Download

1 / 50

500 likes | 628 Views

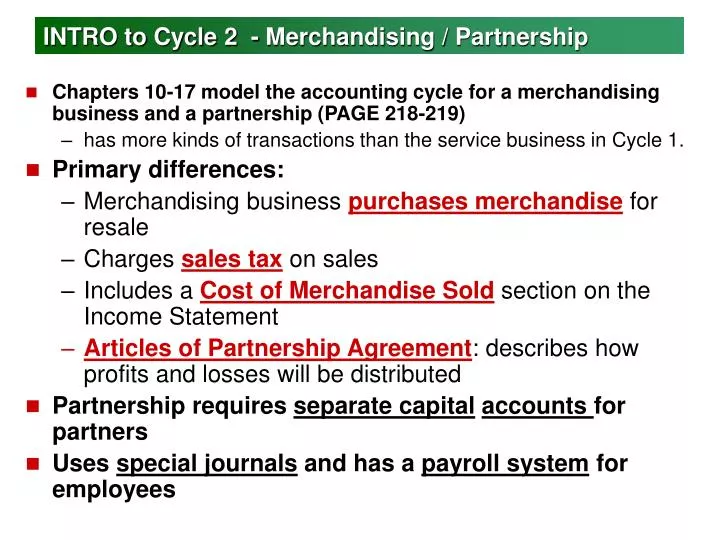

INTRO to Cycle 2 - Merchandising / Partnership. Chapters 10-17 model the accounting cycle for a merchandising business and a partnership (PAGE 218-219) has more kinds of transactions than the service business in Cycle 1. Primary differences:

E N D

INTRO to Cycle 2 - Merchandising / Partnership • Chapters 10-17 model the accounting cycle for a merchandising business and a partnership (PAGE 218-219) • has more kinds of transactions than the service business in Cycle 1. • Primary differences: • Merchandising business purchases merchandise for resale • Charges sales tax on sales • Includes a Cost of Merchandise Sold section on the Income Statement • Articles of Partnership Agreement: describes how profits and losses will be distributed • Partnership requires separate capitalaccounts for partners • Uses special journals and has a payroll system for employees

Chart of Accounts, page 219-220 • Similarities • Several typical divisions of accounts • Assets • Liabilities • OE • Revenue • Expenses • Several familiar accounts within divisions • Differences • New liability and expense accounts have been added for payroll expense and sales tax payable • Two owners – 2 capital and 2 drawing accounts • Cost of Merchandise section • Assets section: Merchandise Inventory • Subsidiary ledger accounts • Accounts Receivable • Accounts Payable

Chapter 10 Journalizing Purchases and Cash Payments Using Special Journals

Objectives: • Define accounting terms related to purchases and cash payments for a merchandising business. • Identify accounting concepts related to purchases and cash payments for a merchandising business. • Journalize purchases of merchandise using a purchases journal. • Journalize cash payments using a cash payments journal. • Total, prove, and rule a cash payments journal and start a new cash payments journal page. • Journalize other transactions using a general journal.

TYPES OF OWNERSHIP – READ PAGE 220 • Proprietorship – Cycle 1 • One person • Partnership – Cycle 2 • Two or more • Combine assets and capital • Share profits/losses • Unlimited liability • Corporation – Accounting II • More sources of capital available • Limited Liability • New legal entity

ADVANTAGES More Capital More expertise Share losses Combine assets DISADVANTAGES Share decisions Share profits Unlimited liability Partnership

TYPES OF BUSINESSES - READ pg. 222 • Service – provides service for a fee • Merchandise – business that purchases and sells goods • Retail merchandising business - sells to those who use or consume goods • Wholesale merchandising business – buys and sells merchandise to retail merchandising business • Merchandise: goods a business purchases to sell • To avoid confusion use consistent wording: • Purchased merchandise always means Purchases is debited • Bought supplies supplies account is debited

Omni Import - • Merchandising business organized as partnership • Partners: Michelle Wu and Karl Koehn • What: purchases and sells imported novelty and gift items • Where: Omni rents the building and equipment for operation • Expects to make money and continue indefinitely Going Concern

Special Journal • A journal used to record only one type of transaction. • Why use special journals?? • Separate transactions by category • Separate work load and responsibility • Many daily transactions in business • Special Columns in Journals • They are used when many transactions affect the same account. • They save time in recording and posting.

