Download

1 / 4

50 likes | 58 Views

"The new provision of Section 194R of the Income Tax Act, 1961 introduced through Finance Act 2022 comes into effect from 01 July 2022, there has already been a"<br>TaxGuru is a platform that provides Updates On Amendments in Income Tax, Wealth Tax, Company Law, Service Tax, RBI, Custom Duty, Corporate Lawu00a0, Goods and Service Tax etc.<br>To know more visit https://taxguru.in/income-tax/implications-arising-section-194r-income-tax-act.html

E N D

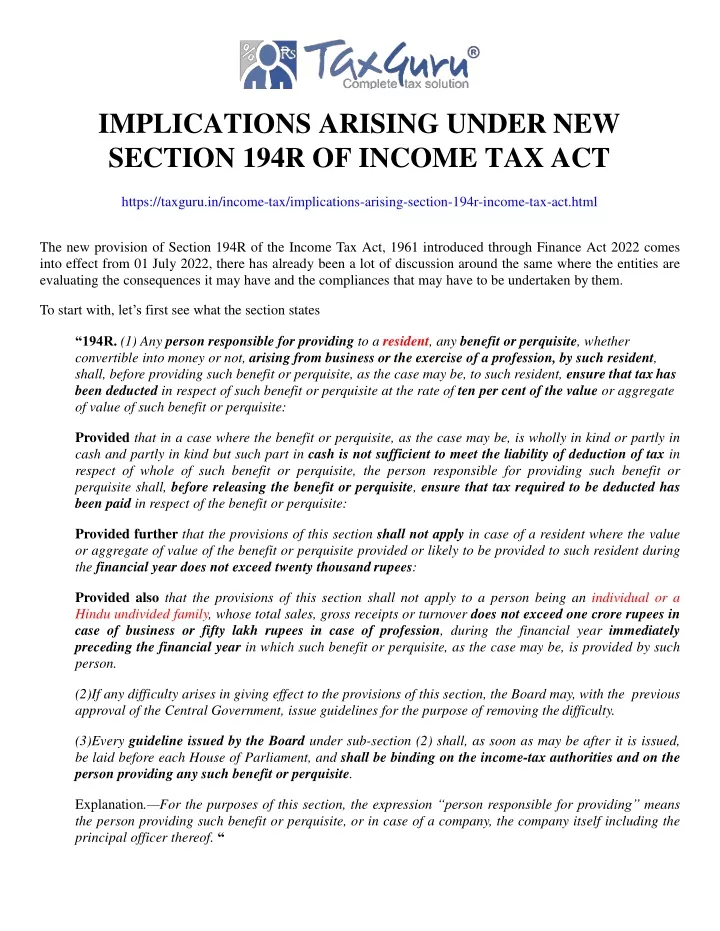

IMPLICATIONS ARISING UNDERNEW SECTION 194R OF INCOME TAXACT https://taxguru.in/income-tax/implications-arising-section-194r-income-tax-act.html The new provision of Section 194R of the Income Tax Act, 1961 introduced through Finance Act 2022 comes into effect from 01 July 2022, there has already been a lot of discussion around the same where the entities are evaluating the consequences it may have and the compliances that may have to be undertaken bythem. To start with, let’s first see what the sectionstates “194R. (1) Any person responsible for providing to a resident, any benefit or perquisite, whether convertible into money or not, arising from business or the exercise of a profession, by such resident, shall, before providing such benefit or perquisite, as the case may be, to such resident, ensure that taxhas been deducted in respect of such benefit or perquisite at the rate of ten per cent of the value or aggregate of value of such benefit orperquisite: Provided that in a case where the benefit or perquisite, as the case may be, is wholly in kind or partly in cash and partly in kind but such part in cash is not sufficient to meet the liability of deduction of tax in respect of whole of such benefit or perquisite, the person responsible for providing such benefit or perquisite shall, before releasing the benefit or perquisite, ensure that tax required to be deducted has been paid in respect of the benefit orperquisite: Provided further that the provisions of this section shall not apply in case of a resident where the value or aggregate of value of the benefit or perquisite provided or likely to be provided to such resident during the financial year does not exceed twenty thousandrupees: Provided also that the provisions of this section shall not apply to a person being an individual or a Hindu undivided family, whose total sales, gross receipts or turnover does not exceed one crore rupees in case of business or fifty lakh rupees in case of profession, during the financial year immediately preceding the financial year in which such benefit or perquisite, as the case may be, is provided by such person. If any difficulty arises in giving effect to the provisions of this section, the Board may, with the previous approval of the Central Government, issue guidelines for the purpose of removing thedifficulty. Every guideline issued by the Board under sub-section (2) shall, as soon as may be after it is issued, be laid before each House of Parliament, and shall be binding on the income-tax authorities and on the person providing any such benefit orperquisite. Explanation.—For the purposes of this section, the expression “person responsible for providing” means the person providing such benefit or perquisite, or in case of a company, the company itself including the principal officer thereof.“

