Download

1 / 38

380 likes | 644 Views

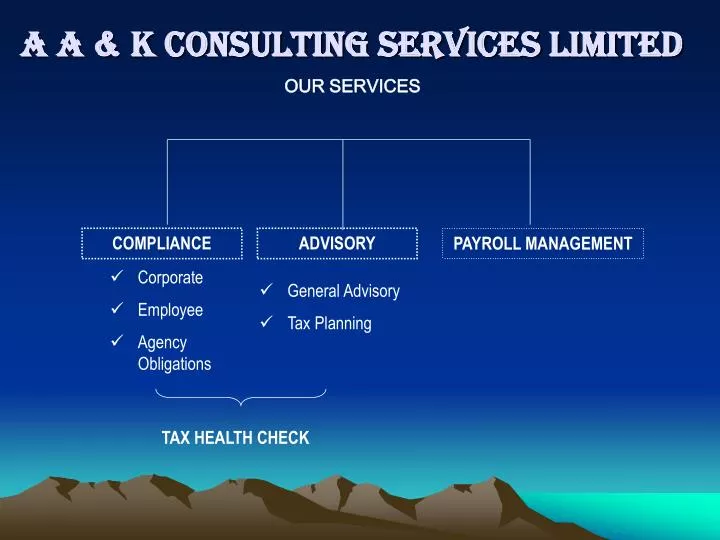

OUR SERVICES. COMPLIANCE. ADVISORY. PAYROLL MANAGEMENT. Corporate Employee Agency Obligations. General Advisory Tax Planning. TAX HEALTH CHECK. A A & K CONSULTING SERVICES LIMITED. CONTEMPORARY TAX ISSUES. Integration of Revenue Agencies

E N D

OUR SERVICES COMPLIANCE ADVISORY PAYROLL MANAGEMENT • Corporate • Employee • Agency Obligations • General Advisory • Tax Planning TAX HEALTH CHECK A A & K CONSULTING SERVICES LIMITED

CONTEMPORARY TAX ISSUES • Integration of Revenue Agencies • Tax Policy Initiatives in 2011 Budget In 2010 two major tax policy initiatives were introduced:

INTEGRATION OF REVENUE AGENCIES Ghana Revenue Authority (GRA) Act 2009 [Act 791] merged: • Internal Revenue Service (IRS) Act 592, • VAT Service Act 546 and • Customs Excise & Preventive Service (CEPS) [PNDC Law 330]

MINISTRY OF FINANCE & ECONOMIC PLANNING [MOFEP] BOARD OF DIRECTORS IRS COMMISSIONER VAT SERVICE COMMISSIONER CEPS COMMISSIONER PRE MERGER

MINISTRY OF FINANCE & ECONOMIC PLANNING [MOFEP] BOARD OF DIRECTORS GHANA REVENUE AUTHORITY COMMISSIONER-GENERAL [GRA] DOMESTIC DIVISION COMMISSIONER CUSTOMS DIVISION COMMISSIONER GENERAL SERVICES COMMISSIONER POST MERGER

EFFECT OF INTEGRATION All powers of pre-integration Commissioners are now vested in the Commissioner-General e.g. • Final Authority for Interpretation • Practice Notes • Private Rulings

COMMENTARY ON TAX POLICY INITIATIVES IN THE 2011 BUDGET STATEMENT • SUMMARY OF MAJOR TAX INITIATIVES Domestic tax initiatives include: • Increases in tax rates and thresholds for withholding taxes and VAT • Removal of Tax Holidays • Extension of National Fiscal Stabilization Levy • Revision of personal tax rates • Extension of coverage of Communications Service Tax • Review of Exemptions and Zero-rated items under the VAT Act • Review of Excise Duty Rates

COMMENTARY ON TAX POLICY INITIATIVES IN THE 2011 BUDGET STATEMENT International tax initiatives include: • Increases in Duty rates • Review of operations of Bonded warehouses • Import tax on rice and poultry products

REVIEW OF WITHHOLDING TAX REGIME Introduction Withholding taxes on payments by residents to: • Non-residents for the supply of services • Residents for supply of goods and services • Other withholding taxes (Section 86 of Act 592)

PAYMENTS TO NON-RESIDENTS FOR SERVICES SUPPLIED TO GHANA • Current Position Section 3 of Act 592 imposes a final withholding tax on the following payments ServiceTax Rate (%) Dividend 8 Interest 8 Royalty 10 Endorsement Fees 15 Rent 10 Management & Technical Service Fees 15 • No changes have been proposed in the 2011 fiscal policy statement • Increase in withholding tax on Foreign Supplies of Services