TYPES OF SPECIAL JOURNALS • Purchases • records all purchases of merchandise on account • Cash Payments • records all cash payments • Sales • records all sales of merchandise on account • For charge customers only • Cash Receipts • records all cash received • General • records all other transactions ***** ALL like transactions go in one journal***

Purchasing Merchandise – New Account • Cost of Merchandise: • The price a business pays for goods it purchases to sell • New classification – 5000 (Expenses move to 6000) • Purchases 5110 • COST ACCOUNT • Temporary account • Markup = Amount added to cost to establish a selling price • Revenue includes both cost and markup • ONLY markup increasescapital and profits • Cost of Merchandise + Markup = Sales (Operating Revenue) • Kept in separate division on chart of accounts see page 219, COST OF MERCHANDISE INCOME STATEMENT ACCOUNT

Cost of Merchandise • ‘Purchased Merchandise’ ALWAYS means that Purchases is DEBITED

Purchases on Account • The purchases account is only used to record items bought for resale not for assets. • Vendor: A business or person from which the company purchases merchandise or assets. • Historical cost: The amount used in the transaction is the price agreed upon at the time of purchase. • Merchandise and other items bought are recorded and reported at the price agreed upon at the time the transactions occur • Purchase on account to be paid later • Some businesses keep separate ledger accounts for each vendor • Lots of vendors create a bulky ledger, so INSTEAD, we summarize the TOTAL amount in Accounts Payable

Accounts Payable • Classification Liability - 2110 • This account summarizes the total amount owed to all vendors in a single account. Accounts Payable Credit Side Normal Balance Side Increase Side Debit Side Decrease Side

Purchases Journal • Special Journal to record ONLY purchases on account NOT FOR CASH • One special amount column where both debit and credit amount are entered. • Saves time in recording entry and in posting. • Vendor’s name must be entered in Account Credited column. • Journals must be totaled, proved, and ruled (end of month and/or page)

PURCHASE INVOICE: Source document for all entries in purchases journal. 1 4 2 3 • Stamp date received and purchase invoice number. • **DO not confuse with Vendor’s date and number 2. Place a check mark by each amount received 3. Initials of person who checked invoice. 4. Review vendor’s terms of sale- agreement between buyer and seller about pymt and time frame

Purchases Accounts Payable PURCHASING MERCHANDISE ON ACCOUNT November 2. Purchased merchandise on account from Crown Ltd., $2,039.99. Purchase Invoice No. 83. 1. Which accounts are affected? Purchases Accounts Payable 2,039.00 2. How is each account classified? Purchases is a cost account. Accounts Payable is a liability account. 3. How is each amount entered in the accounts? Costs increase on the debit side. Liabilities increase on the credit side. 2,039.00

PURCHASING MERCHANDISE ON ACCOUNT 1 2 3 4 1. Write the date. 2. Write the vendor name in the Account credited column. 3. Write the purchase invoice number in the Doc. No. column. 4. Write the amount of the invoice in the special amount column. November 2. Purchased merchandise on account from Crown Ltd., $2,039.00. Purchase Invoice No. 83.

TOTALING AND RULING A PURCHASES JOURNAL 1 5 2 3 6 4 1. Rule a single line across amount column. 2. Write the date. 3. Write word Total. 4. Add the amount column. 5. Write total amount below single line. 6. Rule double lines across amount column. POSTING – CHAPTER 12

Chapter 10-1 • TO DO: • Work Together, pg 228 • On Your Own

Review: • Which of the following should be recorded in the purchases journal??? • Buying supplies on account • Purchasing merchandise for cash • Purchasing merchandise on account • What kinds of transactions are recorded in a purchases journal? • Why are there two account titles in the ‘amount column’ of a purchases journal? • What is the advantage of having special amount columns?

