Download

1 / 14

140 likes | 289 Views

Understand Your Credit Report and Credit Score. Make the Most and Minimize the Mess. Your credit history can affect many parts of your life. Lenders, potential employers, and landlords — just to name a few — can all legally access your credit history, and often do.

E N D

Understand Your Credit Report and Credit Score Make the Most and Minimize the Mess

Your credit history can affect many parts of your life. Lenders, potential employers, and landlords — just to name a few — can all legally access your credit history, and often do. • To determine how good a credit risk you are, lenders often buy both a credit report and a credit score from the three major credit reporting agencies: Equifax, Experian, and TransUnion.

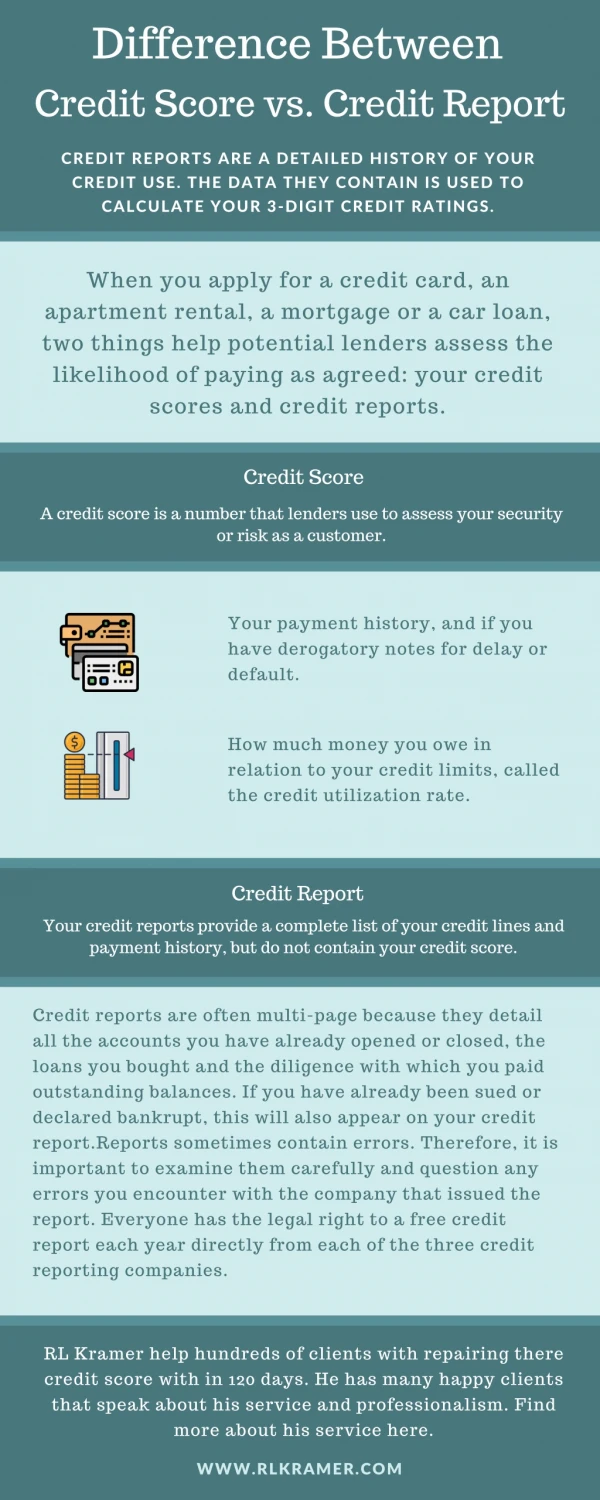

What’s in your credit report Your credit report is a detailed list of your credit history. Part of what it includes is: • The type of credit you have (credit card, auto loan, mortgage, etc.) • Your credit limit or original loan amount • Your account balance (or the total balance of your last statement) • Your payment history (late payments stay on your credit report for seven years) • Bankruptcies (stays on your credit report for 10 years) • Identifying information such as your name, date of birth, and employment history is listed on your credit report, but is not used to determine your credit score.

How to check your credit report • You should review your credit report at least once a year to check for errors or fraud, and also before making a big purchase like a house or a car. • Residents of most states can get one free credit report from each of the three credit reporting agencies once a year through www.annualcreditreport.com. • To get credits reports more often than once a year, you can order your credit report for a small fee.

