Download

1 / 28

280 likes | 345 Views

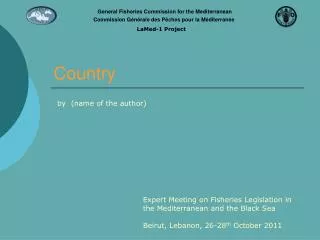

( λ + ω ) investors receive information about Asset 1 ( λ - ω ) investors receive information about Asset 2. ( λ - ω ) investors receive information about Asset 1 ( λ + ω ) investors receive information about Asset 2. λ =0.5, ω =0. Home Country. Foreign Country. Asset 2.

E N D

(λ+ω) investorsreceive information about Asset 1 (λ-ω) investorsreceive information about Asset 2 (λ-ω) investorsreceive information about Asset 1 (λ+ω) investorsreceive information about Asset 2 λ=0.5, ω=0 Home Country Foreign Country Asset 2 Asset 1 1 0

(λ+ω) investorsreceive information about Asset 1 (λ-ω) investorsreceive information about Asset 2 (λ-ω) investorsreceive information about Asset 1 (λ+ω) investorsreceive information about Asset 2 λ=0.5, ω=0.05 Home Country Foreign Country Asset 2 Asset 1 1 0

(λ+ω) investorsreceive information about Asset 1 (λ-ω) investorsreceive information about Asset 2 (λ-ω) investorsreceive information about Asset 1 (λ+ω) investorsreceive information about Asset 2 λ=0.5, ω=0.10 Home Country Foreign Country Asset 2 Asset 1 1 0

(λ+ω) investorsreceive information about Asset 1 (λ-ω) investorsreceive information about Asset 2 (λ-ω) investorsreceive information about Asset 1 (λ+ω) investorsreceive information about Asset 2 λ=0.5, ω=0.15 Home Country Foreign Country Asset 2 Asset 1 1 0

(λ+ω) investorsreceive information about Asset 1 (λ-ω) investorsreceive information about Asset 2 (λ-ω) investorsreceive information about Asset 1 (λ+ω) investorsreceive information about Asset 2 λ=0.5, ω=0.20 Home Country Foreign Country Asset 2 Asset 1 1 0

(λ+ω) investorsreceive information about Asset 1 (λ-ω) investorsreceive information about Asset 2 (λ-ω) investorsreceive information about Asset 1 (λ+ω) investorsreceive information about Asset 2 λ=0.5, ω=0.25 Home Country Foreign Country Asset 2 Asset 1 1 0

(λ+ω) investorsreceive information about Asset 1 (λ-ω) investorsreceive information about Asset 2 (λ-ω) investorsreceive information about Asset 1 (λ+ω) investorsreceive information about Asset 2 λ=0.5, ω=0.25 Home Country Foreign Country Asset 2 Asset 1 1 0 GrossmanStiglitz (1980), Hellwig (1980), Admati (1985): postulateequilibriumprice as a linearfunction of the averagesignals and the aggregate stock supply, find the optimal demands and impose market clearing to solve for the undetermined coefficients.

Privatesignals Normalizedprice signal

GrossmanStiglitz (1980), Hellwig (1980), Admati (1985): postulateequilibriumprice as a linearfunction of the averagesignals and the aggregate stock supply, find the optimal demands and impose market clearing to solve for the undetermined coefficients.