Download

1 / 15

310 likes | 900 Views

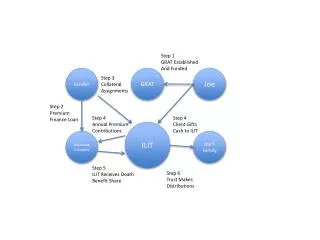

What Is An Irrevocable Life Insurance Trust (ILIT)?. A vehicle for owning life insurance policies in order to: Remove and avoid taxation of policy proceeds in the insured’s gross estate

E N D

What Is An Irrevocable Life Insurance Trust (ILIT)? • A vehicle for owning life insurance policies in order to: • Remove and avoid taxation of policy proceeds in the insured’s gross estate • Provide liquid funds to make loans to estate or pay estate taxes through the purchase of assets from the estate • Removal of proceeds could be achieved by giving policies or cash to purchase policies outright to children and grandchildren • However, there is no guarantee these funds will be made available to the estate for payment of taxes, debts, and other estate related cash needs

What Is An ILIT? (cont’d) • Where annual gifts of premium will be made after the initial gift, in order for those gifts to qualify as a “present interest” for the annual exclusion, the trust will have a Crummey withdrawal power in the beneficiaries • A Crummey power allows beneficiaries a temporary right to withdraw funds from the trust each time a contribution is made to the trust

What Is ILIT? (cont’d) • Once the withdrawal right lapses, the trustee is free to use the monies to pay premiums on the life insurance policy • If a beneficiary makes a demand, the trustee must deliver the funds to the beneficiary, and may cause an inability of the trustee to pay the premiums due to lack of funds

When Is Use Of An ILIT Appropriate? • Whenever an individual or couple faces a death tax at his or her generation • Whenever there is a desire to provide liquidity for the estate, without subjecting life insurance policy proceeds to death taxes • To leverage the value of a gift, since the gift value of life insurance is based on the interpolated terminal reserve, whereas the death benefit of the policy is many times greater

When Is Use Of An ILIT Appropriate? (cont’d) • For gifts to minors or others who lack capacity to manage the policies or proceeds • Where the donor does not have confidence that gift recipients will make proceeds available to the donor’s estate for payment of taxes and expenses

What Are The Requirements? • Donor must create a trust to receive the insurance gift (or to receive cash to purchase a new policy) • Trust needs to provide terms for managing assets both before and after insured’s death, as well as with respect to availability of funds to make loans or purchase assets from the insured’s estate • Donor must transfer the policy by signing an irrevocable assignment to the trustee of the trust or make a cash gift to the trust to allow the trustee to purchase a new policy • Note: Policies transferred to the trust are subject to the 3 year rule, new policies purchased by the trust are not

What Are The Requirements? (cont’d) • Insured or proposed insured must be in reasonably good health to: • Avoid the policy being valued at a much greater value for gift tax purposes • To be able to keep gifts for annual premiums within the annual exclusion or lifetime gift tax exemption, if possible

What Are The Requirements? (cont’d) • Crummey Withdrawal Power • Beneficiary must have notice of demand right • Adequate time must be allowed for exercise of the withdrawal power (usually 30 days) • For annual exclusion, must be a present interest, meaning an unfettered, ascertainable right to use, possess or enjoy the money or property placed in the trust • Gifts of future interest will not qualify for the annual exclusion

What Are The Requirements? (cont’d) • Crummey Withdrawal Power (cont’d) • Beneficiary must be able to actually receive the property upon exercise of the demand right • Where the beneficiary is a minor, the ability of a guardian to make a demand on the minor’s behalf is necessary to qualify as a present interest • The IRS attacks naked Crummey powers where persons given the powers have little or no interest in the trust other than the Crummey powers, merely to increase the number of annual exclusions

How It Is Done – An Example • Harry and Donna Bradley wish to make a gift to each of their two children and four grandchildren that will qualify for the annual exclusion • Their annual exclusion amount in 2011 is $13,000 per individual from both Harry and Donna, or a total of $156,000 (2 donors x 6 donees x $13,000) • The Bradley’s would like to make these gifts to a trust that would continue until their youngest child reaches age 35, and then distribute equally to the children and grandchildren

How It Is Done – An Example (cont’d) • The Bradley’s do not want the trust to make any distributions of current income • An ILIT meets all of the Bradley’s requirements if it includes Crummey powers for all of the children and grandchildren • Note: Separate shares are required if the trust is to be exempt from GST tax using only the GST annual exclusion (otherwise allocation of GST exemption should be made)

Issues In Community Property States • A couple owning community property can give $26,000 (in 2010 and 2011) per recipient without any need for gift splitting because each spouse owns ½ of the community property • It is not appropriate to give a surviving spouse a life interest in the entire policy proceeds, where the surviving spouse has been a grantor as to ½ of the gifts used to pay the insurance premiums

Gift & Estate Tax Implications • Gift value of life insurance policy based on interpolated terminal reserve value, but may be much higher if insured is in poor health or uninsurable • Crummey withdrawal power can make both cash gifts and gifts of policies themselves qualify for the annual exclusion Note: Lapse of withdrawal power to the extent it exceeds the greater of $5,000 or 5% of trust corpus causes a taxable gift by the power holder to the remainder persons of the trust

Gift & Estate Tax Implications (cont’d) Note: Since the beneficiary who allowed the power to lapse also has a continuing right in the trust (life estate), the property subject to the lapsed power will be included in the beneficiary’s estate for estate tax purposes as a transfer with a retained interest Careful estate planning, trust drafting, and record keeping can limit or eliminate the problems associated with the lapses exceeding the 5 or 5 limit Note: The amount subject to the Crummey withdrawal, where the withdrawal period has not lapsed, is included in the beneficiary’s estate for estate tax purposes since the withdrawal power is a general power of appointment

3 Year Rule • Gift of life insurance policy within 3 years of death, generally brought back into gross estate • There’s really no way around the 3 year rule as it relates to gifts of insurance policies to an ILIT • Also, sales of existing policies to an ILIT will trigger the transfer for value rule, causing policy proceeds to be taxed as ordinary income to the extent they exceed the purchase price of the policy, unless an exception applies • If possible, the best route is to give money to trust and have the trust purchase a new policy on the grantor