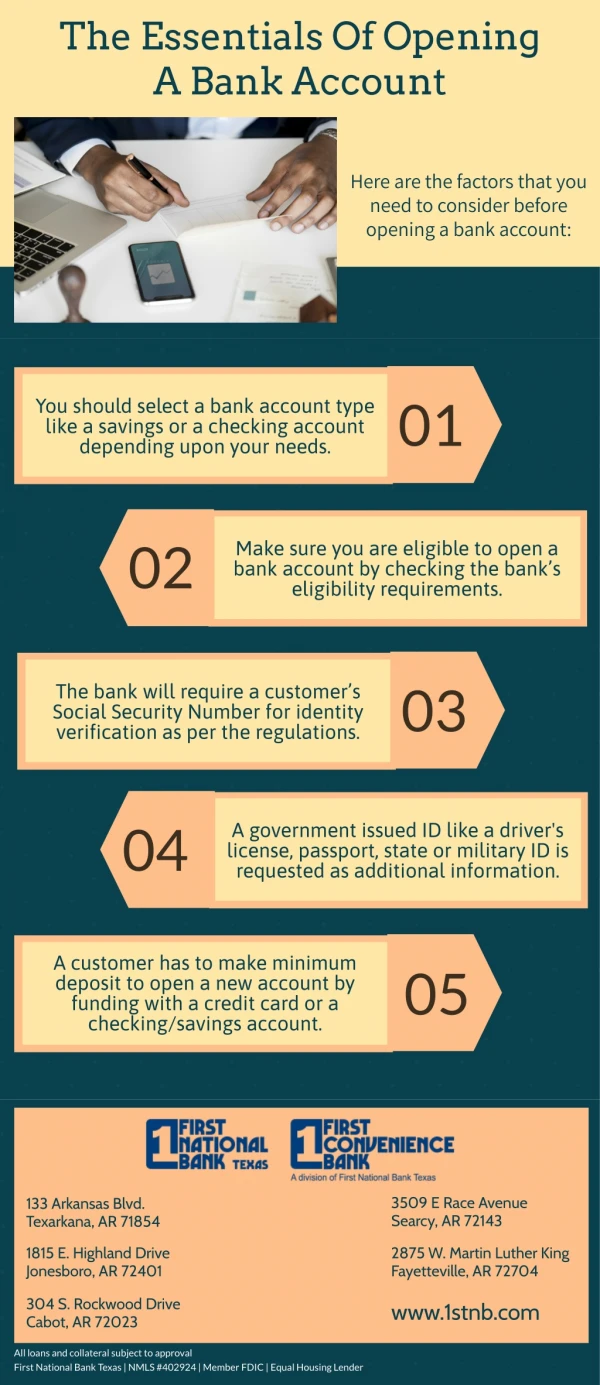

Download

1 / 12

120 likes | 283 Views

D. 17 AUG 05. Improvement of the Retail Account Opening Process. M. TBD. Champion: Chris Berry, GM Personal Banking Team Members : Amro Obaid Mona Al-Ghoraibi Mohiyadeen Ismail Abdulaziz Al-Bani Basher Al-Bahli Shohan Wimalaratne Mohammad Al-Abbad

E N D

D 17 AUG 05 Improvement of the Retail Account Opening Process M TBD Champion: Chris Berry, GM Personal Banking Team Members: Amro Obaid Mona Al-Ghoraibi Mohiyadeen Ismail Abdulaziz Al-Bani Basher Al-Bahli Shohan Wimalaratne Mohammad Al-Abbad Quality Leader:Abdulaziz Al-Ajaji A TBD I TBD C TBD

Project Charter (Version 1.3) Title: Improvement of the Retail Account Opening Process Prepared by: Abdulaziz Al-AjajiChampion: Chris Berry, General Manager Personal Banking Key Stakeholders: Operations / Personal Banking / Branch Network / IT Problem Statement: Business Case: As the opening of an account is typically the first direct contact that the Bank has with a customer, it is also the point at which we create our first impression with the customer – a negative experience could adversely affect the customer’s appetite to do further business with us, determining whether or not they will respond to future cross selling efforts for our range of financial solutions. Therefore it is critical to ensure that the process is efficient and meets their expectations. This initiative complements the Bank’s strategy to make SABB the customer’s 1st choice for the provision of complete financial solutions, and to differentiate ourselves from the competition by the quality of service that we provide. By achieving the target cycle time SABB will improve efficiency and achieve cost saving of XX SAR. Cycle time for account opening (starts at the point of keying customer information into HFE and ends at the point of delivering the ATM card, ATM PIN, and SABB Direct PIN to the customer) ranges between 2-22 days. This has a negative impact on customer service as it creates a poor first impression and a potential loss of sales opportunities. Goal Statement: • Design and pilot a new process that facilitate opening accounts and delivering the related material within 30 minutes by 31 DEC 2005 Project Milestones: Project Scope and Background: Have you checked elsewhere?: HBMY What did you find? Developed a package that includes a generic ATM card, PIN number, and chequebook. Items in this package can be used immediately after opening the account. As a result of such practice, they have a much shorter cycle time than SABB. Scope: This project will cover the end-to-end account opening process, which starts at the point of keying customer information into HFE and ends at the point of delivering a functional account, ATM card, ATM PIN, and SABB Direct PIN). In-Bounds: - Retail accounts pertaining to HNW, affluent, middle, and mass segments Out-of-Bound: - Payroll accounts - Chequebooks - ATM Card/PIN replacement processes Team Selected: Metrics: Primary Metric: Cycle time to open an account and deliver ATM card, ATM PIN, and SABB Direct PIN Secondary Metric: Number of error logs recorded 2

