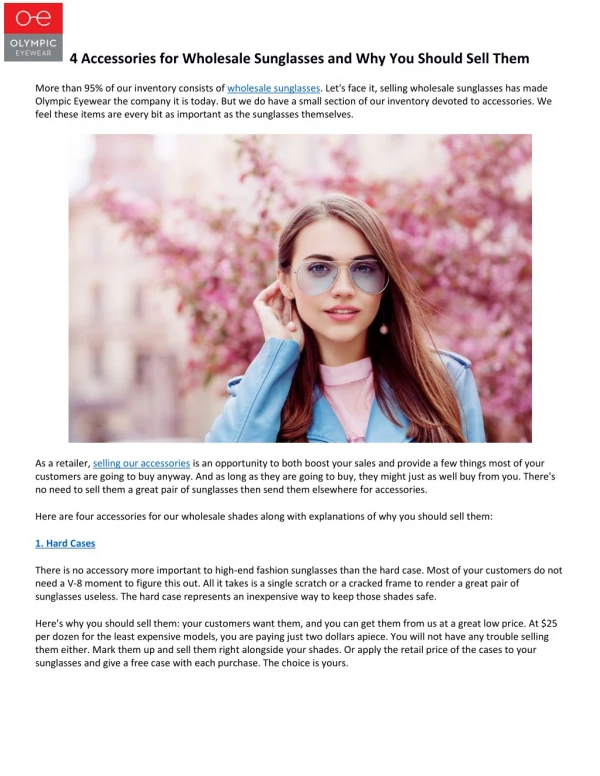

Download

1 / 46

460 likes | 654 Views

Why you should Sell Prudential LTC3. IFS-A148588 Ed. 06/2008. Key Features and Benefits that make Prudential’s LTC3 the Product you Want to Sell. LTC3 SM : Philosophy & Purpose. Offer our consumers a product with STRENGTH of Company

E N D

Why you should Sell Prudential LTC3 IFS-A148588 Ed. 06/2008

Key Features and Benefits that make Prudential’s LTC3 the Product you Want to Sell

LTC3SM: Philosophy & Purpose • Offer our consumers a product with • STRENGTH of Company • FLEXIBILITY: Choice on how they want to be paid at time of claim • FOCUS: on the problem • VALUE: Key Features that are Built-In

Issue Ages: 18-79 Daily Benefit: $50-$500 Benefit Periods: 2,3,4,5,6,10 & lifetime Calendar Elimination Period: 30, 60,90, 120, 180, 365 120, 180 & 365 N/A in some states Home Health Care: 50%, 75%, 100%, 150% of facility daily benefit LTC3: Product Features

LTC3: Calendar Day Elimination Period • Built-In • Begins from date chronic illness or disability is certified by licensed health care practitioner • Services not required to “trigger” and/or satisfy elimination period • Can receive care from family member during EP • Elimination period days are: • Cumulative • Need to be met only once per lifetime

How Does the Competition Measure Up? Source: LTC Advisor (StrateCision Benefit Comparison Software), current as of September 2008

LTC3: Cash Solutions Three “Cash” Solutions to offer your clients based on their personal & financial needs: 1. Cash Alternative Feature (built-in) 2. Cash Benefit Optional Rider (“CBO”) 3. Flex Cash Benefit Optional Rider (“50/50”) • Prudential does NOT sell an LTC policy • that doesn’t have a Cash Benefit in it!

