Download

1 / 1

1.17k likes | 3.15k Views

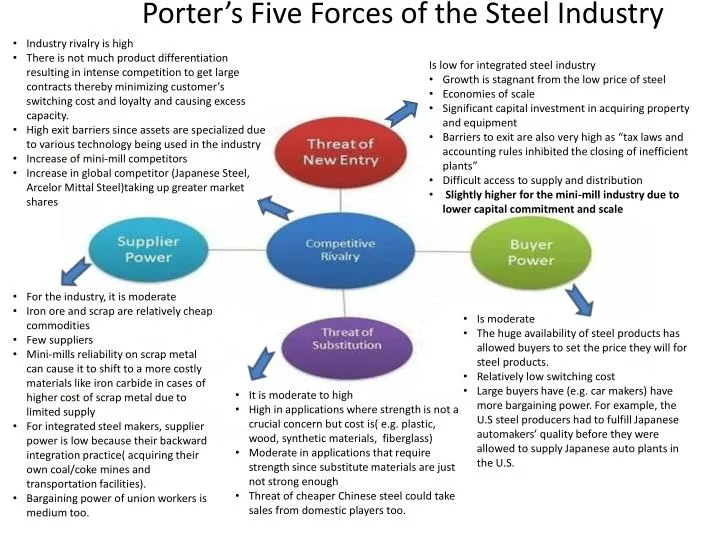

Porter’s Five Forces of the S teel Industry. Industry rivalry is high There is not much product differentiation resulting in intense competition to get large contracts thereby minimizing customer’s switching cost and loyalty and causing excess capacity.

E N D

Porter’s Five Forces of the Steel Industry • Industry rivalry is high • There is not much product differentiation resulting in intense competition to get large contracts thereby minimizing customer’s switching cost and loyalty and causing excess capacity. • High exit barriers since assets are specialized due to various technology being used in the industry • Increase of mini-mill competitors • Increase in global competitor (Japanese Steel, Arcelor Mittal Steel)taking up greater market shares • Is low for integrated steel industry • Growth is stagnant from the low price of steel • Economies of scale • Significant capital investment in acquiring property and equipment • Barriers to exit are also very high as “tax laws and accounting rules inhibited the closing of inefficient plants” • Difficult access to supply and distribution • Slightly higher for the mini-mill industry due to lower capital commitment and scale • For the industry, it is moderate • Iron ore and scrap are relatively cheap commodities • Few suppliers • Mini-mills reliability on scrap metal can cause it to shift to a more costly materials like iron carbide in cases of higher cost of scrap metal due to limited supply • For integrated steel makers, supplier power is low because their backward integration practice( acquiring their own coal/coke mines and transportation facilities). • Bargaining power of union workers is medium too. • Is moderate • The huge availability of steel products has allowed buyers to set the price they will for steel products. • Relatively low switching cost • Large buyers have (e.g. car makers) have more bargaining power. For example, the U.S steel producers had to fulfill Japanese automakers’ quality before they were allowed to supply Japanese auto plants in the U.S. • It is moderate to high • High in applications where strength is not a crucial concern but cost is( e.g. plastic, wood, synthetic materials, fiberglass) • Moderate in applications that require strength since substitute materials are just not strong enough • Threat of cheaper Chinese steel could take sales from domestic players too.