Download

1 / 27

270 likes | 529 Views

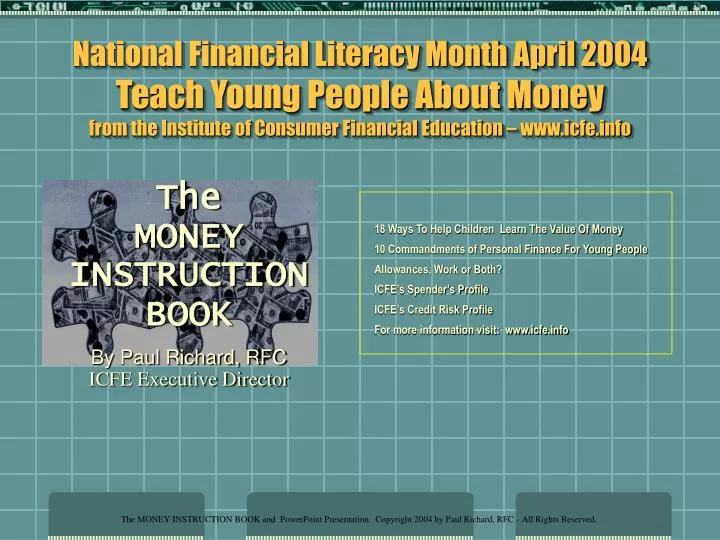

The MONEY INSTRUCTION BOOK By Paul Richard, RFC ICFE Executive Director. National Financial Literacy Month April 2004 Teach Young People About Money from the Institute of Consumer Financial Education – www.icfe.info. 18 Ways To Help Children Learn The Value Of Money

E N D

The MONEY INSTRUCTION BOOK By Paul Richard, RFC ICFE Executive Director National Financial Literacy Month April 2004Teach Young People About Moneyfrom the Institute of Consumer Financial Education – www.icfe.info 18 Ways To Help Children Learn The Value Of Money 10 Commandments of Personal Finance For Young People Allowances, Work or Both? ICFE’s Spender’s Profile ICFE’s Credit Risk Profile For more information visit: www.icfe.info

As soon as children can count, introduce them to money. Communicate with children, as they grow, about your values concerning money and how to save it Helping children also learn the difference between needs, wants and wishes. Setting goals is a fundamental concept to help young people learn the value of money and also how to save. Indoctrinate your children to accumulation (or savings). When giving children an allowance or income, give money in denominations that encourage savings. 18 Ways To Help Children Learn The Value of Money

18 Ways To Help Children Learn The Value of Money • Introduce U. S. Savings Bonds to children. Take them to the bank when you make the purchase. • Take the youngsters with you to a credit union (or a bank) when you open their savings accounts. • Keeping good records of money saved, invested or spent is another primary skill young people must learn. • Going to the grocery store is usually one of a child’s first spending experiences. • Take children with you to other stores, explaining how to plan purchases in advance and make unit price comparisons and also checking for value, quality, reparability, warranty, etc. • Allow young people to make spending decisions, both good and poor, and then encourage a discussion of pros and cons before more spending takes place.

13. Show children how to evaluate ads on TV, radio and in print. Will the product really perform and do what the commercials say? 14. Look into joining a credit union, if you are not a member already. 15. Alert children to the dangers of borrowing and paying interest. 16. If parents are using credit cards, at a restaurant for example, take advantage of an opportunity and explain to children how to verify the charges, how to calculate the tip. 17. Be cautious about making credit cards available to young people even when they are entering college. 18. Using a calendar, establish a regular schedule for a family discussion about finances. 18 Ways To Help Children Learn The Value of Money

18 Ways To Help Children Learn The Value of Money • SUMMARY: Money gives people - both young and older - decision-making opportunities. Everyday spending decisions can have a far greater negative impact on your children’s financial future (and yours also) than any investment decisions they (or you) may ever make. Educating, motivating and empowering your children to become regular savers and investors will enable them to keep more of the money they earn and do more with the money they keep!

10 Commandments of Personal Finance for Young People 1) Manage your expenses so they don’t exceed your income. 2) Spend money thinking about your future as well as your present. 3) Begin saving early to take advantage of compound interest, because it’s not retroactive. 4) Avoid collecting credit cards for borrowing.

10 Commandments… 5) Always honor your debts and other financial obligations. 6) Project income and expenses for 12 months and track any variances from month to month. 7) Focus on the relationship between the risk and the projected return of investments. It’s one thing to get a return on your investment, it’s another to get all of your initial investment back.

10 Commandments… 8) Maintain and organize records for tax and also general financial planning purposes. 9) Have a plan and a purpose for your investing. 10) Obtain a financial education to be in a position make intelligent financial decisions.

Allowances . . or Work . . or Both? • The question of allowances is often raised by parents and children alike. While it is a personal decision, the concept of giving an allowance and having work income seems to work best. Parental goals, when paying an allowance, should be to:1)Shift some spending decisions from parents to the child.2)Eliminate or dramatically reduce the need for the child to have to ask for money.3)Provide a method, under proper supervision, for learning about accumulating money and also wise spending techniques.