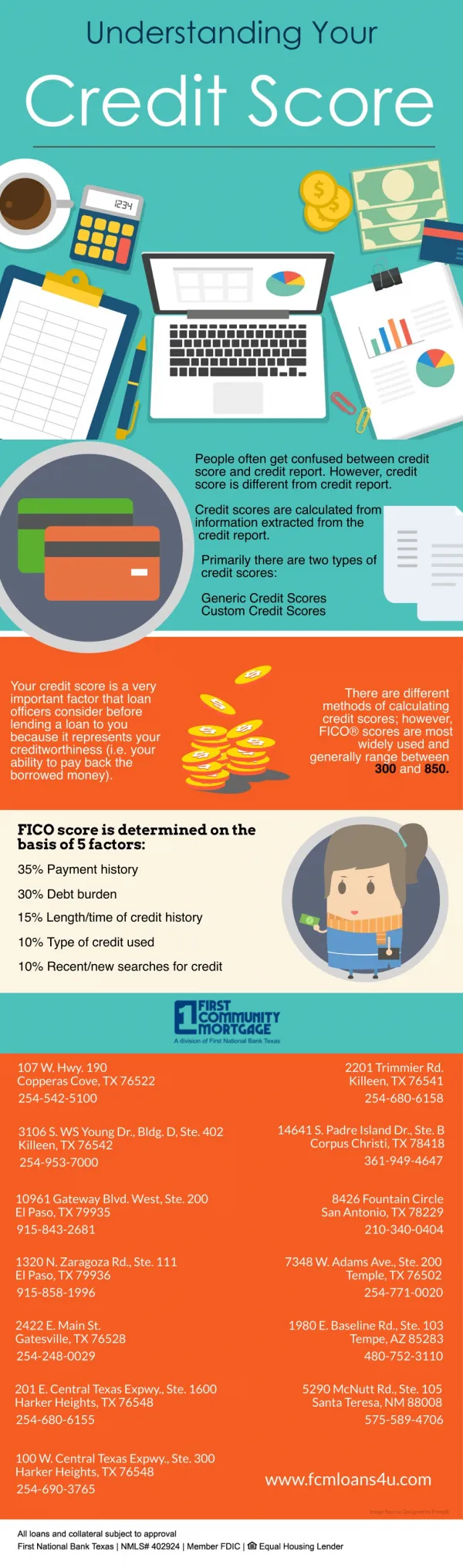

Credit scoresA credit score — also known as a credit rating — is a numeric value based on the information contained in your credit report. That score (usually between 300 and 850) tells the lender the level of future risk associated with your credit history. The higher the score, the lower the risk. • Credit bureau scores are often called "FICO scores" because many credit bureau scores used in the U.S. are produced from software developed by Fair Isaac Corporation (FICO). • While many lenders use credit scores to help them make their lending decisions, each lender has its own criteria. There is no single minimum credit "cutoff score" used by all lenders, and there are many additional factors that lenders use to determine your actual interest rates.

Tips for Raising your Credit Score Raising your credit score is a bit like losing weight — it takes time and there is no quick fix. In fact, quick-fix efforts can backfire. The best advice is to manage credit responsibly over time. Follow these suggestions from Fair Isaac Corporation, the creators of the FICO® score. • Improve your payment history • Pay your bills on time. Delinquent payments and collections can have a major negative impact on your score. • If you have missed payments, get current and stay current. The longer you pay your bills on time, the better your score. But also be aware even if you pay off a collection account, it will stay on your report for seven years. • Contact your creditors or a legitimate credit counselor if you're having trouble making ends meet. This won't improve your score immediately, but if you can begin to manage your credit and pay on time, your score will get better over time. • Lower your amounts owed • Keep your balances low on credit cards and other "revolving credit." High outstanding debt can affect a score. • Pay off debt rather than moving it around. The most effective way to improve your score is by paying down your revolving credit. • Don't close unused credit cards as a short-term strategy to raise your score. Owing the same amount but having fewer open accounts may lower your score. • Don't open new credit cards you don't need, just to increase your available credit. This approach could backfire and lower your score.

Tips for Raising your Credit Score (cont.) • Make the most of the length of your credit historyIf you've been managing credit for a short time, don't open a lot of new accounts too rapidly. New accounts will lower your average account age, which will have a larger effect on your score if you don't have a lot of other credit information. Also, rapid account buildup can look risky if you are a new credit user. • Getting new credit • Do your rate shopping within a focused period of time. FICO scores distinguish between a search for a single loan and a search for many new credit lines, in part by the length of time over which inquiries occur. • Re-establish your credit history. Even if you'd had problems in the past, opening new accounts responsibly and paying them off on time will raise your score in the long term. • Manage the types of credit you have • Apply for and open new credit accounts only as needed. Don't open accounts just to have a better credit mix — it probably won't raise your score. • Have credit cards — but manage them responsibly. In general, having credit cards (and paying them on time) will raise your score.

Factors That Affect Your Score • Many lenders use a FICO® score — a numeric calculation of your credit report calculated by Fair Isaac Corporation — to obtain a fast, objective measure of your credit risk. By understanding the factors that can help or hurt your score, you'll have a better understanding of how lenders view you as a credit risk — and how you can improve your score. Here are the five factors that determine your FICO score. The levels of importance shown here are for the general population, and will be different for each individual: • 1. Your payment history: what is your track record? (approximately 35% of your score)The most significant impact on your score is whether you have paid past accounts in a timely manner (on or before the date the payment was due). However, an overall good credit profile can outweigh a few late payments, and late payments have less impact over time. • 2. Amounts that you owe: how much is too much? (30%)Part of the science of credit scoring is determining how much debt is too much: • In some cases, having a very small balance without missing payments shows you've managed credit responsibly, and may be slightly better than having no balance at all. • While you don't want to have too many accounts open, it's good to have more than one, so that you're not using too much of one account's available credit limit. • Owing a lot of money on numerous accounts suggests to lenders that you may be overextended and more likely to make late payments — or make no payments at all.

