Download

1 / 23

230 likes | 234 Views

Rates of Return(Review and More). Rates of Return. Single period, and with dividends. Multiple periods, averaging, APR and EAR. Adjusting returns for Taxes. Adjusting returns for Inflation. IRA Accounts and Retirement Scenarios. Expected and Risk-adjusted returns (simple CAPM).

E N D

Rates of Return Single period, and with dividends. Multiple periods, averaging, APR and EAR. • Adjusting returns for Taxes Adjusting returns for Inflation IRA Accounts and Retirement Scenarios Expected and Risk-adjusted returns (simple CAPM).

Single Period (Year) 0 1 100 120 HPR = (120-100) / 100 = 20% (Tie to PV/FV)

With Div. 0 1 Holding Period Return = ----------------------------------------------- = ------------------------ = 25 % = 20% (cap gain) + 5% (div yield) Cash flow of dividends for stocks, and coupons for bonds. 100 120 Div 5 (End Price – Beg. Price + Cash Flow) (120 - 100 + 5) Beg.Price 100

Annualizing Rates of Return (APR and EAR). Say you borrow $9900 promising to repay $10,000 in one month. The $100 interest for the month can be converted into a one-month holding period return HPR of 1.01%. How do you convert it into an annual rate of return? For the APR you simply multiply by 12. For the EAR you compound it over 12 months. (interest is paid on interest unless you repay) HPR = (10000-9900)/9900 = 1.01% APR = 1.01 * 12(months) = 12.12% EAR = (1.01) 12 – 1 = 12.82%

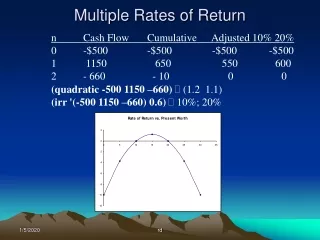

Multiple Periods (Years) 0 1 2 100 * 1+ X)2 = 121 X = 10% per year 0 1 2 100 108 121 8% 12.04% Total Return = 21% for 2-periods (years)

To Average 8% and 12.04% Returns Above? (P 111) • Arithmetic Average = (8 + 12.04)/2 = 10% • Geometric Average = [(1.08) (1.1204)] (1/2) – 1] = 10% When averaging returns over time, use Geometric. • Arith. Avg = 25% • GeomAvg = 0% (which is correct). PV/FV calculations implicitly use the geometric average. 0 1 2 100 50 100 +100% -50%

Dollar Weighted-returns When different amounts are being managed/invested, for different periods of time, then this is just the INTERNAL RATE OF RETURN (IRR).

Pre-tax & After-tax Returns NOTE: Assumption implicit in this calculation is that taxes are paid as you go, i.e, that gains are realized and taxed each year. With mutual funds, the amount to be taxed is determined by the fund at distribution time. For individuals, this may not be appropriate if you are holding stocks long-term. Assume a tax rate of 30%. - tax = -3 After-tax = 107*(1.10) = 117.70 - tax = 3.21 After-tax = 114.49 Together 100 * (1.07 ) = 107 * (1.07) = 114.49 or 10 % pre-tax 10 * (1-tax rate) 7% after tax 10% 1 10% 2 100 * (1.10) = 110 121

Fully Equivalent Taxable Yield (FETY) A CA bond has a yield of 6%, exempt from both federal taxes (@30%) and state taxes @10%. To compare this with a corporate bond on which both federal and state taxes apply, calculate FETY as: 6% 10% ___________ = (1 - 0.4)

Nominal and Real Rates of Return Cost of “basket” =100 (with 7% inflation) = 107 At time 1, the $109 purchases 109/107 = 1.0187 “baskets.” So in terms of purchasing power, the 9% return translates into 1.87% more “baskets” with 7% inflation. 1 + nominal rate Or, real rate of return = ------------------------ - 1 = (1.09/1.07) – 1 = 0.0187 or 1.87% 1 + inflation rate 0 r = 9%(nominal) 1 100 nominal grows at 9% to 109

Nominal and Real Rates of Return (Cont.) Common approximation: To Investors, the Real, After-tax Rate of Return is the One to Consider. Real Rate Nominal Rate Inflation Rate - =

