Download

1 / 75

780 likes | 1.2k Views

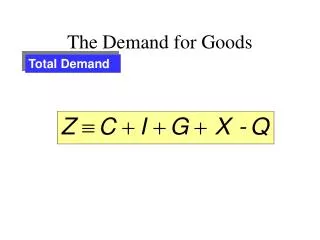

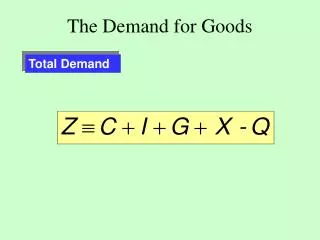

The Demand for Goods. Chapter-5. In This Chapter…. 5.1. Why is demand curve downward slopping? 5.2. How to measure behavioral responses of consumers to changes in determinants of demand (Elasticity)? 5.3. The Effect of Elasticity on the Revenue of the Producer (Seller).

E N D

The Demand for Goods Chapter-5

In This Chapter…. 5.1. Why is demand curve downward slopping? 5.2. How to measure behavioral responses of consumers to changes in determinants of demand (Elasticity)? 5.3. The Effect of Elasticity on the Revenue of the Producer (Seller). 5.3. How Consumers Allocate their Income Among Competing Ends?

5.1. What Explains the Consumer Behavior? • What determines what we buy? How we buy? • What leads us to buy some goods while rejecting others? • Why do we buy more at lower prices and less at higher prices?

5.1.What Explains the Consumer Behavior? • Two Explanations • The Sociopsychiatric Explanation • The Economic Explanation

5.1.What Explains the Consumer Behavior? • The Sociopsychiatric Explanation • In Freud’s view, higher levels of consumption satisfy our basic drives for security, sex, and ego gratification. • According to sociologists, consuming more is an expression of identity that provokes recognition or social acceptance.

5.1. What Explains the Consumer Behavior? • The Economic Explanation • In explaining consumer behavior, economists focus on the demand for goods and services. • Demand is the willingness and ability to buy specific quantities of a good at alternative prices in a given time period, ceteris paribus.

The Economic Explanation • An individual’s demand for a product is determined by: • Tastes—desire for this and other goods. • Income—of the consumer. • Expectations—for income, prices, tastes. • Other goods—their availability and prices.

The Economic Explanation • Economists use the Demand Curve to Explain the consumer behavior… how consumer tastes affect consumption decisions. • Law of demand: Ceteris paribus, individuals buy less quantities, when prices are higher and more quantities when prices are lower. • They do so because they have a goal of getting maximum Possible Satisfaction (Pleasure) from their limited resources. • Utility

The Economic Explanation • Utility is the pleasure or satisfaction obtained from a good or service. Utility Theory • Measuring Utility (Satisfaction) • Cardinal Units (absolute numbers indicating levels): Utils • Ordinal Unity (Rankings, Orders of preferences)

The Economic Explanation • Total Utility is the amount of satisfaction obtained from entire consumption of a product. • The more we consume of a product the more utility (satisfaction) we obtain. I.e., More is Preferred to Less! • Thus the more pleasure (utility) a product gives us, the higher the price we’re willing to pay for it.

The Economic Explanation • However, more is not always and necessarily better. Two Distinct Levels of Satisfaction: • Total Utility • Marginal (additional) Utility

The Economic Explanation • Total Utility : • the amount of satisfaction obtained from the entire consumption of a product. • Marginal utility: • the change in total utility obtained by consuming one additional (marginal) unit of a good or service.

TOTAL UTILITY Total utility Total Utility Rising total utility 0 1 2 3 4 5 6 Quantity of Popcorn (boxes per show) The Economic Explanation • There is a natural limit to how much more...

The Economic Explanation • Although we prefer more to less, more is not always and necessary better … • Human Behavior: • When we have more and more of some thing we start to value it less and less. We do so… • The additional satisfaction we get from consuming one more unit of the same product is lower than the level of satisfaction we obtain from consuming earlier units of the product. • Declining Marginal Utility

TOTAL UTILITY MARGINAL UTILITY Negative marginal utility Total utility Total Utility Marginal Utility Rising total utility Diminishing marginal utility 0 1 2 3 4 5 6 0 1 2 3 4 5 6 Quantity of Popcorn (boxes per show) Quantity of Popcorn (boxes per show) The Economic Explanation

Diminishing Marginal Utility • According to the law of diminishing marginal utility, the marginal utility of a good declines as more of it is consumed in a given time period. • As long as marginal utility is positive, total utility must be increasing.

Diminishing Marginal Utility • According to the law of diminishing utility, each successive unit of a good consumed yields less additional utility. • Eventually, additional quantities of a good yield increasingly smaller increments of satisfaction. • Downward slopping Demand Curve

The Economic Explanation Implication… • Our consumption decision is guided by not by how much total satisfaction we get, but by how much additional satisfaction we get when consuming one more unit of a product

The Economic Explanation Demand Curve: Price and Quantity relationship (Why is it downward slopping?) • Tastes, through marginal utility, tells us how much we desire particular goods. • Price tell us how much of a good we will buy. • The more marginal utility a product delivers, the more a consumer is willing to pay, ceteris paribus. • As the marginal utility of a good diminishes, so does our willingness to pay.

5.2. Gagging Responses to Changes in the Determinants of Demand

5.2. Gagging Responses to Changes in the Determinants of Demand • According to thelaw of demand, the quantity of a good demanded in a given time period increases as its price falls, ceteris paribus. • (Own Price, Income, Price of other Products,….)