LTC3: Cash Alternative Client becomes eligible for benefits • At claim time choose Reimbursement for eligible charges up to 100% of Home Care Daily Benefit OR • Receive 40%* of Home Care Daily Benefit in Cash (remaining 60% of benefit stays in “pool of benefits” to be used later) *In CA, 50% of HHC DBA Choice of reimbursement or cash can be made at end of each month Choice of

Cash Alternative Example $ 4,500 monthly benefit= $4,500 reimbursement Or $1,800 cash You decide at the end of each month

How Does the Competition Measure Up? Source: LTC Advisor (StrateCision Benefit Comparison Software), current as of September 2008

LTC3: 50-50 Flexible Cash Benefit Option • Cash Benefit = 50% of client’s Home Care Daily Benefit x number of days in month • Amount paid whether or not charges are incurred • No proof of charges or submission of bills is necessary – just a claim form to fill out • Remaining 50% is paid for reimbursement of eligible charges in the same calendar month your client receives cash portion 9

LTC3: 100% Cash Benefit Option • 100% of monthly benefit is paid in cash • Provides greatest level of flexibility • No receipts, no bills, no proof of services • Adds about 70% to the Premium Example: $150 DBM with 100% HHC $150 x 30 days = $4,500 monthly benefit $4,500 paid in cash each month 14

How Does the Competition Measure Up? Source: LTC Advisor (StrateCision Benefit Comparison Software), current as of September 2008

Cash: Sales Ideas • Help “professional” clients overcome the gap of their catastrophic disability coverage • i.e. physicians & attorneys, Sales Execs • Coverage for someone who does not earn an income, such as stay-at-home parents • Assist paying for services on an “uninsured” spouse at time the “insured” spouse goes on claim • Provides coverage outside the U.S. • Offer cash-enhanced policy to clients with reimbursement policy 16

LTC3: Home Care Daily Benefit (HCB) Percent Of Facility Care Daily Benefit 50%, 75%, 100%, *150%Services Covered -Adult Day Care - Homemaker Services - Personal Care - Home Health Care*Not available with Cash Benefit Rider, Flexible Cash Rider or Unlimited Lifetime Maximum. The 150% Home Care Daily Benefit Option can only be selected with a Facility Daily Benefit of $350 or less.

Prudential’s 150% Home Care w/Lower Nursing Home Facility Daily Benefit (FDB) • Most Companies - $210/Day w/100% Home Care • Policy with $210/Day and 100% Home Care provides up to $210 for Confined Care and $210 for Home Care • With Prudential LTC3 you can also choose $210/Day w/100% Home Care; OR • LOWER THE PREMIUM by selecting $140/Day w/150% Home Care • LTC3 Policy $140/Day and 150% HHC provides up to $140 for Confined Care and $210 for Home Care

Cash Alternative Benefit and 150% HHC Get even more out of the Cash Alternative Benefit by utilizing the 150%* Home Care Daily Benefit option Monthly cash amount when electingCash Alternative Benefit (40%**) = $3,600 *The 150% Home Care Daily Benefit Option can only be selected with a Facility Daily Benefit of $350 or less. ** In CA, 50% of HHC DBA

How Does the Competition Measure Up? Source: LTC Advisor (StrateCision Benefit Comparison Software), current as of September 2008

Direct Payments to All IndependentHome Care Professionals • Home health aides, registered nurses, licensed practical nurses, etc. qualify for Direct Payment without agency involvement. • All licensed family members also qualify for Direct Payment.

Family as Caregivers • Licensed family members (including live-in spouses) are not excluded from being paid for their services in any LTC care setting. • Unlicensed family members may be paid under the built-in Cash Alternative Benefit or either of the two Cash Benefit options.

How Does the Competition Measure Up? Source: LTC Advisor (StrateCision Benefit Comparison Software), current as of September 2008

LTC3SM: Waiver of Elimination Period for Home Care Option • What is it? • Waives Calendar Day Elimination Period (EP) for reimbursable Home Care services • How does it work? • Policyholder receives policy benefits that reimburse covered Home Care expenses without having to satisfy the Elimination Period – paid from day one • Days that are waived (Home Care services are received and benefits are paid) count toward satisfying EP for Cash Alternative benefits (and other policy benefits) • Where is it available: CO, NV, GA, KS, OR, WI, AK, DC, IL, IA, MN, MS, NE, ND, RI, SC, AL, AR, CT, ID, ME, MI, MO, NH, OH, SD, WV, WY • Considerations • Cannot be used with 120, 180, and 365 Day EPs • EP must still be satisfied to access Cash Alternative and Facility benefits and for premiums to be waived under the Waiver of Premium feature

