Download

1 / 1

10 likes | 76 Views

Abstract

E N D

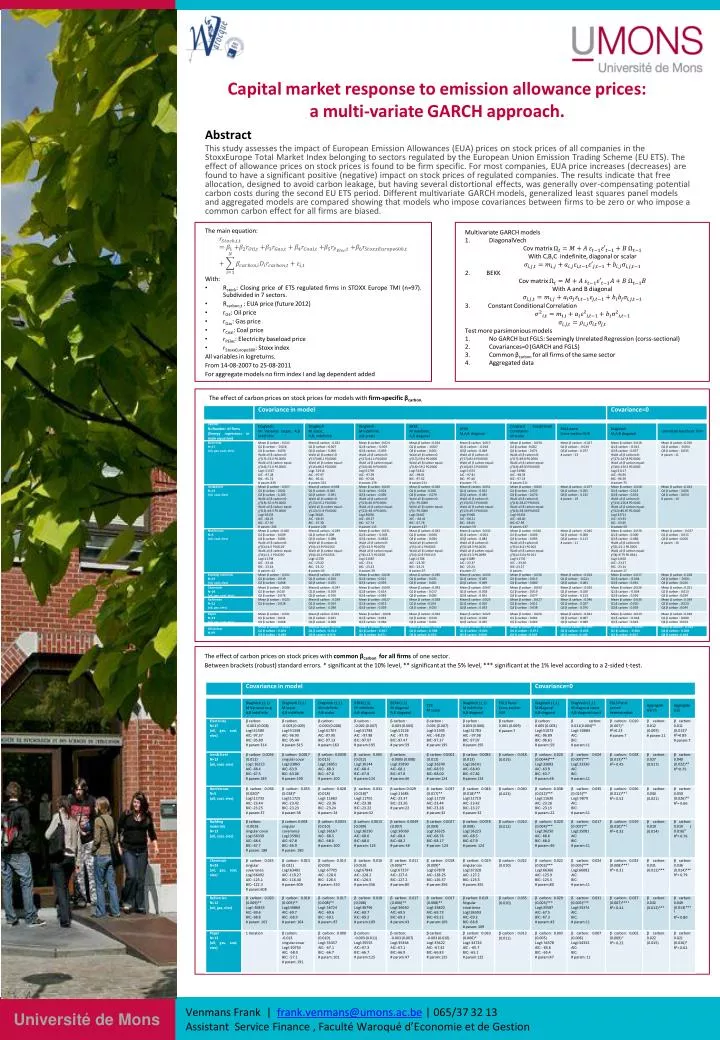

Abstract • This study assesses the impact of European Emission Allowances (EUA) prices on stock prices of all companies in the StoxxEurope Total Market Index belonging to sectors regulated by the European Union Emission Trading Scheme (EU ETS). The effect of allowance prices on stock prices is found to be firm specific. For most companies, EUA price increases (decreases) are found to have a significant positive (negative) impact on stock prices of regulated companies. The results indicate that free allocation, designed to avoid carbon leakage, but having several distortional effects, was generally over-compensating potential carbon costs during the second EU ETS period. Different multivariate GARCH models, generalized least squares panel models and aggregated models are compared showing that models who impose covariances between firms to be zero or who impose a common carbon effect for all firms are biased. Capital market response to emission allowance prices: a multi-variate GARCH approach. The main equation: With: Rstock: Closing price of ETS regulated firms in STOXX Europe TMI (n=97). Subdivided in 7 sectors. Rcarbon,t: EUA price (future 2012) rOil: Oil price rGas: Gas price rCoal: Coal price rPElec: Electricity baseload price rStoxxEurope600: Stoxx index All variables in logreturns. From 14-08-2007 to 25-08-2011 For aggregate models no firm index I and lag dependent added • Multivariate GARCH models • DiagonalVech Cov matrix • With C,B,C indefinite, diagonal or scalar • 2. BEKK • Cov matrix • With A and B diagonal • 3. Constant Conditional Correlation • Test more parsimonious models • No GARCH but FGLS: Seemingly Unrelated Regression (corss-sectional) • Covariances=0 (GARCH and FGLS) • Common βcarbonfor all firms of the samesector • Aggregated data • The effect of carbon prices on stock prices for models with firm-specific βcarbon. • The effect of carbon prices on stock prices with common βcarbon for all firmsof one sector. • Between brackets (robust) standard errors. * significant at the 10% level, ** significant at the 5% level, *** significant at the 1% level according to a 2-sided t-test. Venmans Frank | frank.venmans@umons.ac.be | 065/37 32 13 Assistant Service Finance , Faculté Waroquéd’Economie et de Gestion