Download

1 / 23

230 likes | 241 Views

This article explores the four options for dealing with distressed real estate loans and discusses the lender remedies available after default. It covers short sales, lender remedies while foreclosure action is pending, and the theory of the mortgage in relation to lender remedies. The article also discusses the possibility of physical possession and the assignment of rents as potential remedies for lenders.

E N D

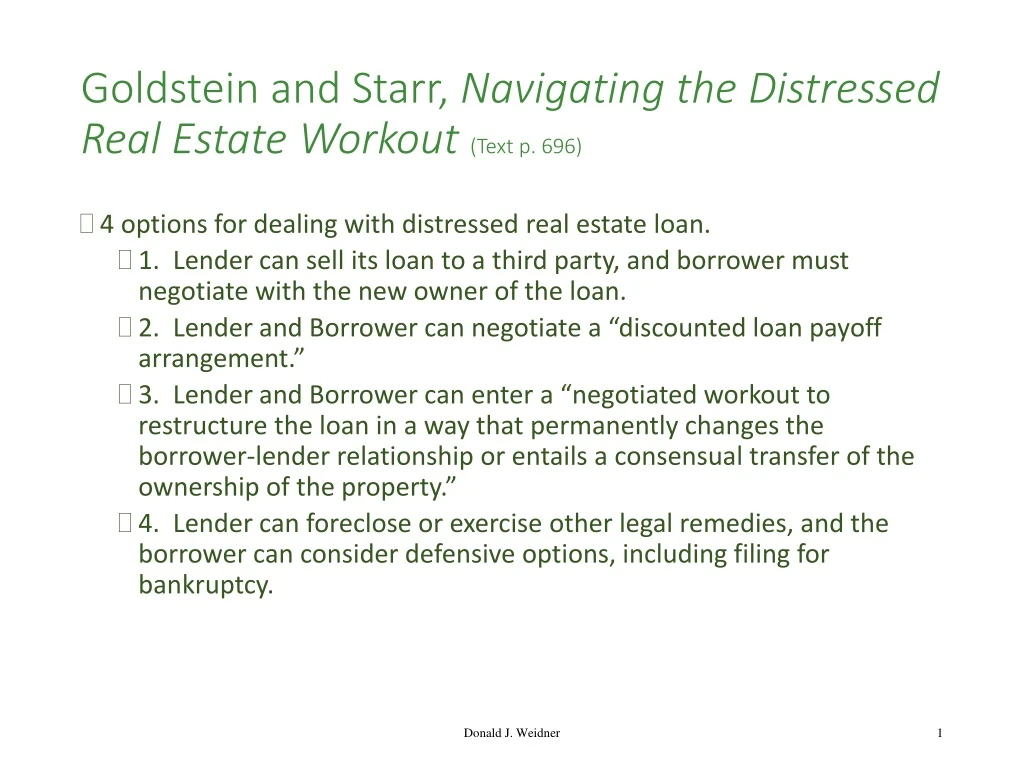

Goldstein and Starr, Navigating the Distressed Real Estate Workout (Text p. 696) • 4 options for dealing with distressed real estate loan. • 1. Lender can sell its loan to a third party, and borrower must negotiate with the new owner of the loan. • 2. Lender and Borrower can negotiate a “discounted loan payoff arrangement.” • 3. Lender and Borrower can enter a “negotiated workout to restructure the loan in a way that permanently changes the borrower-lender relationship or entails a consensual transfer of the ownership of the property.” • 4. Lender can foreclose or exercise other legal remedies, and the borrower can consider defensive options, including filing for bankruptcy. Donald J. Weidner

Lender Remedies After Default by Borrower A Lender that does not sell the loan to a third party or negotiate a discounted payoff from the borrower, has the following basic choices: (1) accept the proceeds of a sale to a third party in satisfaction of the mortgage (“short sale”); (2) accept a deed from the borrower in lieu of a foreclosure proceeding against the borrower (“deed in lieu”); (3) file an action to foreclose; or, (4) in states that permit it, foreclose pursuant to state law that authorizes foreclosure by out-of-court sale. Donald J. Weidner

“Short Sales” • A “short sale” takes place when a lender accepts, in satisfaction of a mortgage, the net proceeds of a sale by the borrower to a third party, even though the proceeds are less than the amount due on the mortgage. • A lender is more likely to entertain a short sale if the property is worth less than the amount of the mortgage and a deficiency judgment against the borrower is either theoretically or practically improbable. Donald J. Weidner

“Short Sales” (cont’d) • Short sales permit lenders to avoid: • The delays incident to foreclosure. • The costs of foreclosure. • The carrying costs or management responsibilities incident to owning property upon consummation of foreclosure. • The costs of reselling property acquired through foreclosure. • The appearance of too many “REO” properties (real estate owned as a result of foreclosure) on its books. Donald J. Weidner

Lender Remedies While Foreclosure Action is Pending • There are 3 remedies a lender might seek while a foreclosure action is pending: • 1. Physical possession of the mortgaged property. • 2. Assignment of rents from the mortgaged property. • 3. Appointment of a receiver to take charge of the mortgaged property. Donald J. Weidner