Now while going through the provision it has been clearly provided that any benefit or perquisite provided to person/ entity carrying on business or profession shall be subject to TDS irrespective of the taxation of the same. To clarify the issues that may be arising from the above provision CBDT issued Circular no 12 of 2022 dated 16 June 2022 which we shall discuss later in the sectionbelow. • Applicability • First let us understand the applicability of the provision and for that the same has been broken down into 2 conditions that needs to bemet: • Benefit or perquisite shall be paid toRESIDENT • Person receiving the benefit/perquisite is carrying on BUSINESS ORPROFESSION • Exceptions • Now let us understand the exception being carved out with respect toapplicability: • Aggregate of the payments made does not exceed Rs. 20,000 inFY. • Individual or HUF with turnover not exceeding Rs. 1 crores (business) or Rs, 50 Lakhs (profession) in the immediately preceding previous year relevant to previous year in which benefit or perquisite has been provided • FAQs/ Clarifications byCBDT • Let us discuss the scenarios that have been specifically clarified by the CBDT vide circular no 12 of2022: • Whether the taxability of the benefit/perquisite in hands of receiver needs to be checked bythe payer before complying with Section 194R? • NO • Benefit has to be in kind for the section to apply? NO • Perquisite in form of capital asset liable to TDS deduction under S. 194R? YES, irrespective of taxability the deduction has to bemade • Sales discount, cash discount, rebates covered as benefit/perquisite? • NO, the same has been specifically clarified to be excluded, however, the other incentives may be taxable such as (notexhaustive): • TV, computer, gold coin, mobile, etc. provided asincentive • Payer sponsors trip for recipient or his/her relatives upon achieving thetargets Free tickets toevent • Medicine samples to medicalpractitioners • Benefit/perquisite to employee covered u/s194R?

The same may be taxable u/s 17 of the Act and liable to TDS u/s 192 of the Act since the employee shall be provided benefit by virtue of employment and not for undertaking business or profession. However, if the person is engaged as independent consultant then he/she would be earning by way of profession liable to TDS u/s 194R for any benefit or perquisitereceived. • Reimbursements to service provider be liable for TDS u/s 194R? YES, if either of the conditions aretrue: • Invoice is not in the name ofcompany • Expense has not been incurred wholly or exclusively for the servicereceiver • Valuation of the benefit or perquisite is to be done in which manner? Benefit/ perquisite has been procured/purchased bythe provider B Purchasepr Pricecharg customers C Benefit/perquisite manufactured by theprovider 8. Limit of Rs. 20,000 in FY to be computed from whichperiod? The computation of the threshold shall begin from 01 April 2022 but liability to deduct TDS shall arise on the benefit or perquisite provided after 01 July2022 Conclusion The new provision is certainly going to create a lot of compliance burden for the taxpayers and would also lead to blocking of unnecessary working capital in the advance tax/ TDS form even if the benefit/perquisite is not taxable in the hands of the recipient. Further, the instances where as general trade parlance certain services/ products are provided additionally without any cost would also be liable to 194R since they might be considered as benefit/perquisite being provided to receiver such as freight being paid on behalf of the party (in case the bill is not raised by the transporter in name of receiving party), payments made in due course for administrative convenience, etc. This will certainly bring in more complexity in case to case basis where the business rationale may require undertaking the said exercise but the tax implication mayarise. Disclaimer: Nothing contained above shall be construed as a legal opinion/ advice or recommendation and the content is to be used strictly for educative purposes only. While reasonable efforts have been made tounderstand

the implications of new provisions, however, the author shall not be liable for any loss arising out from the reliance placed on the above understanding. For any queries the author can be reached at rishabh280695@gmail.com.