Allowances . . or Work . . or Both? • Birth to age 8 1) Assign basic household chores (make the bed) 2) Don’t buy toys on demand 3) Allow them to learn about actions and con -sequences (having possessions also brings responsibilities).

Allowances . . or Work . . or Both? • Ages 9 to 13 1) Allow child to begin making spending decisions on their own. Encourage comparison shopping. 2) Give a specific allowance and stick to it. 3) Don’t pay youngsters for doing basic chores, because if you do, the day may come when a child will refuse to clean their room because they don’t need money.

Allowances . . or Work . . or Both? • Ages 13 and older 1) Be consistent - continue to have daily household chores – no child should be too busy to pick up after him or herself. 2) Help your child forget her or himself. A great family activity is donating time and or money to a worthy cause.

Are you a good spender?Try the ICFE’s Spender’s Profile • Practically everyone loves to spend their money, but how good of a spender are you these days? • Are you getting the most value for your dollar? • The ICFE Spender’s Profile consists of 20 statements about your spending life-style. Instructions follow on the next slide • A scoring module is at the end of this section.

Using a sheet of paper… • Answer the following 20 statements with one of the following five responses.: • 1) totally like me • 2) A lot like me • 3) Equally like and unlike me • 4) A little like me • 5) Not like me at all

ICFE’s Spender’s Profile • 1) Each time I get any money, I put a small amount of cash aside as savings. • 2) Each time I receive any money I usually Deposit it into a savings or checking account. • 3) I keep track of the money I receive from all sources. • 4) I set aside a predetermined amount of my cash for regular weekly expenses.

ICFE’s Spender’s Profile • 5) I set aside at least ten percent of the money I receive for savings. • 6) My money is managed according to a written spending-plan. • 7) My food, grocery and household spending is planned in advance and done with a list. • 8) I rarely make less than two trips-a-week to a grocery or convenience store.

ICFE’s Spender’s Profile • 9) Grocery, household coupons and manufacturer rebates are used whenever possible. • 10) Comparison shopping for price, value, quality is something I do for practically every purchase. • 11) I do not have credit cards with a balance due. • 12) I do not have any loans with a balance owed. • 13) I have comparison shopped for both food and clothing in the last year.

ICFE’s Spender’s Profile • 14) I do not dine/eat out more than once a-week. • 15) I have received my earnings statement from the Social Security Administration. • 16) I account for all my cash spending by collecting receipts and noting what is bought. • 17) I balance my checking/share draft accounts with each statement received.

ICFE’s Spender’s Profile • 18) I have looked into joining or I am a member of a credit union. • 19) I am saving money towards a college education. • 20) I have given money or food to less fortunate individual within the last month. • Total up your points for all 20 questions

ICFE’s Spender’s Profile Scoring • 17-27 points - Terrific! - Teach others. • 28-42 points - Pretty good - Stay Up-to-date • 43-58 points - Average - A class will be helpful • 59-74 points - Lousy – Make needed changes • 75+ points - It Stinks! – Make an immediate appointment with a bona fide, nonprofit Consumer Credit Counseling organization.

ICFE’s Credit Risk Profile • Are you seeking credit for the first time? Or are you seeking more credit, like more credit cards? • If so, Will you be a good credit risk? • The credit risk profile, with true or false questions, may help you understand how well you might manage credit-based spending and also provide insight as to why you want credit.

ICFE’s Credit Risk ProfileUsing a sheet of paper ….. • Answer the following 15 questions true or false • 1) Having a credit card will give me (give me) a sense of security. • 2) I purchase more (expect to purchase more) from retailers who will extend me credit. • 3) I often pay for eating out or purchase gifts to impress others. • 4) Credit cards (will) help me improve my life-style.

ICFE’s Credit Risk Profile…… • 5) Having credit allows me to buy the things I want now. • 6) I often argue with myself or family members or others about over-spending. • 7) My savings account balance is negatively affected by credit-based spending. • 8) I often have trouble recounting the money I have spent during the day.

ICFE’s Credit Risk Profile….. • 9) Other people I know overspend, and it doesn’t seem to hurt them financially. • 10) My closet if full of things I have only used once or twice. • 11) Many things I purchase, I wish I hadn’t by the time I get home. • 12) I am often (can be) a few days late with some payments, but it doesn’t matter much

ICFE’s Credit Risk Profile…… • 13) I have borrowed money from friends and relatives that I have not repaid. • 14) I make impulse purchases to make me feel better. • 15) I charge things like meals, gas and groceries that are gone when the bill arrives. Now add up your true(s) and false(s) – scoring next

ICFE’s Credit Risk Profile Scoring • None True: A credit worthy person. • 1 or 2 True: Just barely “OK” • 3 – 5 True: Suspend credit-based spending. • 5 –10 True: You may be a “debt-head” • 11-15 True: A confirmed plastic addict. • Put those credit cards in a glass of water and freeze them solid. More help onwww.icfe.info

The Institute of Consumer Financial Education • This PowerPoint presentation is made available as a public service in recognition of National Financial Literacy Month – April 2004 by the award winning Institute of Consumer Financial Education (ICFE) ICFE - PO Box 34070, San Diego, CA 92163 • www.icfe.info • Other PowerPoint presentations available