Lender Remedies After Default, Prior to Foreclosure (cont’d) • In the area of Lender remedies after default and prior to foreclosure, the theory of the mortgage has some, although limited, predictive value. Recall the three theories are: 1. Lien—A mortgage is only a lien, that is, a right to obtain title and possession by prosecuting a foreclosure action to completion. 2. Intermediate—A mortgage is initially only a lien, but title, and the right to possession, passes to the mortgagee when the mortgagor defaults 3. Title—A mortgage is a conveyance that passes title, and the right to possession, as soon as it is executed. Donald J. Weidner

Lender Remedy # 1: Physical Possession From Lifton, Real Estate in Trouble, 31 Business Lawyer 1297 (1976) (not in text): • “Even in the title and intermediate states, modern courts are reluctant to grant a mortgagee physical possession of the property.” • Even if physical possession is possible, “restraints on the mortgagee and the risks of possession may dissuade lenders from seeking it.” Depending upon the jurisdiction a mortgagee in possession: • may have limited power over the property; • may not be compensated for its own management efforts and may not be able to recover money it spends to improve or to maintain the property; and • may risk having to account to the owner under stringent accounting rules for decisions on renting and operating the property if the owner later redeems. Donald J. Weidner

Lender Remedy # 2: Assignment of Rents Lifton article (cont’d): • Rather than seek physical possession, “the lender will usually look to the traditional remedies granting constructive possession. These are contained in standard mortgage provisions for • assignment of rents and for • appointment of a receiver in case of default.” • “Generally, an assignment of rents can be activated in title, intermediate and some lien states (such as Florida) by the mortgagee’s serving notice on the tenants . . . to pay their rents to the mortgagee.” • See the Florida assignment of rents Statute 697.07 (next slide) • Most courts prefer to appoint an independent receiver. Donald J. Weidner

Florida Assignment of Rents § 697.07 • Purpose: to avoid the necessity of getting a receiver appointed to collect rents. • If a mortgage or separate instrument provides for an assignment of rents to secure repayment of an indebtedness, “the mortgagee shall hold a lien on the rents, and the lien created by the assignment shall be perfected and effective against third parties upon recordation of the mortgage or separate instrument with the public records of the county in which the real property is located . . . .” §§ 690.07(1) and (2). • The assignment is enforceable “upon the mortgagor’s default and written demand for the rents made by the mortgagee . . . .” § 690.07(3). • Therefore, on this issue, Florida is not the strictest of lien states Donald J. Weidner

Florida Assignment of Rents Statute 697.07 (cont’d) • Upon application by either the mortgagor or the mortgagee, in a foreclosure action, a court “may require the mortgagor to deposit the collected rents into the registry of the court, or in such other depository as the court may designate.” § 697.07(4). • The court may authorize the use of the collected rents to pay “the reasonable expenses solely to protect, preserve, and operate the real property, including, without limitation, real estate taxes and insurance,” and to make payments to the mortgagee. §§ 697.07(4)(a) and (c). • “The court shall expedite the hearing on the application by the mortgagee or mortgagor to enforce the assignment of rents.” § 697.07(6). Donald J. Weidner

Assignment of Rents in Bankruptcy • In re Town Center Flats, LLC v. ECP Commercial II LLC, No. 16-1812 (6th Cir. 2017). • Bankruptcy court held that that an assignment of rents clause created a security interest, but did not change ownership. It held that the debtor continues to have a property interest in rents, which therefor remained in the debtor’s bankrupt estate. • District Court REVERSED and the 6th Circuit agreed. The Debtor “did not retain sufficient rights in the assigned rents under Michigan law for those rents to be included in the bankruptcy estate.” Donald J. Weidner

Lender Remedy # 3: Appointment of Receiver Lifton article (cont’d): • States vary in their approach to appointment of a receiver: • At one extreme, an agreement to appoint a receiver is usually sufficient to support an appointment. • In the middle, some states will appoint a receiver if there is proof: • that the security is impaired (courts differ on what constitutes impairment) and/or • that the borrower is insolvent. • At the other extreme, it is almost impossible to obtain a receiver. Donald J. Weidner

Lender Remedy # 3: Appointment of Receiver (cont’d) • Drawbacks of the Remedy of Appointment of a Receiver: • It can take a long time to get a receiver appointed. • The receiver may not be a good manager. • The receiver’s fees may eat up a good portion of the income. • Many lenders will simply choose to accept a deed in lieu of foreclosure. • Which can have risks. Donald J. Weidner

CUNA Mortgage v. Aafedt (Text p. 704) 3 notes to finance 3 townhouse purchases 1985 Borrower Credit Union 3 Mortgages to secure notes HUD insured the Mortgages Credit Union Assign Ns & Ms CUNA Assignee Defaulted 1989 Borrower Commenced action to foreclose, stating it will not seek Deficiency .Judgment. CUNA Assignee CUNA Assignee Offers Deeds in Lieu of Foreclosure Rejects offer because CUNA’s mortgage insurer, HUD, said it would not reimburse CUNA if all CUNA could assign to HUD was a title acquired by a Deed in lieu of Foreclosure. CUNA filed foreclosure action Borrower Executed Quitclaim Deeds of 3 properties and records them w/out CUNA’s knowledge Borrower Moved to dismiss foreclosure action because it executed the Deeds in lieu of foreclosure Borrower Donald J. Weidner

