Download

1 / 29

290 likes | 438 Views

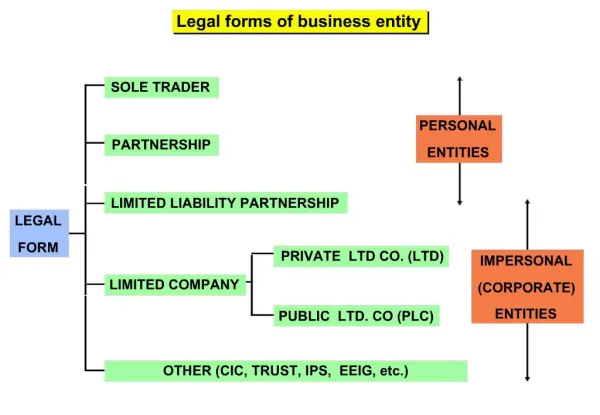

Considerations in Making the Choice of Business Entity. Sole Proprietorship LLP LLC Partnership S Corporation C Corporation. 1. Sole Proprietorship. General Partnership - Registered Limited Liability Partnership. 3. Limited Partnership.

E N D

Considerations in Making the Choice of Business Entity Sole Proprietorship LLP LLC Partnership S Corporation C Corporation

General Partnership- Registered Limited Liability Partnership

DISCUSSION QUESTIONS • 1. When might an S corporation be preferable to an LLC or LP? • 2. When is a single member LLC not a good idea? • 3. When, if ever, is a C corporation appropriate?

DISCUSSION QUESTIONS • 4. When would an LLC be preferable to an LP? • 5. Can you have a 0% General Partner in a Limited Partnership? • 6. What is the level of protection a Registered Limited Liability Partnership provides to its partners?

REGISTERED LIMITED LIABILITY PARTNERSHIP (“RLLP”) A. Requirements. • 1. Name must include the words “registered limited liability partnership” or “limited liability partnership” or the abbreviation “LLP” or “L.L.P.” • 2. Registration with the Secretary of State; $200 per Partner annual filing fee. • 3. Liability Insurance of $100,000 or $100,000 of designated segregated funds

B. Liability Shield Limitations. 1. Liability Protection Not Available if: a. Partner directly supervised or directed the negligent partner or representative; b. Partner directly involved in specific negligent activity committed by other partner or representative; or c. Partner had notice or knowledge of omissions, errors, or negligence and failed to take reasonable steps to cure or prevent such actions.

B. Liability Shield Limitations (cont.) 2. Actions or omissions detailed in 1 above are fact questions. 3. Minimal case law interpreting.

Texas Franchise Tax Planning Conversion of Corporation to Limited Partnership EXISTING PICTURE: Individual Shareholders 100% Corporation (TX) [S Corp]

Texas Franchise Tax Planning Conversion of Corporation to Limited Partnership STEP ONE: Form the Holding Company, a Texas general partnership; make election for the Holding Company to be taxed as a corporation followed by S election (Note: Under IRC Reg. §301.7701-3T(c), an entity that timely files S-election (Form 2553) is deemed have made election to be classified as a corporation (Form 8832)). Individual Shareholders 100% Corporation (TX) [S Corp] Holding Company (TX GP) [taxed as S Corp]

Texas Franchise Tax Planning Conversion of Corporation to Limited Partnership STEP TWO: Transfer 100% of stock ownership in the Corporation to the Holding Company. The Holding Company then makes a Q Sub election for the Corporation. Individual Shareholders Holding Company (TX GP) [taxed as S Corp] Corporation TX [Q Sub]

Texas Franchise Tax Planning Conversion of Corporation to Limited Partnership STEP THREE: The Holding Company forms the General Partner (a corporation or LLC) and transfers a nominal % of the Corporation’s stock to the General Partner as its capital contribution (Consider 0% GP: See Section 4.01 of the TX Limited Partnership Act). Holding Company (TX GP) [taxed as S Corp] 100% General Partner (TX) [Disregarded] 99.75% 0.25% Corporation (TX) [Q Sub]

Texas Franchise Tax Planning Conversion of Corporation to Limited Partnership STEP FOUR: Convert the Corporation into the Partnership (a Texas limited partnership) with General Partner as the sole general partner of the Partnership and the Holding Company as sole limited partner of the Partnership. Holding Company (TX GP) [taxed as S Corp] 100% 99.75% LP General Partner (TX) [Disregarded for FIT] 0.25% GP Partnership (TX) Disregarded for FIT