Factors That Affect Your Score (cont.) • 3. Length of your credit history: how established is it? (15%)In general, a more seasoned credit history will increase your FICO score. Lenders want to see that you can responsibly manage your credit accounts over time. However, even those people who have not used credit for an extended period of time may get high scores, depending on how the other information in their credit report appears. • 4. New credit: are you taking on more debt? (10%)Opening several credit accounts in a short period of time can represent a greater risk, especially for those with newer credit histories. According to Fair Isaac Corporation, FICO scores try to distinguish between an attempt to obtain many new credit accounts and an attempt to obtain the best interest rate. FICO scores generally do not associate higher risk with shopping for the best interest rate. • 5. Types of credit in use: is it a "healthy" mix? (10%)Your FICO score will reflect your mix of credit cards, retail accounts, installment loans, finance company accounts and mortgage loans, etc. While a healthy mix will improve your score, it's not necessary to have one of each, and it's not a good idea to open accounts you don't intend to use. • What does not affect your scoreLenders look at many things when making a credit decision, including your income, employment history, and the kind of credit you're requesting. But none of those factors are included in your FICO score. And neither the lender nor your score considers your race, religion, sex, marital status, age, or if you receive public assistance. • FICO scores also ignore self-inquiries, so checking your own credit report will not lower your credit score. In fact, it's a good idea to check your credit report once a year to make sure there are no mistakes.

Interpreting Your Score A credit score, a numeric summary of your credit history, generally ranges between 300 and 850. But what does the number mean to you? • What's a good score?There is no single "cutoff" score used by all lenders, and there are many additional factors besides your credit score that lenders use to determine whether to give you credit and at what interest rate. So it's hard to say what a good score is outside of a particular lending situation. For example, one auto lender may offer lower interest rates to people with scores above, say, 680; another lender may use 720, and so on. How others scoreAccording to Fair Isaac Corporation (FICO), this is how FICO® scores are typically spread among the population:

Why your score isn't higherWhen a lender receives your FICO score, up to four "score reason codes" are also delivered. If the lender rejects your request for credit, and your FICO score was part of the reason, these score reasons can help the lender tell you why your score wasn't higher. • These score reasons are more useful than the score itself in helping you determine whether your credit report might contain errors, and how you might improve your score over time. However, if you already have a high score (for example, in the mid-700s or higher) some of the reasons may not be very helpful, as they may be marginal factors related to length of credit history, new credit, and types of credit in use. • Top ten score reasonsThese are the top 10 most frequently given score reasons. Note that the specific wording given by your lender may be different from this. • Serious delinquency. • Serious delinquency, and public record or collection filed. • Derogatory public record or collection filed. • Time since delinquency is too recent or unknown. • Level of delinquency on accounts. • Number of accounts with delinquency. • Amount owed on accounts. • Proportion of balances to credit limits on revolving accounts is too high. • Length of time accounts have been established. • Too many accounts with balances.

Top Misconceptions About Scores Credit scores can be confusing. Empower yourself by ordering your FICO score and understanding how scoring works. Make sure you know the truth about these popular misconceptions: • My score determines whether or not I get credit.Lenders use a number of facts to make credit decisions, including your credit score. Lenders look at information such as the amount of debt you can reasonably handle given your income, your employment history, and your credit history. Based on their analysis of this information under specific underwriting policies, lenders may extend or decline credit to you regardless of your score. • A poor score will haunt me forever.Just the opposite is true. Since a credit score is a mathematical calculation, it changes as new information is added to your credit history. Scores change gradually as you change the way you handle credit. For example, past credit problems impact your score less as time passes. • Lenders request a new current score when you submit a credit application, so they have the most recent information available. So by taking the time to improve your score, you might qualify for more favorable interest rates and other credit terms. • My score will drop if I apply for new credit.If it does, it probably won't drop much. If you apply for several credit cards within a short period of time, multiple requests for your credit report (called "inquiries") will appear on your report. Your score may drop if you open numerous accounts from different types of lenders within a short period of time. But most credit scores are not affected by rate shopping, when multiple inquiries from different lenders are made within a short period of time.

Top Misconceptions About Scores(cont) • My score will drop if I check my credit report.Self-inquiries do not affect your score, as long as you order your credit report directly from the credit reporting agencies, or through an organization authorized to provide credit reports to consumers. It's a good idea to check your credit report once a year. • People with high incomes have high credit scores.Income might affect your ability to get a loan, but it does not affect your credit score. Only your credit history — such as timely payments and how much you owe — affects your score. Regardless of income, if you manage your debt responsibly, you can have a high score. • Credit scoring is unfair to minorities.Scoring considers only credit-related information. Factors like gender, race, nationality, and marital status are not included. In fact, the Equal Credit Opportunity Act (ECOA) prohibits lenders from considering this type of information when issuing credit. Because the credit score is mathematically calculated, it treats all borrowers the same. • Credit scoring infringes on my privacy.Credit scoring evaluates the same information lenders already review — the credit bureau report. A score is simply a numerical calculation based on the information contained in your credit report.