Chapter 10-2: Journalizing Cash Payments using a Cash Payments Journal Special Journals: • Cash payments • Cash receipts • Purchases • Sales Then, for all remaining transactions, use the • General journal

Cash Payments Journal • Special journal to record ONLY CASH PAYMENT transactions • Source document is usually a check stub; but might be a memo (bank service charge). • EVERY entry has a CREDIT to CASH. • General amount columns: for cash payments that do not occur often (Rent Expense payment) • Special columns: Acct Pay DR and Cash CR

Purchases Cash PURCHASING MERCHANDISE FOR CASH November 1. Purchased merchandise for cash, $575.00 Check No. 290. 1. Which accounts are affected? Purchases Cash 575.00 2. How is each account classified? Purchases is a cost account. Cash is an asset account. 3. How is each amount entered in the accounts? Costs increase on the debit side. Assets decrease on the credit side. 575.00 Lesson 10-2, page 230

PURCHASING MERCHANDISE FOR CASH 4 1 2 5 3 November 1. Purchased merchandise for cash, $575.00 Check No. 290. 1. Write the date. 2. Write the account title column. 3. Write the check number. 4. Write the debit amount. 5. Write the credit amount. What happened in Nov. 2 and Nov. 5 transactions???

Supplies—Office Cash BUYING SUPPLIES FOR CASH November 5. Paid cash for office supplies, $34.00. Check No. 292. 1. Which accounts are affected? Supplies—Office Cash Debit Normal Balance 2. How is each account classified? Supplies—Office is an asset account. Cash is an asset account. 34.00 3. How is each classification changed? Assets are increased. Assets are decreased. Debit Normal Balance 4. How is each amount entered in the accounts? Assets increase on the debit side. Assets decrease on the credit side. 34.00 Lesson 10-2, page 230

Cash Payment on Account Nov. 7. Paid cash on account to Pacific Imports, $1050.00, covering Purchase Invoice No. 81. Check No. 294 • Write date • Write vendor name • Write Check No. • Write Debit amount • Write Credit amount

CASH PAYMENT OF AN EXPENSE 1 2 3 4 5 1. Write the date. Nov. 9. Paid cash to advertising, $150.00. Check No. 296 2. Write the account title. 3. Write the check number. 4. Write the debit amount. 5. Write the credit amount. Lesson 10-2, page 232

To Do: Work Together On Your Own Application Problems 10-1, 10-2 Read Chapter 10

REVIEW: • What is recorded in the general amount columns of the cash payments journal? • What is the difference between purchasing merchandise and buying supplies? • When cash is paid on account, what is the effect on the cash account? • ***Remember – Special Journals eliminate the need to write general ledger account titles for each transaction***

Chapter 10-3: Additional Cash Payments Journal Operations • What kinds of transactions might a business typically write checks for? • Pay an expense • Buy supplies • Purchase merchandise • Withdrawal of cash • Establish and Replenish petty cash • Make payment on account

Miscellaneous Expense Advertising Expense Supplies—Office Supplies—Store Cash 92.00 35.00 31.00 47.00 205.00 CASH PAYMENT TO REPLENISH PETTY CASH November 9. Paid cash to replenish the petty cash fund, $205.00: office supplies, $35.00; store supplies, $47.00; advertising, $92.00; miscellaneous, $31.00. Check No. 297. Entered Debit side Debit side Debit side Debit side Credit side Accounts Affected Supplies—Office Supplies—Store Advertising Expense Miscellaneous Expense Cash Classification Asset Asset Expense Expense Asset Lesson 10-3, page 234

CASH PAYMENT TO REPLENISH PETTY CASH 2 5 1 3 4 1. Write the date. 2. Write the titles of accounts for which petty cash was used. 3. Write the check number. 4. Write the debit amounts. 5. Write the credit amount. ***REMEMBER – Petty Cash account is used ONLY when establishing the account***

Michelle Wu, Drawing Cash 1,200.00 1,200.00 CASH WITHDRAWALS BY PARTNERS November 10. Michelle Wu, partner, withdrew cash for personal use, $1,200.00. Check No. 298. Accounts Affected Michelle Wu, Drawing Cash *Must have separate drawing accounts for each partner **Recorded in separate accounts (from capital) to easily determine total amounts for each period

CASH WITHDRAWALS BY PARTNERS 2 1 3 5 4 1. Write the date. 2. Write the account title. 3. Write the check number. 4. Write the debit amount. 5. Write the credit amount. Lesson 10-3, page 235

Prove Cash Payments Journal • Proved at the end of the page and ALWAYS at the end of the month. • Add all columns • Add the totals of all debit columns • Add the totals of all credit columns • The debit total and the credit total must equal. • Draw a double ruling to represent equality of DR and CR.

