Download

1 / 14

140 likes | 246 Views

The Long Slump. By Robert Hall 2011. Slumps. Negative interest rate preserves full employment. Three Adverse forces the gripped the Economy in the aftermath. 1.The overhang of housing and consumer durables resulting from the building and buying frenzy of the decade of the 2000’s

E N D

The Long Slump By Robert Hall 2011

Three Adverse forces the gripped the Economy in the aftermath 1.The overhang of housing and consumer durables resulting from the building and buying frenzy of the decade of the 2000’s 2. High consumer commitments to debt service 3. financial frictions from the crisis (These adverse forces were so destructive because the economy was unable to lower its interest rate to stimulate other kinds of spending to replace house construction and other affected components of spending)

The overhang of housing and consumer durables • Housing bubble in the 2000’s • 14% more housing and durables in relation to GDP than normal going into the crisis • Thought that everything will return to trend (Thus the overhang of housing and consumer durables pointed toward lower future spending in these categories, no matter what happened to the economy)

Illiquid Households and Debt-Service Commitments • US consumers tend to borrow as much as they can and hold almost no liquid assets • To protect themselves when there is a loss of income they borrow against or sell houses and cars, liquidate retirement accounts, and look for help from family and friends • Households new borrowings are not enough to pay for interest payments on older debt.

Financial Frictions • Financial frictions drive wedges between the returns that savers receive and the rates that borrowers pay. • Adverse selection- asymmetric information- worsened by loss of equity among household borrowers. • Agency problems- Worsened by large declines in equity values of financial intermediaries.

Credit Rationing and Lending Standards • Adverse selection becomes a more serious danger when more borrowers are close to the margin of failure. • Lending decreased as a result of the higher lending standard making loans much harder to get for households and businesses

Nominal Interest Rate Pinned at Zero • Currency is a safe asset paying zero return. Currency becomes financially attractive if other safe assets pay negative returns. • Consequently, as long as the Fed will give currency in exchange for reserves dollar for dollar, the interest rate cannot be negative. Because the owner of the bond would sell it, and earn the safer return and bond prices would fall so that their returns rose to zero.

How a Pinned Interest Rate Causes a Slump • By having a pinned Interest rate people will hold on to currency which is returning a higher return then the interest rate so that they can invest in productive capital and consume more in the second period. • To consume more in the second period means to spend less in the current which leads to a slump.

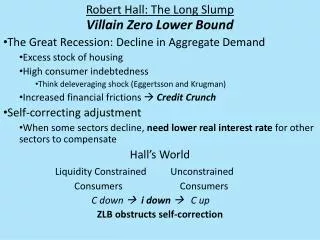

Conclusions of the Model • An economy with a pinned interest rate is subject to extreme sensitivity- little room to maneuver • The same economy without a lower limit on the real rate is completely stable and always operates at full employment. • REAL INTEREST RATES ARE TOO HIGH- conclusion corresponds with Romer’s account of the Great Depression

Unemployment starts at a very high rate above 30 percent and gradually declines during the four years that the interest rate is blocked from declining below 0.12 percent. Once the economy is free of the limit on the interest rate, the unemployment rate drops immediately to its normal 5.5 percent.

For four years the interest rate is pinned at 0.12 percent. At the end of the period of high interest, the rate drops discontinuously to −0.20 percent. That is enough, at that time, to restore full employment. The rate then gradually rises as the adverse forces dissipate.

Conclusion • “An economy with a disabled real interest rate is in deep trouble when one type of Spending” (Homebuilding) • Slump will last until affected spending returns to normal levels • If deflation occurs the slump will worsen as the real interest rate rises • AS OF TODAY THERE HAS BEEN NO DEFLATION