Download

1 / 34

350 likes | 519 Views

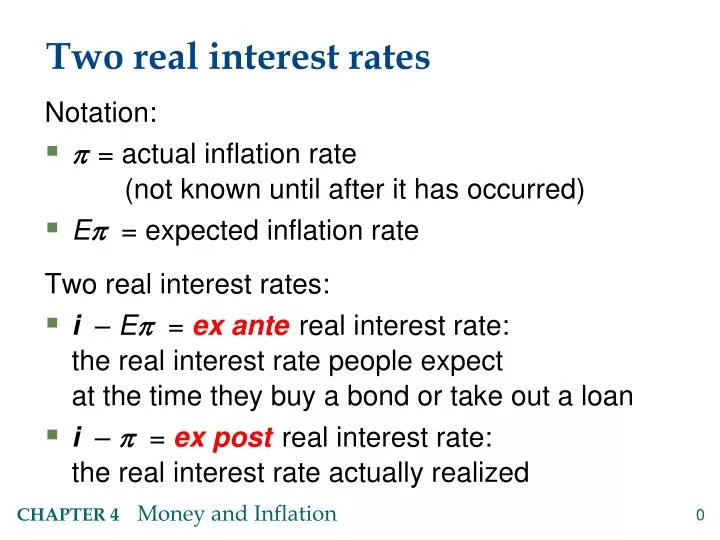

Two real interest rates. Notation: = actual inflation rate (not known until after it has occurred) E = expected inflation rate Two real interest rates: i – E = ex ante real interest rate: the real interest rate people expect at the time they buy a bond or take out a loan

E N D

Two real interest rates Notation: • = actual inflation rate (not known until after it has occurred) • E = expected inflation rate Two real interest rates: • i – E = ex ante real interest rate: the real interest rate people expect at the time they buy a bond or take out a loan • i – = ex postreal interest rate:the real interest rate actually realized

Money demand and the interest rate • In the Quantity Theory of Money, the demand for real money balances depends only on real income Y. • Another determinant of money demand: the nominal interest rate, i. • the opportunity cost of holding money (instead of bonds or other interest-earning assets). • Hence, i in money demand.

(M/P)d = real money demand, depends negatively on i i is the opp. cost of holding money positively on Y higher Y more spending so, need more money (“L” is used for the money demand function because money is the most liquid asset.) The money demand function

When people are deciding whether to hold money or bonds, they don’t know what inflation will turn out to be. Hence, the nominal interest rate relevant for money demand is r + E. The money demand function

The supply of real money balances Real money demand Equilibrium

variable how determined (in the long run) M exogenous (the Fed) r adjusts to ensure S = I Y P adjusts to ensure ~ What determines what ~

How P responds to M • For given values of r, Y, and E, a change in Mcauses P to change by the same percentage – just like in the quantity theory of money.

What about expected inflation? • Over the long run, people don’t consistently over- or under-forecast inflation, so E = on average. • In the short run, E may change when people get new information. • EX: Fed announces it will increase Mnext year. People will expect next year’s P to be higher, so E rises. • This affects Pnow, even though M hasn’t changed yet….

How P responds to E • For given values of r, Y, and M ,

NOW YOU TRY:Discussion Question Why is inflation bad? • What costs does inflation impose on society? List all the ones you can think of. • Focus on the long run. • Think like an economist.

A common misperception • Common misperception: inflation reduces real wages • This is true only in the short run, when nominal wages are fixed by contracts. • (Chap. 3) In the long run, the real wage is determined by labor supply and the marginal product of labor, not P or . • Consider the data…

The CPI and Average Hourly Earnings, 1965-2009 900 $20 800 Real average hourly earnings in 2009 dollars, right scale 700 $15 600 500 1965 = 100 Hourly wage in May 2009 dollars $10 400 Nominal average hourly earnings, (1965 = 100) 300 $5 200 CPI (1965 = 100) 100 0 $0 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010

The classical view of inflation • The classical view: A change in the price level is merely a change in the units of measurement. Then, why is inflation a social problem?

The social costs of inflation …fall into two categories: 1. costs when inflation is expected 2. costs when inflation is different than people had expected

The costs of expected inflation: 1. Shoeleather cost • def: the costs and inconveniences of reducing money balances to avoid the inflation tax. • i real money balances • Remember: In long run, inflation does not affect real income or real spending. • So, same monthly spending but lower average money holdings means more frequent trips to the bank to withdraw smaller amounts of cash.

The costs of expected inflation: 2. Menu costs • def: The costs of changing prices. • Examples: • cost of printing new menus • cost of printing & mailing new catalogs • The higher is inflation, the more frequently firms must change their prices and incur these costs.