Prudential LTC3 Restoration of Benefits • Included in Policy – not an option • If a previously eligible client is assessed and found to no longer have chronic illness or disability, and status is maintained for six consecutive months, restoration of benefits can restore to full lifetime maximum • Consideration • Can be 1 ADL deficient and still restore benefits • Benefits can only be restored once in a lifetime

Prudential LTC3 Restoration of Benefits • Companies are now charging significantly higher premiums for Unlimited Benefit Period policies • More LTC policies being sold with BPs that are shorter than unlimited • Clients concerned about using up benefits with an early claim (accident, stroke, etc.) • Advances in Medicine & Technology

How Does the Competition Measure Up? Source: LTC Advisor (StrateCision Benefit Comparison Software), current as of September 2008

Home Support Services • This essential built-in component (50 X Facility Daily Benefit) now covers durable medical equipment, home modifications, assistive devices, caregiver training, emergency response systems, and transportation services for medically necessary health care included in the Plan of Care. • Unlike some of our competitors, these expenses can be incurred in addition to qualified LTC expenses without regard to daily or monthly maximums.

How Does the Competition Measure Up? Source: LTC Advisor (StrateCision Benefit Comparison Software), current as of September 2008

Private Care Consultant (built-in) • Independent Care Management: Advises client and family • No Elimination Period • Additional Annual Pool: 20X Facility Benefit • No Reduction in Lifetime Maximum Benefit

How Does the Competition Measure Up? Source: LTC Advisor (StrateCision Benefit Comparison Software), current as of September 2008

LTC3SM: Inflation Protection Options • NONE • Guaranteed Purchase Option • Automatic 5% Simple Inflation Benefit • Automatic 5% Compound Inflation Benefit – 2x Maximum • Automatic 5% Compound Inflation Benefit – No Maximum • Automatic 3% Compound Inflation Benefit – No Maximum

LTC3SM: Guaranteed Purchase Option (GPO) • What is it? • Increases will occur automatically every 3 years unless the offer is refused in writing (negative election) • Benefits will increase by 5% of the current policy benefit amount, compounded annually over the 3 year period only; “catch-up” no longer offered • No evidence of insurability is required • Increased coverage is rated at insured’s attained age • Increases made even if insured is benefit eligible or on claim • Offers continue as long as policy in-force even if premium waived • Considerations • Cannot be purchased with 10 Pay or Paid Up At Age 65, Premium Reduction at Age 65, Joint or Survivor Waiver of Premiums, or Shared Care

LTC3SM Inflation OptionsPremium & Benefit Comparison NW Rates (ME) – Age 55 Annual Premiums, $150/Day, 100% HHC, 90 EP, 5 yr. Benefit Period ($273,750 TLB at issue), Standard 1 rates, 2-Spouse Discount - For illustrative purposes only

How Does the Competition Measure Up? Source: LTC Advisor (StrateCision Benefit Comparison Software), current as of September 2008

Partner Discounts*30% for 2 insured & 15% for 1 insured • One-year relationship window is one of the shortest in the industry. • Where allowed by law, no partner combination (i.e., same-sex, mother-daughter, brother-sister, etc.) is excluded from receiving this discount. * Discounts may vary by state.

How Does the Competition Measure Up? * Discounts and restrictions may vary by state. Source: LTC Advisor (StrateCision Benefit Comparison Software), current as of September 2008

LTC3SM: Premium Payment Options • Lifetime • Premiums are paid until waived or policy ends or lapses • Premium Reduction at Age 65 • Premiums reduced by 50% at age 65 • Available to ages 60 or younger • 10 Year Paid Up • Premiums paid for 10 years • Available to ages 40 - 75 • Paid Up at Age 65 • Premiums paid until age 65 • Available to ages 54 and under

Premium Sweet Spots • Monthly Payment Mode premiums can be less expensive than those of our major competitors (only 2% more than Annual when electronic funds transfer is chosen). • 6-year benefit period is approximately 5% more than 5-year benefit period. • 150% Home Health Care Rider is only 12% more than 100% Home Health Care. • Shared Care is approximately 7-10% for 4-10 benefit years.

