Download

1 / 2

20 likes | 26 Views

If you’re in the market for a new car, we recommend a few steps to make car shopping go smoother. The most important? Check your credit history. Visit: https://www.outsidefinancial.com/

E N D

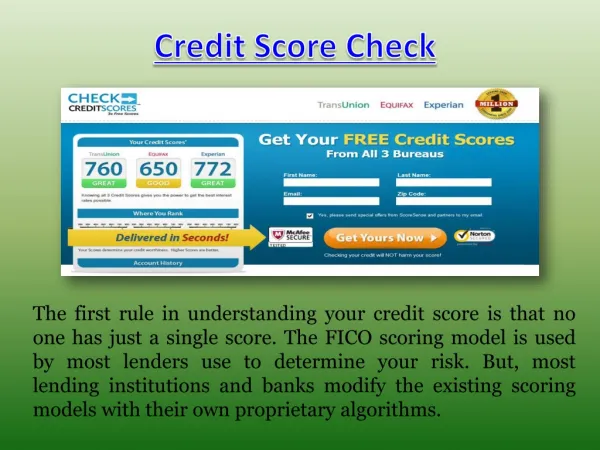

Buying a Car? Try to Improve your Credit Score First If you’re in the market for a new car, we recommend a few steps to make car shopping go smoother. The most important? Check your credit history. What does credit have to do with car shopping? Car loans! Auto loan interest rates depend on the borrower’s credit history and score. The higher your credit score, the lower interest rates you should expect because lenders view lending you money as lower-risk. Your credit score doesn’t just change the interest rate; it can also mean the difference between being approved and declined. Many lenders won’t lend money to anyone with a credit score below a certain number. [Sidebar: You can always check the auto interest rates you pre-qualify for on Outside Financial, without affecting your credit.] How Can You Check Your Credit Score? By law, you can access each of your credit reports for free once a year at annualcreditreport.com. Before you car shop, make sure yours is accurate and up-to-date. One surprising thing not included on your credit report is your credit score. Many credit card providers, banks, and credit unions offer free scores as a perk; ask your financial service provider if they’re one of them. Discover offers free scores, even to non-customers, and sites like Credit Karma and NerdWallet will monitor your score. These scores may not be identical to what lenders use, but they will give some indication of your credit profile. What Happens If You See an Error on Your Credit Report? If you see an error, contact the credit bureau (Equifax, Experian, or TransUnion) and the company that reported the error. The CFPB offers helpful templates if you want to dispute anything on your credit report. How Can You Increase Your Credit Score? You’ve checked your report, and everything checks out. So how do you improve your credit score? First, make sure you pay your bills on time, especially your car loan. Most auto lenders give your car loan history extra weight, so it’s important that your car loan payments are paid on time, in full, each month. Second, improve your credit utilization ratio. Credit utilization measures the amount of credit available to you compared to the amount you’re using. For example, if you have a credit card with a $10,000 limit, and you charged $1,000, your utilization is 10%. Keeping utilization under 30% is a good benchmark. Third, be careful about applying for too much credit, especially in the month or two before you plan to car shop. Each hard inquiry can reduce your score by a few points. That doesn’t apply to shopping around for the best rate on a loan, though: credit bureaus count multiple inquiries for the same type of

loan as one inquiry, as long as they’re within a short period of time (45 days for FICO). And when you apply for a loan at Outside Financial, we do a soft pull, which doesn’t affect your credit. Ready to see the rates you qualify for? Apply today, without affecting your credit score!