PAYMENTS TO RESIDENTS FOR SUPPLY OF GOODS AND SERVICES BY RESIDENTS • Current Position A withholding tax of 5% applies where the contract sum exceeds GH¢50.00 • Proposed amendment The threshold raised from GH¢50.00 to GH¢500.00 • Implication • The 5% withholding tax under Section 84 (2) of the Internal Revenue Act 2000 [Act 592] shall apply where the contract sum for the supply of goods and services exceed GH¢500.00

TAX HOLIDAYS • Real Estate Developers – for sale or letting • 5 year Holidays abolished except for • Developers in partnership with Ministry of Works and Housing to provide affordable housing • Issues • Fate of those enjoying holiday uncertain • Hotels and Hospitality Industry • GIPC Regulations, 2005 [LI 1817] providing exemptions for the industry repealed • Desirable LI 1817 provisions to be incorporated in Act 592 and managed by GRA • Amendment is not clear • APEX Bank • Tax Holiday extended to 2014

NATIONAL STABILIZATION LEVY [NSL] Introduction • NSL imposed on 2009 and 2010 profit before tax • The tax rate of 5% of profit before tax • The levy is not tax deductible Proposed Amendment • The imposition of the levy is to be extended by one year

GIFT TAX • The Internal Revenue Act 2000 imposes a gift tax at the rate of 5% on taxable gifts exceeding Gh¢50.00 Proposed Amendment The rate of tax imposed on taxable gifts is to be increased to 15%.

MINING ROYALTIES Introduction • Mineral royalties are paid by mining companies at the rate of 3% to 6% • The royalty is paid quarterly Proposed Amendments • Mineral royalties to be accounted for on monthly basis by the 15th of the following month

CHANGES IN INDIVIDUAL TAX RATES AND RELIEFS Proposed Amendment • Increase in tax free Chargeable Income from GH¢1,008.00 to GH¢1,104.00 • Increases in amount granted as reliefs to individuals proposed • Chargeable Income above GH¢20,280.00 (2010 GH¢16,200.00) to be taxed at 25%

INITIATIVES UNDER INDIRECT TAXES OBJECTIVES 2 Types of VAT Schemes (i) VAT Invoice Scheme (VIS) • Retailers with a minimum turnover of GH¢10,000.00 (ii) VAT Flat Rate Scheme (VFRS) • Retailers under GH¢10,000.00 currently operate under VFRS. • The tax rate is 3% on selling price • No input tax credit is available for them.

COMMUNICATIONS SERVICE TAX (CST) Introduction • Introduced in 2008 - passage of the Communications Service Tax Act, 2008 (Act 754). • The tax applied to Class1 Telecom Operators • Class 1 License Telecom Operator authorized to provide public communication service - National Communications regulations,2003 (LI 1719). • Public communications service - service made available to the general public for a fee or charge without discrimination (LI 1719)

COMMUNICATIONS SERVICE TAX (CST) cont’d • Private communications service is a service established by an individual, a body corporate or other legal entity to satisfy its own communications needs. • LI 1719 defines communication service to include the following: • Telecommunications services • Broadcasting services • Cable services • Satellite services • Value added services • Aeronautical services • Maritime services • Communications services may be provided as public or private services

PROPOSED AMENDMENT • CST coverage to extend to all companies and persons within the communication industry. • 2011 budget statement does not clearly state whether the extension of the tax base of CST will include companies with their own private radio communications or other communications services. • Details in relevant legislation to be passed.

RECLASSIFICATION OF DOMESTIC ZERO-RATED SUPPLIES • Locally produced items currently zero-rated • Pharmaceutical Products • Paper for the publishing industry • Agricultural input like cutlasses • Producers and wholesalers currently entitled to refund of input taxes incurred in the production.

RECLASSIFICATION OF ZERO-RATED SUPPLIES Proposed Amendment • Reclassification as exempt items under Act 546 • Companies producing items no more entitled to refunds of input taxes incurred in the course of production. • All input taxes incurred to be incorporated into cost build up.

DEFERRED PAYMENT OF VALUE ADDED TAX • Manufacturers permitted to defer payment of import VAT on imported raw materials. • Practice is allowed to various manufacturers based AGI recommendations. • Practice improved cash flow of the manufacturing companies.

DEFERRED PAYMENT OF VALUE ADDED TAX Proposed Amendment • ‘Reliefing’ manufacturers of import VAT/NHIL on imported raw materials to be abolished. • No legislation is required. • Cash flow implications for affected companies must be factored into current year budget.