5 TOTALING, PROVING, AND RULING A CASH PAYMENTS JOURNAL PAGE TO CARRY TOTALS FORWARD 1 2 6 4 3 1. Rule a single line. 2. Write the date. 3. Write Carried Forward. 4. Place check mark in Post. Ref. column. 5. Write each column total. 6. Rule double line. Lesson 10-3, page 236

5 STARTING A NEW CASH PAYMENTS JOURNAL PAGE 1 2 3 4 1. Write the journal page number. 2. Write the date. 3. Write the words Brought Forward. 4. Place check mark in Post. Ref. column. 5. Record column totals brought forward from previous page. Lesson 10-3, page 237

4 TOTALING, PROVING, AND RULING A CASH PAYMENTS JOURNAL AT THE END OF A MONTH 1 5 2 3 1. Rule a single line. 2. Write the date. 3. Write Totals. 4. Write each column total. 5. Rule double line if DR=CR • MUST prove DR = CR Lesson 10-3, page 238

TO DO: • Work Together • On Your Own

Chapter 10-4: Journalizing Other Transactions Using a General Journal • ALL transactions that CANNOT be recorded in a special journal • Supplies purchased on account. • Partner withdrawal of merchandise. • Debit to Drawing account • Credit to Purchases • Correcting Entry • ex) Recorded an entry as a debit to supplies and it should have been purchases.

Buying Supplies on Account • Nov. 6. bought store supplies on account from Foxfire Supply, $210. Memo no. 52. • What accounts are affected? • Supplies - Office and Accounts Payable/vendor • What is the classification of each account? • Asset Supplies/ Accounts Pay/vendor liability • How are they affected? • Supplies + Accounts Payable/vendor + • Do you debit or credit? • Supplies-debit Accounts Payable/vendor-credit

BUYING SUPPLIES ON ACCOUNT 2 4 3 1 7 6 5 • Nov. 6. bought store supplies on account from Foxfire Supply, $210. Memo no. 52. 1. Write the date. 2. Write the account title. 3. Write the memorandum number. 4. Write the debit amount. 5. Write the account title and vendor name. 6. Place diagonal line in Post. Ref. column. 7. Write the credit amount. Lesson 10-4, page 241

Why the diagonal lines???? • The general ledger account - Accounts Payable and the vendor account - Foxfire Supply are affected by this credit part of the entry • Both titles are recorded, separated by a diagonal line • Diagonal line is repeated in Post Ref column to show that single credit amount is posted to 2 accounts (CHAPTER 12)

Withdrawals by Owner • Assets • Cash – Cash payments • Supplies – General • Equipment – General • etc. • Merchandise – General • A withdraw of merchandise affects the PURCHASES account - decrease

Karl Koehn, Drawing Purchases 300.00 300.00 MERCHANDISE WITHDRAWALS BY PARTNERS November 12. Karl Koehn, partner, withdrew merchandise for personal use, $300.00. Memorandum No. 53. Accounts Affected Karl Koehn, Drawing Purchases Lesson 10-4, page 242

MERCHANDISE WITHDRAWALS BY PARTNERS 2 3 1 4 5 6 1. Write the date. 2. Write the account title Karl Koehn, Drawing. 3. Write the memorandum number. 4. Write the debit amount. 5. Write the account title Purchases. 6. Write the credit amount. Lesson 10-4, page 242

REVIEW: WHICH JOURNAL????? • Paying cash on account • Buying supplies on account • Purchasing merchandise on account • Buying supplies for cash • Merchandise withdrawal by partner • Purchasing merchandise for cash

TO DO: • Work Together • On your Own

10-4 Review: • What journal is used to record transactions that cannot be recorded in special journals? • Why is a memo used as the source doc when supplies are bought on account? • Why are 2 account titles written for the credit amount when supplies are bought on account? • When is the equality of DR and CR proved for a general journal? • Why is the cash pymts journal NOT used when a partner withdrawals merchandise for personal use?