The costs of expected inflation: 3. Relative price distortions • Firms facing menu costs change prices infrequently. • Example: A firm issues new catalog each January. As the general price level rises throughout the year, the firm’s relative price will fall. • Different firms change their prices at different times, leading to relative price distortions… …causing microeconomic inefficiencies in the allocation of resources.

The costs of expected inflation: 4. Unfair tax treatment Some taxes are not adjusted to account for inflation, such as the capital gains tax. Example: • Jan 1: you buy $10,000 worth of IBM stock. • Dec 31: you sell the stock for $11,000, so your nominal capital gain is $1000 (10%). • Suppose = 10% during the year. Your real capital gain is $0. • But the govt makes you pay taxes on your $1000 nominal gain!!

The costs of expected inflation: 5. General inconvenience • Inflation makes it harder to compare nominal values from different time periods. • This complicates long-range financial planning.

Additional cost of unexpected inflation: Arbitrary redistribution of purchasing power • Many long-term contracts not indexed, but based on E. • If turns out different from E, then some gain at others’ expense. Example: borrowers & lenders • If > E, then (i ) < (iE) and purchasing power is transferred from lenders to borrowers. • If < E, then purchasing power is transferred from borrowers to lenders.

Additional cost of high inflation: Increased uncertainty • When inflation is high, it’s more variable and unpredictable: turns out different from Emore often, and the differences tend to be larger (though not systematically positive or negative) • Arbitrary redistributions of wealth become more likely. • This creates higher uncertainty, making risk averse people worse off.

One benefit of inflation • Nominal wages are rarely reduced, even when the equilibrium real wage falls. This hinders labor market clearing. • Inflation allows the real wages to reach equilibrium levels without nominal wage cuts. • Therefore, moderate inflation improves the functioning of labor markets.

Hyperinflation • Common definition: 50% per month • All the costs of moderate inflation described above become HUGEunder hyperinflation. • Money ceases to function as a store of value, and may not serve its other functions (unit of account, medium of exchange). • People may conduct transactions with barter or a stable foreign currency.

What causes hyperinflation? • Hyperinflation is caused by excessive money supply growth: • When the central bank prints money, the price level rises. • If it prints money rapidly enough, the result is hyperinflation.

Why governments create hyperinflation • When a government cannot raise taxes or sell bonds, it must finance spending increases by printing money. • In theory, the solution to hyperinflation is simple: stop printing money. • In the real world, this requires drastic and painful fiscal restraint.

The Classical Dichotomy Nominal variables: Measured in money units, e.g., • nominal wage: Dollars per hour of work. • nominal interest rate: Dollars earned in future by lending one dollar today. • the price level: The amount of dollars needed to buy a representative basket of goods.

Real variables:Measured in physical units – quantities and relative prices, for example: • quantity of output produced • real wage: output earned per hour of work • real interest rate: output earned in the future by lending one unit of output today

The Classical Dichotomy • Note: Real variables were explained in Chap 3, nominal ones in Chapter 4. • Classical dichotomy: the theoretical separation of real and nominal variables in the classical model, which implies nominal variables do not affect real variables. • Neutrality of money: Changes in the money supply do not affect real variables. In the real world, money is approximately neutral in the long run.

CHAPTER SUMMARY Money • def: the stock of assets used for transactions • functions: medium of exchange, store of value, unit of account • types: commodity money (has intrinsic value), fiat money (no intrinsic value) • money supply controlled by central bank Quantity theory of money assumes velocity is stable, concludes that the money growth rate determines the inflation rate.

CHAPTER SUMMARY Nominal interest rate • equals real interest rate + inflation rate • the opp. cost of holding money • Fisher effect: Nominal interest rate moves one-for-one w/ expected inflation. Money demand • depends only on income in the Quantity Theory • also depends on the nominal interest rate • if so, then changes in expected inflation affect the current price level

CHAPTER SUMMARY Costs of inflation • Expected inflationshoeleather costs, menu costs, tax & relative price distortions, inconvenience of correcting figures for inflation • Unexpected inflationall of the above plus arbitrary redistributions of wealth between debtors and creditors

CHAPTER SUMMARY Hyperinflation • caused by rapid money supply growth when money printed to finance govt budget deficits • stopping it requires fiscal reforms to eliminate govt’s need for printing money

CHAPTER SUMMARY Classical dichotomy • In classical theory, money is neutral—does not affect real variables. • So, we can study how real variables are determined w/o reference to nominal ones. • Then, money market eq’m determines price level and all nominal variables. • Most economists believe the economy works this way in the long run.