Define - Develop team charter, identify key stakeholders and requirements. Define critical processes. D M A I C Problem Statement: Cycle time for account opening (starts at the point of keying customer information into HFE and ends at the point of delivering the ATM card, ATM PIN, and SABB Direct PIN to the customer) ranges between 2-22 days. This has a negative impact on customer service as it creates a poor first impression and a potential loss of sales opportunities. Business Case: As the opening of an account is typically the first direct contact that the Bank has with a customer, it is also the point at which we create our first impression with the customer – a negative experience could adversely affect the customer’s appetite to do further business with us, determining whether or not they will respond to future cross selling efforts for our range of financial solutions. Therefore it is critical to ensure that the process is efficient and meets their expectations. This initiative complements the Bank’s strategy to make SABB the customer’s 1st choice for the provision of complete financial solutions, and to differentiate ourselves from the competition by the quality of service that we provide. By achieving the target cycle time SABB will improve efficiency and achieve cost saving of XX SAR. Measure, Analyze, and Improve Milestones: • VOC Plan: • Created a sample of target customers who opened an account within 3 months • Performed a survey to obtain preliminary customer requirements in the following segments (Premier, Imtiaz, and Rwaad) • Will translate customer needs into CTQs • Will set specifications for CTQs Ideally wanted to have a more detailed VOC; however, we are confident that customers’ main requirements are captured (see appendix A for further details). More details will be obtained upon the completion of the MR&A report • Goal Statement: • Design and pilot a new process that facilitate opening accounts and delivering the related material within 30 minutes by 31 DEC 2005 Scope: This project will cover the end-to-end account opening process, which starts at the point of keying customer information into HFE and ends at the point of delivering a functional account, ATM card, ATM PIN, and SABB Direct PIN). In-Bounds: - Retail accounts pertaining to HNW, affluent, middle, and mass segments Out-of-Bound: - Payroll accounts - Chequebooks - ATM Card/PIN replacement processes Metrics: Primary: Cycle time to open an account and deliver ATM card, ATM PIN, and SABB Direct PIN Secondary: Number of error logs recorded • Team Needs: • Approval to proceed to the Measure phase Defect Definition: Applications that exceed the 30 minutes target

Improvement of the Retail Account Opening Process VOC Plan WHO WHAT & WHY • Customer and Segments • HNW • Affluent • Middle • Mass • Indicate specifically what do you want to know about your customers • Customer satisfaction level with current cycle time • How long would you like the cycle time to be? • Dissatisfiers in the existing Account Opening Process • How are we doing compared to our competitors? • What are the essential items you would like to receive immediately when opening and account (I.e. ATM card and PIN, phone banking PIN, and chequebook)? • How important it is to have those items personalized as opposed to generic? • Would you prefer the above items mailed or have it immediately? SOURCES • Reactive Sources • Personal Banking existing research and database • Complaints • Proactive Sources • Surveys • Market Research and Analysis • Interviews SUMMARY • Obtain the above customer needs for each of the defined segments (except LVRA) • Translate customer needs into CTQs • Set specifications for CTQs

Voice of the Customer: • Voice of the Customer (VOC) was collected from the following sources: • Sources: • Customer Survey: 60 customers were surveyed, representing the Premier, Imtiaz, Rwaad segments • Market Research and Analyses: Will be carried by an external research agency (ACNielsen). Results of same will be presented in the Measure phase. • Main Findings: • 62% of surveyed expressed low interest in obtaining chequebooks • 62% of surveyed will feel delighted if they received their ATM card and PIN within 30 minutes (20% feel 1-5days ideal) • 30% of surveyed will feel delighted if they received Direct Banking PIN within 30 minutes (58% feel 1-5daysideal) • 20% of surveyed will feel delighted if they received their chequebooks within 30 minutes (58% feel 1-5daysideal)