A Simple Retirement Scenario 30 WORK (r = 10%) 65 RETIRE (r=6%) 85 Q: How much to save each year ? Say S. S * FV(ann) (35yrs, 10%) = 458797 = 40000 * PV(ann) (20yrs, 6%) S = 1693/yr or 1693/50000 = 3.3% of income! Q: TOO LITTLE? SAY, inflation is 3% per year over the next 55 years. What does $40,000 in year 85 buy? [40000 / {(1.03)55 }]= 7870 of things in today’s dollars. Note that $40,000 is nominal and $7870 are REAL (or inflation-adjusted) dollars. INCOME = $50,000/yr CONSUME=$40,000/yr

Life expectancy • Inflation Adjustment Issues • Redo in real terms? • Other Savings • Fidelity/Vanguard Software, moneycentral.com, quicken.com, Torrid-tech.com, esplanner.com, wealthwhen.com

Young people find retirement calculations boring, but consider…. You are part of the investment committee of a large pension fund. Say it is the Employees Provident Fund Organization of India (EPFO). BTW, it is the 21st largest pension fund in the world, with assets over USD 110 billion. Employees contribute a portion of their salaries to this provident fund. Employers match it. The money gets invested in fixed income (essentially they are financing the government’s budget deficit! Recently, they were permitted to invest upto 15% of new inflows in the NIFTY and SENSEX ETFs. Retiring employees are given: a) a defined benefit; and/or b) a defined contribution. How risky or conservative would you be in recommending investments to the committee?

EXPECTED RETURNS = sum of (probabilities & possible returns) Prob.Possible Return (over next year) 0.5 50% 0.3 10% 0.4 -20% Exp. Return = 0.5 * 50% + 0.3 * 10% + 0.2 * -20% = 24% Standard deviation = 28%, link to Normal Distribution

Risks • Business Risk • Financial Risk • Exchange rate/Country risks • Systematic and unsystematic risks

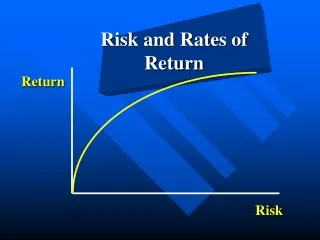

Risk and Expected Return Standard Model (CAPM) E(return) • E(Rj) = Rf + [E(Rm)-Rf] * j = 2 + 6 j • Slope of line = 6 reward per unit risk • Intercept of line = risk free rate = 2% SML (CAPM) Risk (beta)

Where Does This Come From? • For A, the expected return of 14% from current price levels implies an expected future price of 15 * (1.14) = $17.1 • For B, expected return of 12% => expected future price of 50 * 1.12 = $56

Case(i): Suppose B is priced correctly with a risk-reward of 8 • A is priced incorrectly. Investors will buy B, those owning A will sell it and move to B until A’s risk-reward is same as B. • A’s price will fall and its expected return will rise. • What expected return for A is consistent with a risk-reward of 8? • [E(R ) – 4]/1.5 = 8, E(R ) = 16% (increases) • What current price (based on future expected price of 17.1? • Current Price * (1.16) = 17.1, implies Current price for A = 14.74 (decreases from 15). • NOTE: This is a bit contrived to make the point, we have to keep something fixed!

Case (ii): Suppose instead that A is priced correctly • Then B is undervalued and its price will increase to 50.601, its expected return will drop to 10.67% and its risk-reward ratio will be 6.67. Confirm it! • Often, both can happen especially if the market risk-reward is 7 (say). The example illustrates a process of how assets get priced and repriced in markets. The message is that prices will (should) move this way to equate risk/reward ratios across all assets. Or, prices should be set so that the risk/reward ratio for all assets are equal.

Case (ii): Suppose instead that A is priced correctly • Then B is undervalued and its price will increase to 50.601, its expected return will drop to 10.67% and its risk-reward ratio will be 6.67. Confirm it! • Often, both can happen especially if the market risk-reward is 7 (say). The example illustrates a process of how assets get priced and repriced in markets. The message is that prices will (should) move this way to equate risk/reward ratios across all assets. Or, prices should be set so that the risk/reward ratio for all assets are equal. Here the risk-reward ratio has a specific form and using it, • [E(Rj) – Rf]/j = [E(Rm) – Rf]/1.0 = 8, Rearranging: • E(Rj) = Rf + j [E(Rm) – Rf] or the CAPM.

In life, the risk-reward is probably more complicated than that assumed for the CAPM and other models for valuing assets exist.