Download

1 / 22

220 likes | 326 Views

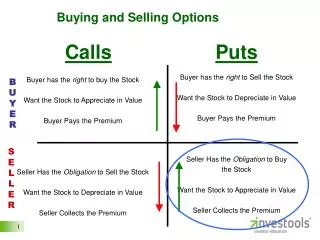

Buying and Selling Securities. Chapter 13. Classifying Today’s Investment Alternatives. Direct investing You actually own the investment Types of direct investments Fixed-income securities Stocks Real estate Exotic investments (options, futures, real assets, collectibles)

E N D

Buying and Selling Securities Chapter 13

Classifying Today’s Investment Alternatives • Direct investing • You actually own the investment • Types of direct investments • Fixed-income securities • Stocks • Real estate • Exotic investments (options, futures, real assets, collectibles) • Indirect investing • You own shares in an investment company (typically a mutual fund) that actually owns the investment

Fixed-Income Securities • You are lending money to the issuer of the security (can be a corporation, the government, etc.) • Characteristics • You would buy the fixed-income security because the issuer promises to pay you a fixed amount of interest income every period • The security will mature at some point and you will receive par, or face value, at that point • If the issuer fails to make interest or principal payments when due, you have certain legal rights as a lender • Known as default risk

Money Market Instruments • Mature within one year of issuance • Typically sold at a discount • Low risk (in terms of default) • Large face values ($100,000 to $1 million) • You’ll probably never buy a money market security directly • T-bills have small face values ($10,000)

Bonds (Long-Term, Fixed-Income Securities) • Up to a 30-year maturity date • Most bonds pay a periodic, fixed amount of interest (income to you) • Most bonds are callable • Gives issuer right to buy back the bonds • Bonds vary widely in terms of default risk • How much default risk a bond has depends on the issuer • U.S. government, municipality, corporation

Bonds (Long-Term, Fixed-Income Securities) • Treasury notes and bonds • Issued by U.S. Treasury • Maturities range from 2 to 30 years • Treasury has not sold bonds since 1999 • Fixed coupon rates • No default risk • Interest is exempt from state (not federal) income taxes

Bonds (Long-Term, Fixed-Income Securities) • Municipal bonds • Issued by state and local government units • Used for public projects such as building a new school, repairing highways • Types of municipal bonds • Revenue – only the revenue generated from the project for which bonds were issued is used to pay income on bond • General obligation bond – backed by the “full faith and credit” of the state • Interest income is exempt from federal income taxes • Many are rated by bond rating companies • Standard & Poors • Moodys

Bonds (Long-Term, Fixed-Income Securities) • Corporate bonds • Issued by corporations to finance expansion, etc. • Vary widely in terms of collateral and repayment provisions • Vary widely in terms of default risk • Interest income is subject to federal and state taxes

What Determines Bond Prices? • Price of bond is present value of future expected cash flows • The higher the discount rate used to find the present value, the lower the present value, and vice versa • It is possible for a bond to sell at a price above or below face value • Depends on the interest rate used to discount the bond’s future cash payments • Known as yield to maturity • A bond’s yield to maturity changes as market interest rates change

Stock Investing • As a stockholder, you actually own a portion of a company • You have voting rights (vote for members of the board of directors who oversee the company’s management) • Why invest in common stock? • As a bondholder, you are promised a fixed income (interest) regardless of how well or poorly the firm performs • As a stockholder, as the firm profits, you profit through either dividends or stock price increase (or both)

Stock Investing • Dividends represent cash payments from a firm to its stockholders • Not guaranteed • Can be eliminated, increased, decreased • Some firms pay dividends, some don’t • As a stockholder, you want to see a firm’s stock price rise, as you would benefit when you sold the stock • Most of a stockholder’s return comes in the form of an increase in stock price

Types of Common Stock • Blue chip stocks: companies with a long record of stable earnings and dividend growth, financially strong • Growth stocks: firms experiencing rapid sales and earnings growth (and this growth is expected to continue) • Income stocks: stocks that produce most of the return to stockholders in the form of dividends, rather than price appreciation (utility companies) • Speculative stocks: risky, as they may do quite well or quite poorly • Cyclical vs. defensive stocks: stocks that move with, or against (or have little relationship with) the market

Valuing Common Stocks • How much should you be willing to pay for this stock? • If you own it already, at what price should you sell it? • Subjective component • Stock A is currently selling for $46 • To some, this is a good purchase price • To others, it is not… • Different people use different valuation techniques • Technicians vs fundamentalists

Valuing Common Stocks • In general, the following factors affect a stock’s price • Company earnings • Company dividends • Expected growth rate in company’s future earnings and dividends • Uncertainty over above growth rate • Interest rates

Choosing the Right Stock for You • Does the stock fit into your overall investment plan in terms of • Goals • Risk tolerance • Don’t forget to diversify

Understanding Financial Markets • U.S. financial markets are fair, open, and orderly • Trades occur in full view of all market participants • Information is available as to the number of buyers and sellers (important because supply and demand determine market prices) • Assuming no new pertinent information, one can place a trade at or near the last trade price • Transaction costs are low (commissions) • All participants have equal access to the market • Prices adjust quickly to new public information

Types of Financial Markets • Primary vs secondary • Where trading takes place • Physical location—trading floor • Via computers (over-the-counter markets) • Examples of financial markets • NYSE • Trading floor • NASDAQ • Computer-based network

Selecting a Brokerage Firm and a Broker • Do you want full service? • Offer investment advice • Record keeping • Access to analysts’ reports • Provide list of recommended securities • Normally deal with a specific person who is your broker (and paid on commission) • Do you want discount service? • Mainly provides order execution & record keeping • Most provide information from independent sources (for a fee) • Broker works via salary, you deal with no specific person • Do you want deep discount service? • Provide order execution and record keeping and little else

Selecting a Brokerage Firm and a Broker • The main difference is in the area of advice and how much you pay • Are you an inexperienced investor AND • Do you think an experienced investment professional can consistently earn you more than if you invested in the stock market in general?

Selecting a Stockbroker • Remember, with a full-service firm, the stockbroker is paid on commission (and receives a higher commission on some items compared to others) • Before you select a broker, set your financial goals, time horizon, and your tolerance for risk • Interview several brokers at several firms • Ask about their experience, educational background, typical client • Check the broker’s background and licenses • Make certain that the broker clearly explains the commission he’ll receive for specific products • Don’t submit to pressure! • Be wary of unsolicited calls (cold calls) • NEVER buy a security from a cold call—ALWAYS ask for written information about the investment and check that investment via other sources

Types of Orders and Trades • Market order • Order to trade at the best possible price for you • Lowest (highest) if you are buying (selling) • Most are filled within seconds of the time you place the order • Limit order • Establishes a floor (as a seller) or ceiling (as a buyer) for stock price

Investment Record Keeping • Extremely important • Taxes • Dividends • Capital gains/losses • Commissions are tax deductible, but you need to have the records for proof • Track your performance • Update records at least quarterly • Will receive monthly statements from broker