INTERNATIONAL TAX INITIATIVES Bonded Warehousing • Imported goods or locally manufactured goods may be stored under Customs control in a Government or private bonded warehouse. • Deferral of payment of duty and taxes until the goods are needed for home consumption or for export. • Bonded warehousing is allowed for both finished products and raw materials for manufacturing. • The goods may be re-entered for warehousing after two years.

INTERNATIONAL TAX INITIATIVES Proposed Amendment • Bonded warehousing facility to be restricted only to raw materials for manufacturing. • Importers of finished goods will not be allowed to warehouse them for up to two years • The proposed amendment is likely to define the maximum period that importers will be allowed to warehouse finished goods

IMPORT DUTY ON RICE AND POULTRY PRODUCTS • The revised rates will apply in Ghana upon ratification by ECOWAS.

OTHER TAX INITIATIVES Exemptions from payment of import duty • Energy saving lamps, LED lamps and • Raw materials for local companies producing energy saving bulbs • New taxes imposed • An environment tax on plastic packaging materials and products

DOUBLE TAXATION AGREEMENT BETWEEN THE REPUBLIC OF GHANA AND THE FRENCH REPUBLIC INTRODUCTION What is Double Taxation? Double Taxation has been defined as the imposition of comparable taxes in two or more states on the same taxpayer in respect of the same subject matter. Negative Effects of Double Taxation It results in multiplicity of taxes It inhibits the free flow of investment and trade activities Purpose of Double Taxation Agreements Due to the negative effects of Double Taxation, nations have deemed it expedient to enter into Double Taxation Treaties toward attainment of the following:

Removal of Tax Barriers to Trade and Investment • Resolution of Tax Disputes • Removal of uncertainties about a country’s Tax regime • Promotion of Investment through the granting of Tax Incentives • Reduction/Elimination of Tax Avoidance Schemes through the provision of a framework of co-operation between Tax Authorities LEGAL AUTHORITY FOR GHANA TO ENTER INTO DOUBLE TAXATION ARRANGEMENTS • Provided for in Section 111 of the Internal Revenue Act 2000 (Act 592) • Under Section 111 (1) of Act 592, the DTA prevail over the provisions of the Act

PROCESS OF RATIFICATION • Each contracting state has to ratify the convention and give notice to the other through diplomatic channels before the entry into force • In Ghana the ratification is done by Parliament in accordance with Article 75 (2) of the 1992 Constitution of the Republic of Ghana ENTRY INTO FORCE • Normally, the convention is entered into force on the day the latter of the notification is received • The provisions of the Convention normally have effect on the commencement of the fiscal year next following that in which the Convention was entered into force BASIS FOR TAXING EACH REVENUE ITEM Source of Revenue – e.g. Directors Fees. Employment etc Residence of tax payer – e.g. Business Profit, Air and Shipping Transport Sharing – e.g. Dividends, Interest, Royalties etc. shared between Treaty Partners

PERSONAL SCOPE • It indicates that the convention is applicable to persons who are residents of one or both of the contracting states

CONDITION PRECEDENT OR PROOF TO BE FURNISHED BY A RESIDENT OF THE OTHER CONTRACTING STATE SECTION 111 (4) OF ACT 592 To benefit from a reduction in the Ghanaian Rate of Tax or exemption from Ghanaian tax, a Resident of the other contracting state is required to provide the proof below to the Commissioner-General of the Ghana Revenue Authority. • That no individual(s) resident outside the contracting state owns 50% or more of the underlying ownership of that person’s business. The essence of the proof is to prevent ‘Treaty Shopping’ that is a situation where a resident of a non-contracting state tries to enjoy the benefits of a Double Taxation Agreement between two other states.

BASIS FOR TAXING REVENUE ITEM UNDER GHANA/FRANCE DOUBLE TAXATION AGREEMENT

BASIS FOR TAXING REVENUE ITEM UNDER GHANA/FRANCE DOUBLE TAXATION AGREEMENT

COMPARISON BETWEEN LOCAL RATES AND RATES UNDERGHANA/FRANCE DOUBLE TAXATION AGREEMENT NOTE:Under dividends in the DTA, the rates of 5% or 7.5% Are applicable where the beneficial owner has at least 10% Interest in the company paying the Dividend.

CONCLUSION Double Taxation Treaties provide some tax incentives and exemptions that pave the way for the free flow of trade and investment activities. It is important for residents of the contracting states to acquaint themselves with the provisions of the relevant conventions so as to take full advantage of the opportunities therein.