5.2. Gagging Responses to Changes in the Determinants of Demand • Elasticity • A measure of the responsiveness (the sensitivity) of consumers (buyers) –in terms of the quantities they buy, to changes in the determinants of demand (Own Price, Income of the Consumer, Price of Other Goods, etc)

5.2. Gagging Responses to Changes in the Determinants of Demand • Elasticity • Price Elasticity of Demand • Income Elasticity of Demand • Cross Price Elasticity of Demand

Price Elasticity (E) • Theprice elasticity of demand is the percentage change in quantity demanded divided by the percentage change in price. • Is a measure of the response of consumers to a changes in own price of a product.

$0.55 A 0.50 B 0.45 C 0.40 D 0.35 E 0.30 PRICE (per ounce) F 0.25 G 0.20 H 0.15 I 0.10 J 0.05 0 4 8 12 16 20 24 28 32 Quantity Demanded (Ounces per show) Individual’s Demand Schedule and Curve The willingness to pay diminishes along with marginal utility

Computing Price Elasticity • To ensure consistency,… • average quantity and average price (before and after) is used in the calculation of Elasticity.

Note on the Sign of Price Elasticity (E) of Demand • The price elasticity of demand (E) is always negative because quantity demanded decreases when prices increase. • However, as we often use its absolute value, the price elasticity of demand is reported as a positive number (greater than zero).

$0.55 A 0.50 B 0.45 C 0.40 D 0.35 E 0.30 PRICE (per ounce) F 0.25 G 0.20 H 0.15 I 0.10 J 0.05 0 4 8 12 16 20 24 28 32 Quantity Demanded (Ounces per show) In Class Hands-on-Problem • Compute Elasticity for • A movement from • C to D • G to H • J to I

Possible Values of Elasticity: |E| • E can take any value between from 0 to infinity • Five Broad categories • 0<E<1; E=1; 1<E<Positive Infinity • Two extreme Values (E=0 ; E=Positive Infinity)

Elastic, Inelastic, Unitary Elastic Demand • If E is larger than 1, demand is elastic. • Consumer response is large relative to the change in price. • Relatively Flat Demand Curve • If E equals 1, demand is unitary elastic. • If E is less than 1, demand is inelastic. • Consumers aren’t very responsive to price changes. • Relatively Steeper Demand Curve

Extremes of Elasticity • Two extreme Values (E=0; E=Positive Infinity) • E=0: Perfectly inelastic. • Quantity demanded will not change regardless of the price change. • A Vertical demand curve • E=Infinity: Perfectly elastic • Any price increase would cause demand to fall to zero. • A Horizontal demand curve.

Perfectly elastic (E = ) Perfectly inelastic (E = 0) p2 p2 Price Price p1 p1 q1 q1 0 0 Quantity Quantity Extremes of Elasticity

Determinants of Elasticity • The price elasticity of demand is influenced by all of the determinants of demand. • Four factors are particularly worth noting: • Necessities vs. Luxuries. • Availability of Substitutes. • Relative Price (to income). • Time.

Necessities vs. Luxuries • Necessities are goods that are critical to our day-to-day life. • Demand for necessities is relatively inelastic • Luxuries are goods we would like to have but are not likely to buy unless our income jumps or the price declines sharply. • Demand for luxury goods is relatively elastic.

Availability of Substitutes • If a good has relatively many substitutes, consumers are highly sensitive to changes in the price of the good. • Thus the greater the availability of substitutes, the higher is the price elasticity of demand…relatively elastic

Relative Price (to income) • Consumers are more sensitive to changes in prices of goods that account for a relatively larger share of their budget (at higher price level) than those that account for relatively smaller share of their budget (lower price) • The higher the price of a good relative to a consumer’s income, the higher the elasticity of demand. • The price elasticity of demand declines as price moves down the demand curve.

Time • Consumers are better able to change their buying habits over the long-run (thus more sensitive to changes in prices) than in the short-run (Less sensitive). • Thus in the long-run price elasticity of demand is higher than the short-run elasticity.

Elasticities and the Other Determinants of Demand • Price Elasticity of Demand • Income Elasticity of Demand • Cross Price Elasticity of Demand

Shifts vs. Movements • Recall: • When the price changes, the outcome is a movement along the same demand curve. • When any one of the underlying determinants of demand (other than own price of the good) changes, the entire demand curve shifts. • Income and prices of other goods are among such factors

Income Elasticity • An increase (decrease) in consumer income will cause a rightward (leftward) shift in demand. • I.e., consumers will purchase more at any price than they did prior to the increase in income.

Shift Income Elasticity F N 0.25 Price of Popcorn (dollars per ounce) D2 (after income rise) D1(before income rise) 0 12 16 Quantity of Popcorn (ounces per show)

Income Elasticity • Income elasticity of demand is the measure of the percentage change in quantity demanded by the consumer resulting from a percent change in income of the consumer.

Computing Income Elasticity • As with price elasticity, income elasticity is computed using average values for the changes in quantity and income.

Normal vs. Inferior Goods • A normal good has an income elasticity of demand greater than zero. • Anormal good is a good for which demand rises when income rises. • An inferior good has an income elasticity of demand less than zero. • An inferior good is a good for which demand decreases when income rises.

Cross-Price Elasticity • A change in the price of one good affects the demand for another. • The decision to buy a good also depends on the prices of substitutes and complements of that good.

Cross-Price Elasticity • Substitute goods are goods that substitute for each other. • When the price of good X rises, the demand for good Y increases, ceteris paribus. • Complementary goods are goods frequently consumed in combination. • When the price of good X rises, the demand for complementary good Y falls, ceteris paribus.

Price of Popcorn (cents per ounce) R F 0.25 D3 D1 D2 0 8 12 Quantity of Popcorn (ounces per show) Substitutes and Complements