Download

1 / 15

160 likes | 393 Views

Auto Insurance. Note Information in this presentation is derived from Insurance for Dummies by Jack Hungelmann . I highly recommend this book. Auto Insurance Policy Categories. Liability Coverage (injury and property) Medical Payments (for you)

E N D

Auto Insurance Note Information in this presentation is derived from Insurance for Dummies by Jack Hungelmann. I highly recommend this book.

Auto Insurance Policy Categories • Liability Coverage (injury and property) • Medical Payments (for you) • Collision and Comprehensive (your vehicle) • Uninsured/Under-insured

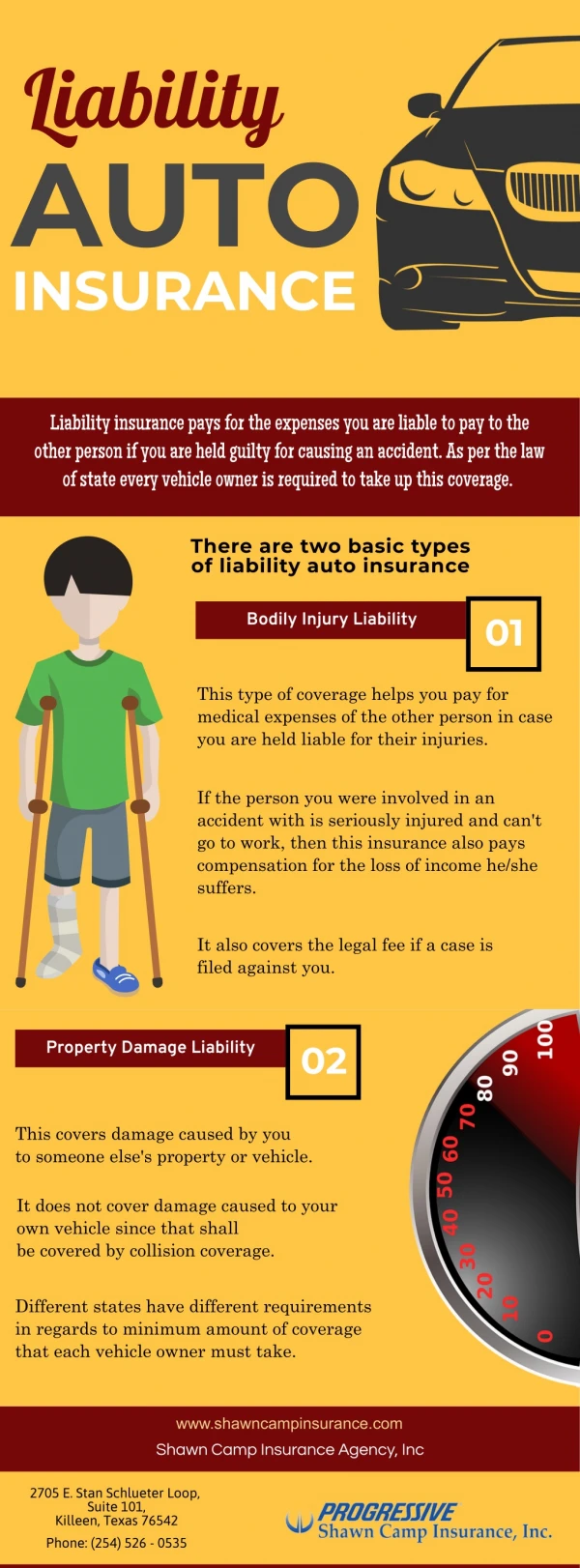

Auto: Liability Insurance Covers • Lawsuits: suability factor is important • pays for your defense • legal judgments • Lost wages • Pain and suffering • Medical Expenses

Auto: Liability ExampleYou hit a ____ who is hurt, misses one year of work

So, if you have a high suability factor. . . . . . consider buying an Umbrella Policy (discussed in another clip)

Auto: Medical Payments for YouInsuring Your Personal Injuries Bottom line: Medical and Disability should be covered using other medical and disability insurance, not auto insurance SO Buy what the law requires

Collision and ComprehensiveInsuring Against Damage to Your Vehicle • Collision: covers damage caused from colliding with another object (often another vehicle), regardless of fault • Comprehensive: other accidental damage such as fire, theft, vandalism, glass breakage, hail.

Collision and Comprehensive, cont’d • Both require a deductible • General rule: Embrace as large of a deductible as you can financially and emotionally handle

Determining Your Deductible, Example Using Collision Insurance, 4 Year Payback

When Should You Drop Collision and Comprehensive? • Use the same logic as determining your deductible • Cannot drop if you have a loan on the vehicle

Uninsured and Under-Insured Motorist Treat this like liability insurance you buy for the person who hits you who doesn’t have insurance or doesn’t have enough insurance or hits you and runs. Logically, you should buy as much uninsured/under-insured coverage as you buy liability insurance.

Saving Money on Car Insurance • Buy a safe vehicle- test crash results www.iihs.org • Choose high collision and compr. Deductibles • Keep a clean driving record • Maintain a high credit score • Insure your car and home with the same company • Don’t submit small claims on property damage • Study– G.P.A of 3.0 or greater