CUNA Mortgage v. Aafedt (cont’d) • CUNA said its ability to receive the mortgage insurance proceeds from HUD would be impaired if it accepted a deed in lieu rather than title through foreclosure. • Trial Court: • 1. Quitclaim deed was void [it was a unilateral act without CUNA’s consent, acquiescence, and hence there was no delivery]; and • 2. CUNA was entitled to bring the foreclosure proceeding. Donald J. Weidner

CUNA Mortgage v. Aafedt (cont’d) • Normally, recording a deed creates a rebuttable presumption of its delivery to, and its acceptance by, the grantee. • However, the presumption of acceptance arises only if the deed is beneficial to the grantee, not when the deed places a burden on the grantee. • Here, CUNA’s refusal to accept a deed in lieu was not in bad faith. Donald J. Weidner

Lender Wariness of Deeds in Lieu of Foreclosure Lenders are wary of “deeds in lieu” for a variety of reasons: 1. If bankruptcy is filed against the debtor within 90 days of the conveyance, a deed in lieu may be set aside as a preference. • Many title companies won’t insure on a deed in lieu until the 90-day preference period has passed. 2. Another possibility, though less likely, is that, if bankruptcy is filed within a year of the conveyance, it may be deemed a fraudulent transfer. Donald J. Weidner

Lender Wariness of Deeds in Lieu of Foreclosure (cont’d) 3. A voluntary conveyance from the owner does not cut off junior mortgagees or mechanics lien claimants. • Therefore, a foreclosure action may still be necessary to wipe out those liens. • Also: a junior lienor may argue, under the merger doctrine, that it is now the senior lien. • In short, if intervening liens are discovered, “the only prudent alternative for the mortgagee is to foreclose.” • In some states, the tax on voluntary transfers may be very high—based on the total value of the property (unreduced by the mortgage). Donald J. Weidner

Lender Wariness of Deeds in Lieu of Foreclosure (cont’d) • There is a difference between theory and practice as state courts consider deeds in lieu. • In theory: • The rule against contemporaneous clogs on the equity of redemption does not apply to transactions subsequent to the original mortgage • Most courts permit the mortgagee to purchase the mortgagor’s equity of redemption. Donald J. Weidner

Lender Wariness of Deeds in Lieu of Foreclosure (cont’d) • However, in practice, courts examine a deed in lieu to assure it is: 1. Free from fraud. 2. Based on an adequate consideration; and 3. Is truly subsequent to the mortgage and not contemporaneous with it (not put in escrow when the mortgage was first executed). Donald J. Weidner

Lender Wariness of Deeds in Lieu (cont’d) 5. Theory versus practice and deeds in lieu (cont’d) • Courts are concerned with the disparity in bargaining strength between a lender and a borrower in default. • There are two situations in which the courts are more likely to be especially solicitous of the borrower: 1. If the transaction might be construed “as unfair and unconscionable,” • “especially if the consideration paid is disproportionately less than the value of the equity or if none is paid where the equity has value.” 2. Nonrecourse Debt. If “the deed is not by the mortgagor, but by a non-assuming grantee of the mortgagor, a release of the debt, since there was no personal liability, would be no consideration for the conveyance . . . and subject it to being set aside.” Donald J. Weidner

Lender Wariness of Deeds in Lieu (cont’d) 5. Theory versus Practice (cont’d) • “[T]here is always the possibility that a court will construe the [deed in lieu] as simply another mortgage transaction.” • “If the mortgagor is successful, he will be treated as a mortgagor under two mortgages—under the original mortgage which was not eliminated by the deed in lieu and under the deed in lieu treated as a second mortgage.” • “[T]he possibility [also] exists that because of insolvency of the mortgagor or an actual intent on his part to defraud creditors the conveyance may be subject to avoidance at the suit of creditors outside of bankruptcy.” Donald J. Weidner

Post Foreclosure Lender Remedy • Fla. Stat. § 702.06: “In all suits for the foreclosure of mortgages heretofore or hereafter executed the entry of a deficiency decree for any portion of a deficiency, should one exist, shall be within the sound discretion of the court . . . . The complainant shall also have the right to sue at common law to recover such deficiency, unless the court in the foreclosure action has granted or denied a claim for a deficiency judgment.” • In Dyck-O’Neal, Inc. v. Lanham, So.3d , 2018 WL 3301567 (Fla. 2018), a foreclosure court had expressly reserved jurisdiction in its final judgment to handle a deficiency claim, without actually deciding the claim on its merits. The Florida Supreme Court held that the lender could nonetheless pursue an independent action at law for a deficiency judgment, relying on § 702.06. Reserving jurisdiction on the matter does not preclude other courts from exercising their jurisdiction of the matter. • We close on this final reminder of the distinction between the note and the mortgage. Donald J. Weidner