION • RELATIVE REAL RATE OF RETURN AMONG VARIOUS ASSETS - REAL ECONOMICS - TAX EFFECTS

EXPECTED INFLATION, REAL AND NOMINAL INTEREST RATES, AND CAPITAL MARKET EQUILIBRIUM • A CHANGE IN THE EXPECTED RATE OF INFLATION MAY CHANGE THE REAL RATE OF INTEREST • CHANNELS FOR THE CHANGE IN THE REAL RATE OF INTEREST ARE: - INCOME SAVINGS EFFECTS - WEALTH EFFECTS • NOTE: THERE MAY BE DIFFERENCES IN SHORT RUN VERSUS LONG RUN IMPACTS OF CHANGES IN INFLATION.

LENDER RETURN UNDER INFLATION: EXAMPLE • ASSUME: • DESIRE 2% REAL RETURN AFTER TAXES • IF NOMINAL RATE IS 12% AND THE EXPECTED INFLATION RATE IS 10%, WHAT IS THE REAL RETURN FOR THE LENDER? • LENDER IS IN 50% TAX BRACKET

INFLATION AND DEPRECIATION: THE FIRM • NET AFTER TAX REAL REVENUE FROM INVESTMENT PROJECT • = (1 - TAX RATE) X (SALES REVENUE - PRODUCTION COSTS) • NOTE: • GENERAL INFLATION HAS NO REAL IMPACT IN PRINCIPLE! • BRACKET CREEP CHANGES CONCLUSION • DEPRECIATION EFFECT ALTERS INCENTIVE TO INVEST • In sum, the firm will require a lower real rate of return (i.e., and cost of financing) if high inflation persists. Hence, as inflation increases, nominal interest rates must rise less than the change in the inflation rate.

INFLATION AND DEPRECIATION • INSERT