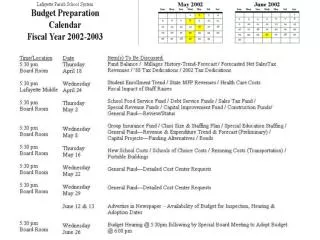

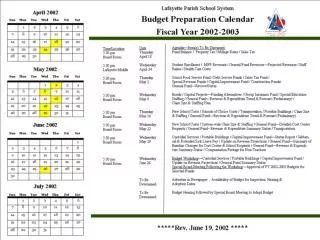

Download

1 / 23

230 likes | 425 Views

Budget Preparation. Bonnie Jackson Supervisory Grants Management Specialist Eunice Kennedy Shriver National Institute of Child Health and Human Development (NICHD). Overview. Budget Considerations Budget Section in Funding Opportunity Announcements Direct Costs

E N D

Budget Preparation Bonnie Jackson Supervisory Grants Management Specialist Eunice Kennedy Shriver National Institute of Child Health and Human Development (NICHD)

Overview • Budget Considerations • Budget Section in Funding Opportunity Announcements • Direct Costs • Facilities and Administrative (F&A) Costs • Budget Components

Budget Considerations • Process for preparing a budget: • How much can be requested? • How do we request it? • F&A costs? • Any restrictions on what can be requested? • What application should be used? • How it will be submitted? • What format?

Funding Opportunity Announcement (FOA) • Includes information about what types of institutions are eligible to apply • Includes information about allowable budget for applications • Foreign applicant organizations should consult Section III of the FOA to ensure eligibility

Allowable Costs • Allowable Costs: Costs incurred by a recipient that are: • Reasonable for the performance of the award; • Allocable; • In conformance with any limitations or exclusions set forth in the federal cost principles applicable to the organization incurring the cost or in the Notice of Award (NoA) as to the type or amount of cost; • Consistent with regulations, policies, and procedures of the recipient that are applied uniformly to both federally supported and other activities of the organization;

Allowable Costs (cont.) • Allowable Costs: • Accorded consistent treatment as a direct or indirect cost; • Determined in accordance with generally accepted accounting principles; and • Not included as a cost in any other federally supported award (unless specifically authorized by statute). For additional information on each, see Cost Considerations—The Cost Principles.

Budget Resource OER Grants (home page): http://grants.nih.gov/grants/oer.htm

Foreign Grant Budgets • All requests for funds and financial reports must be stated in U.S. dollars. • Once an award is made, NIH will not compensate foreign grantees for currency exchange fluctuations through the issuance of supplemental awards • All communication with NIH must be in English.

Foreign Grant Budgets: Cost Principles • Cost principles define what can and cannot be requested in a grant budget. The applicable cost principles depend on the type of applicant organization (educational institution, hospital, government, business), which can be found here: http://grants.nih.gov/grants/compliance/compliance.htm • General information about Cost Considerations may be found at: http://grants.nih.gov/grants/policy/nihgps_2011/nihgps_ch7.htm#cost_considerations.

Foreign Grant Budgets: Allowable Costs • Allowable and Unallowable Costs. Costs that are generally allowable under grants to domestic organizations also are allowable under foreign grants, with the following exceptions: • Major Alterations & Renovations (>$500,000). Unallowable under foreign grants and domestic grants with foreign components. • Minor Alterations & Renovations (≤$500,000). Generally allowable on grants made to foreign organizations or to the foreign component of a domestic grant, unless prohibited by the governing statute or implementing program regulations.

Foreign Grant Budgets: Allowable Costs (cont.) • Allowable and Unallowable Costs • Customs and Import Duties. Unallowable under foreign grants and domestic grants with foreign components. This includes consular fees, customs surtax, value-added taxes, and other related charges. • Patient Care Costs. Patient care costs are provided only in exceptional circumstances.

Direct Costs • Direct Costs: Any costs that can be specifically identified with a particular project, program, or activity or that can be directly assigned to such activities relatively easily and with a high degree of accuracy. • Direct costs include, but are not limited to: • Salaries • Travel • Equipment • Supplies • All directly benefiting the grant-supported project or activity

Indirect/F&A Costs • Indirect/F&A Costs. Costs that most organizations incur for common or joint objectives that cannot be readily identified with an individual project, program, or organizational activity. • Facilities operation and maintenance costs, depreciation, and administrative expenses are examples of costs that usually are treated as F&A costs. • The organization is responsible for presenting costs consistently and must not include costs associated with its F&A rate as direct costs.

Indirect/F&A Costs (cont.) • Grants to foreign institutions and international organizations • With the exception of the American University of Beirut and the World Health Organization, foreign and international organizations will be funded at a rate of 8 percentof modified total direct costs, exclusive of expenditures for equipment.

Budget Components • Personnel: • Name • Role on project • Appointment type • Months devoted to project • Salary requested • Fringe benefits • Totals

Budget Components (cont.) • Consultant costs • Equipment • Supplies • Travel • Other costs • Direct costs total • Budget narrative: The justification of how and/or why a line item helps to meet the program objectives. • Explains how the costs were estimated • Justifies the need for the cost