Measure – Define critical process metrics and establish baseline process capability D M A E C • Revised Problem Statement: • Cycle time for account opening (starts at the point of keying customer information into HFE and ends at the point of delivering the ATM card, ATM PIN, and SABB Direct PIN to the customer) ranges between 2-22 days. This has a negative impact on customer service as it creates a poor first impression and a potential loss of sales opportunities. USL • Process Performance: • Median Cycle Time = 7 days • Maximum number of days = 22 • Data Collection: • Benchmarked against peer and non-peer groups (appendix A) • Mapped existing process • Timed activities, delays, and reworks • Identified causes of errors and reworks • Quick Hits: • Maintenance for ATM card and PIN to be performed at the branch (this will reduce 1 day in delivery time) • CPU and HSV to adopt an assembly-line method • HSV staff to assist CPU in account processing from 8a.m. to 11a.m. and resume signature capturing from 11a.m. to 4:30p.m. • The above two points will ensure that signatures are captured in the same day the documents come to CPU. In addition it will eliminate a delay time of 3H 55M for each application • Stop branches from using quick method (will reduce 08M 20S in CPU processing per application) • Eliminate the requirement of MBO to authorize/stamp/initial applications and documents (this will reduce rework by approximately 35%) • Note: The above quick hits will be evaluated/assessed based on feasibility and ease of implementation. Any initiative that requires a great deal of efforts will only be considered at the design stage. • Key Insights/Way Forward: • Process capability ranges between 2 – 22 days. However, the upper specification limit, which represents customers’ requirements is at 30 minutes • No matter how much we reduce variation, the current process will not meet the specification limits (CTQs) as they are below the process capability limits • Based on the above findings, we will design a new process instead of improving the existing one. This will entail a change in our approach as we will not move to the analyze phase; instead, our next phases will be Design/Engineer and Control (appendix B) • Risks of following such approach are: Time, as the additional complexity of the design requirements might impact/delay the delivery of some milestones. Cost, in terms of new technical requirement, system amendments, …etc. • Appendices: • Appendix A: Benchmarking against peer and non-peer groups • Appendix B: When do we do Design • Appendix C: Detailed process map • Appendix D:Analysis of Rework Causes • Team Needs: • Approval to move to the design phase • Approval to implement quick hits • Approval to reassess project milestones according to the above developments

Appendix A * Only Rawda, Takassusi, Olaya and Nakheel branches provide instant ATM cards. Other branches take 2-3 days to deliver ATM cards to customers

Appendix B When Do We Design? New Process Process Entitlement Define Measure Analyse Engineer Control Yes Yes Design

Appendix D • Analysis of Rework Sources: • The top three causes explain 57.36% of the overall problems with the account opening application; while the top five causes explain 73.76%. • Top five causes are as follows: • Missing authorization signature/stamp/initial • Missing customer information (incomplete application) • Missing documents (ID copy, PoA,…etc.) • Dissimilar customer signature on documents • Missing customer signature • Actions: • The above causes will be considered when designing a new process in the design phase Process Analysis

Engineer – Proposed set of solutions for implementation D M A E C • Solution List: • ATM cards to be produced at the branch and customers will choose PINs via PIN pads • Pre-open accounts and provide branches with all items. (Extend the existing starter process to include all PFS account opening) • Pre-emboss ATM cards and provide instant packages, that contain all account items, to the branches. ATM cards will only be activated when the account is opened and the pack is handed to the customer • Create customer record through direct channels (SABB net or Phone), Produce cards/PINs and provide same to customer at the point of opening the account • Overview of the Selected Solution • Will introduce a system functionality that will enable NSC to assign a max and min thresholds of ATM cards for each branch (to be done once) • Once a branch reaches its min threshold, the system (during the batch run) will automatically produce the required ATM cards to bring it back to the max threshold • ATM cards, ATM PINs, and SABB Direct PINs will be packaged centrally and sent to branches • Branches will keep the assigned number of packages and will be ready to serve the customer within the target time frame • For more information see proposed process maps (Appendix B,C, and D) • Summary of key benefits • Easy/Quick to implement (compared to the solution #1) • The activity/maintenance for ordering the ATM cards is automated as opposed to the manual efforts required for the existing “Starter Accounts” • Accounts are not pre-opened, which reduces the risks/required control measured associated with packaging and handling the account items • Meets project’s goal by facilitating a turn-around time of 30 minutes • Will accommodate the introduction of Chip cards (SPAN2). • More cost effective than the other alternatives (See appendix A for more quantitative analysis) • Way Forward: • Solution will be communicated across the bank as per the attached communication plan (see appendix F) • Control will commence on 3APR06, once new process is functional. COE will develop the monitoring mechanism/control plan and present the Control tollgate in due course Hard Saves • Attachments: • Appendix A: Projected Hard and Soft Saves • Appendix B: Proposed Process Map (Packaging) • Appendix C: Proposed Process Map (Branch) • Appendix D: Proposed Process Map (NSC) • Appendix E: Detailed Implementation Plan • Appendix F: Solution Communication Plan