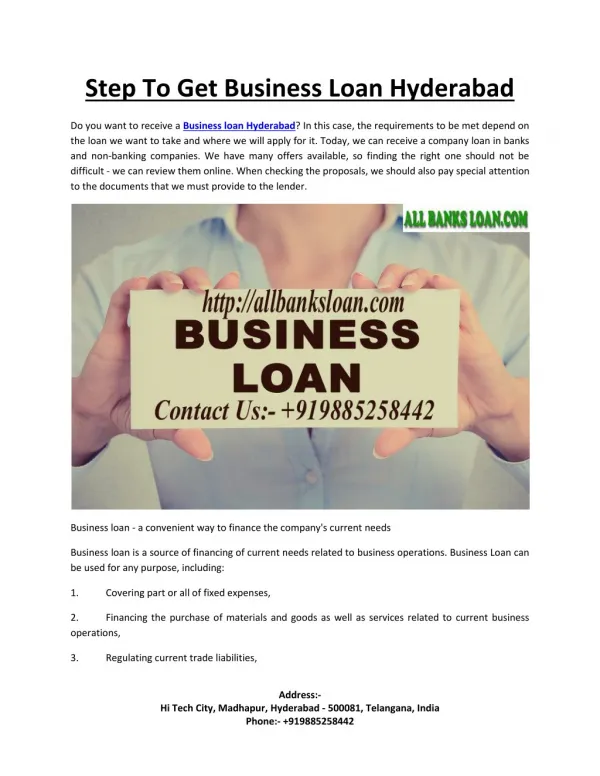

Download

1 / 12

120 likes | 125 Views

Check out the presentation titled: Which Business Loan Option is Right for You? Brought to you by Moula - https://moula.com.au/business-loan-calculator . Moula was founded to help hard-working business owners in Australia access the funding they need to grow. In the past, getting funding meant going through weeks of paperwork, hassle, and hurdles. We use data to assess your loan application, which means we can keep things painless and lightning-speedy. <br><br>With Moula, you can apply online with no paperwork and no hassle, and have the funds in your account the next day. For more info, check out: https://moula.com.au today.

E N D

Business Loan Option • You can have all the right ingredients for a successful business, including the right product or service, excellent customer service and effective marketing that generates revenue. • Although it might seem like all the pieces are in place, not having the right business loan option for your business can mean the difference between success and failure. • Understanding the business loan options will help you make the right decision when you’re looking for funds to help you when you are in a tight spot or need money to grow.

Check out the business loan option that might be right for you:

Business Credit Cards • For a small or new business, a business credit card is usually the easiest form of finance to obtain. • A bank might start you on a lower limit – such as $5,000 – and raise this over time. One of the major drawbacks of using a business credit cards is the high interest rate charged. • If you make regular payments on time, you might be offered regular increases on your limit. With a higher limit, you might take on more debt than you are able to repay.

Business Overdraft • If you have been with a bank for a while and have a good credit rating, you will probably be eligible for a business overdraft as a business loan option. If you are accepted for a business overdraft, it simply means you can run a negative balance on your account. You will be charged interest based on the outstanding negative balance on your account. In addition, there’s usually a set-up fee and ongoing fees for a business overdraft. • A secured business overdraft is usually required when the credit limit is higher. In addition, since the loan is secured there is less risk for the lending institution the interest rate for a secured overdraft is lower. Common forms of security include residential and commercial property. • Although it’s relatively easy to get a business overdraft, one of the major drawbacks is that it can be recalled by the bank at any time. This means you may be required to pay the outstanding amount immediately. Even if you have an unsecured overdraft, your personal assets may be at risk if you are unable to pay the loan, so this could be a risk business loan option for you.

Business Term Loan • Business term loans are a common form of business loan option when loan amounts are over $20,000. This type of loan has a set term and schedule of payments. Business term loans are available with fixed or variable rates. They can be secured or unsecured, depending on the borrower’s circumstances. • With banks and traditional lenders, one of the major drawbacks with business term loans is that most small businesses don’t qualify for them and get rejected. Other negatives include fees, such as establishment fees and monthly maintenance fees, and penalties for early repayment.

Business Line of Credit • Unlike with a traditional bank loan, you don’t get a lump-sum payment with a business line of credit. • A predetermined limit is set for the line of credit and you only pay interest on what you draw. • So if you line of credit is $50,000 and you have only used $20,000, you only pay interest on $20,000.

Business Equity Loan • A business equity loan is a loan or line of credit secured against residential or commercial property. • The advantage of a business equity loan is that you can borrow up to 100% of the value of a residential property and get a competitive interest rate. • One big disadvantage of this business loan option is that your property is at risk if you’re not able to repay the loan.

Low-doc or No-doc Business Loan • If you are unable to provide financial statements and proof of income for the previous two years, a low-doc loan might be a solution to your business finance needs. • If you are unable to provide any proof of income, a low-doc loan could be a business loan option. These type of business loans are backed by residential property. • The main shortcoming with these types of loans is the higher interest rates due to the increased risk to the lender.

Unsecured Business Loan • With an unsecured business loan, you can get fast access to cash when you need it. Typically, non-bank lenders (such as Moula) use leading-edge technology to safely and securely check your banking transactions to determine your ability to service a fixed-term unsecured business loan. • In addition, they will check your credit score. Based on these factors, a decision to provide a loan can usually be made within 24 hours. Since the loan is unsecured, the interest rate will be higher than for other business loan options. • Unsecured business loans from non-bank lenders have been growing at fast rate due to the banks’ inability to serve SMEs as a result of regulatory controls.

Consider All the Factors When Choosing a Business Loan Option • Regardless of which type of loan you choose, look at all the factors. These include: • Interest rates – understand the interest rate you are paying and consider the advantages and disadvantages of fixed and variable interest rates. • Payments – consider whether you will you be able to make the repayments as agreed. • Fees – read the fine print about any fees that may apply. • Flexibility – does the loan offer any flexibility such as topping up if you have made all your payments on time and need more funds before the loan has been paid off? • Risk – consider the risks if business conditions change and you are not able to make repayments as required.

Check These Out! • Moula was founded to help hard-working business owners in Australia access the funding they need to grow. In the past, getting funding meant going through weeks of paperwork, hassle, and hurdles. We use data to assess your loan application, which means we can keep things painless and lightning-speedy. • With Moula, you can apply online with no paperwork and no hassle, and have the funds in your account the next day. • For more info on business loan calculator Check out: https://moula.com.au