Premium Sweet Spots (continued) • With John Hancock’s and Genworth’s refreshed pricing* (i.e., price increase on new business), premiums are now comparable to those of Prudential. • The built-in benefits of the Prudential policy should be able to overcome most any price differential. • When we incorporate monthly payment mode, often times Prudential’s premium is lower than that of our competitors. *Refreshed pricing pertains to John Hancock Custom Care II Enhanced and Genworth Privileged Choice 2007 plans, among others.

How Does the Competition Measure Up? Source: LTC Advisor (StrateCision Benefit Comparison Software), current as of September 2008

NEW IN 2009! Employer Sponsored Program (ESP) Highlights • NEW: Age Requirements for simplified Underwriting 18-65 • NEW: Minimum participation requirement for Simplified Issue • 7 to 200 employees (7 employees must be issued) • 201 size groups and more (4% of eligible employees must be issued) • NEW: Participation requirement parameters • “100% of class” no longer required • Spouses/partner will not count toward participation requirement • NEW: Discounts • 5% discount to employees and spouse/partner • 5% discount to family members* • No maximum on discounts * Parents, in-laws, aunts, uncles, siblings, grandparents, grandparents in-law, and children ages 18 and older.

NEW IN 2009! Employer Sponsored Program (ESP) Highlights • NEW: Employer Sponsored Groups of 2-6 Employees • Full Underwriting – Simplified issue not available to Employees or Spouses/Partners • 5% ESP Discount • If applicant qualifies for Preferred Rates, Preferred Rates will be in addition to (NOT in lieu of) 5% ESP Discount • No minimum participation requirements • Requirements for case approval: Similar to Affiliation Discount Program

Affiliation/Association Program Highlights • Qualification • Association formed for common purpose* • Businesses may also qualify for discount** • Participation requirement • NONE • Program Features • 5% discount for members & extended family • Full underwriting • Unlimited benefits and riders available *Other than to buy insurance. Other restrictions may apply. **May not be used in combination with ESP. 23

Finding the Right Associations • Religious Organizations • Medical/Health Associations • Alumni Associations • Universities & Colleges • Target Market Associations (Women’s Business Group) • Bank Customers • Homeowners Association • Local Chambers of Commerce • Credit Unions • Condominium Associations

Loyalty Discount Program • Program Features • 5% discount • Full underwriting • All benefits, riders, and marital/partner discounts are available • Discount will notbe removed if policyholder lapses/terminates current Life or Annuity contracts • Compensation Reduction applies • Available in ALL States except: • CA, OR, NV, UT, MN, KY, WV, NY and NJ

How to Request the Discount • Complete the Plan Design page on the application • Under the Affiliation section, write in discount code “00618” • Next to Affiliation name, write in “Loyalty” and the client’s Life Policy # or Annuity Contract #

LTC3SM: Exclusions* • Illness, treatment or medical conditions arising out of: • War or an act of war • Participation in a Felony, riot or insurrection, or • Alcoholism and drug addiction • Treatment provided in a government facility • Charges for services or supplies normally provided without charge. • Charges for care or treatment provided outside the United States except as described in the International Coverage benefit • Charges for expenses reimbursable under Medicare or for expenses that would be reimbursable under Medicare but for the application of a deductible or coinsurance amount • Benefits under your policy may be reduced if Prudential also pays benefits for Eligible Charges under any other Prudential Individual Long-Term Care Insurance Policy *Summary is for descriptive purposes only. All provisions are subject to the language of the actual policy, including the definitions, terms, conditions and exclusions set forth in the policy and may vary by state.