Download

1 / 8

80 likes | 86 Views

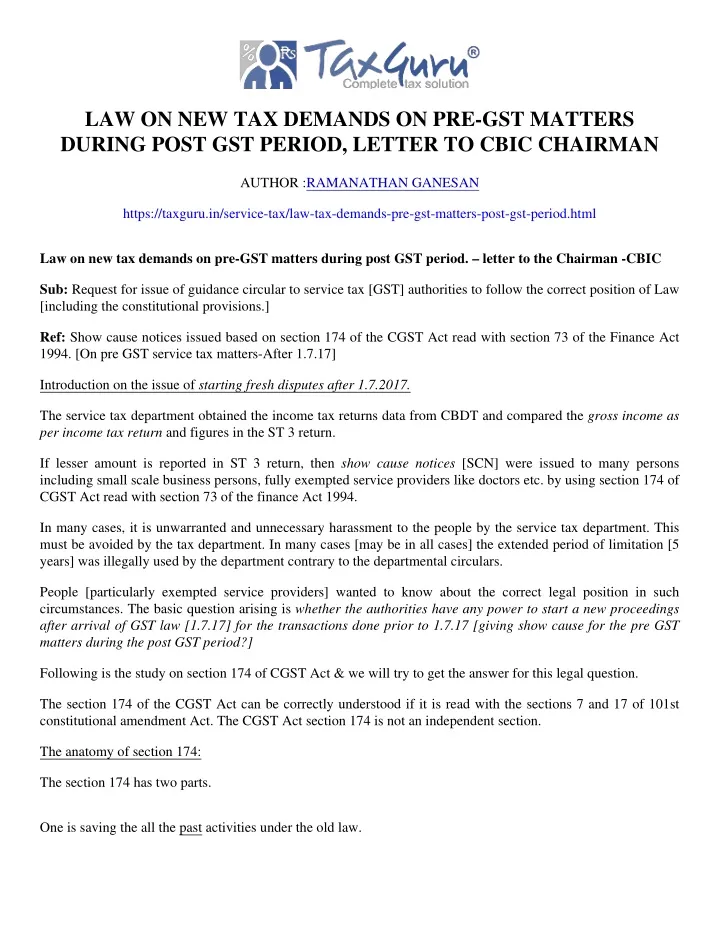

"Law on new tax demands on pre-GST matters during post GST period.u200a-u200aletter to the Chairman -CBIC Sub Request for issue of guidance circular to service tax"<br>TaxGuru is a platform that provides Updates On Amendments in Income Tax, Wealth Tax, Company Law, Service Tax, RBI, Custom Duty, Corporate Lawu00a0, Goods and Service Tax etc.<br>To know more visit https://taxguru.in/service-tax/law-tax-demands-pre-gst-matters-post-gst-period.html

E N D

LAW ON NEW TAX DEMANDS ON PRE-GST MATTERS DURING POST GST PERIOD, LETTER TO CBIC CHAIRMAN AUTHOR :RAMANATHAN GANESAN https://taxguru.in/service-tax/law-tax-demands-pre-gst-matters-post-gst-period.html Law on new tax demands on pre-GST matters during post GST period. – letter to the Chairman -CBIC Sub: Request for issue of guidance circular to service tax [GST] authorities to follow the correct position of Law [including the constitutional provisions.] Ref: Show cause notices issued based on section 174 of the CGST Act read with section 73 of the Finance Act 1994. [On pre GST service tax matters-After 1.7.17] Introduction on the issue of starting fresh disputes after 1.7.2017. The service tax department obtained the income tax returns data from CBDT and compared the gross income as per income tax return and figures in the ST 3 return. If lesser amount is reported in ST 3 return, then show cause notices [SCN] were issued to many persons including small scale business persons, fully exempted service providers like doctors etc. by using section 174 of CGST Act read with section 73 of the finance Act 1994. In many cases, it is unwarranted and unnecessary harassment to the people by the service tax department. This must be avoided by the tax department. In many cases [may be in all cases] the extended period of limitation [5 years] was illegally used by the department contrary to the departmental circulars. People [particularly exempted service providers] wanted to know about the correct legal position in such circumstances. The basic question arising is whether the authorities have any power to start a new proceedings after arrival of GST law [1.7.17] for the transactions done prior to 1.7.17 [giving show cause for the pre GST matters during the post GST period?] Following is the study on section 174 of CGST Act & we will try to get the answer for this legal question. The section 174 of the CGST Act can be correctly understood if it is read with the sections 7 and 17 of 101st constitutional amendment Act. The CGST Act section 174 is not an independent section. The anatomy of section 174: The section 174 has two parts. One is saving the all the past activities under the old law.

This part does not require any constitutional authorisation. Other one is issuing SCN even after 1.7.17 by using the old Finance Act 1994 machinery provisions. [Without constitutional authorisation] This is the disputed part. Section 174 enables voluntary payment of taxes of the past period [pre GST]. Nobody can be compelled to pay fresh demands made after 1.7.17. The machinery provisions will not work without constitutional power to tax services by the central government. Section 174 does not say that notwithstanding anything contained in the constitution of India, new proceedings can be initiated and fresh demands can be made. The section 174 says that the remedy may be instituted. [This means that the remedy may be instituted subject to the other provisions in the law [THE TAX PAYER INSISTS THAT THE CONSTITUTION OF INDIA SHOULD BE FOLLOWED BY THE TAX OFFICER.] First Let us understand about the superiority of constitution of India. 1. Why the constitution of India is the supreme legislation in India? Answer to the question is given below. Ans: The constitution of India is the mother of all other law. If a provision in any Act is inconsistent with constitution of India then such inconsistent part is invalid in law. The constitution of India is stated as the holy book of all Indians (by our Honourable Prime Minister of India). Amendment to the constitution requires special majority in the parliament. [2/3 members present should support the amendment with more than ½ of the total members support] 2. What are the limitations on the central government’s powers? Answer to the question is given below. Ans: The powers of the central government are limited to the union list in the 7th schedule of the constitution of India. After satisfying the specified conditions, powers in concurrent list can be used. The scope of the functions of the central government can be given in a specific Article also. The scope of functioning of the Central government is clearly defined in the Union list. If the central government exceeds its powers than, those excess are ultra vires & legally not valid. Except the above, all others are none of the business of the central government. 3. What is the authorising provision in service tax law? Answer to the question is given below.

Article 268A and entry number 92c (Tax on services) in the union list in the 7th schedule of the constitution of India. These two points authorised the central government to impose tax on services in the past [pre 101st CAA position]. “To tax service” is the high level decision by the parliament. It is the superior decision of the parliament in the superior legislation. 4. What is the machinery provision in the service tax law? Answer to the question is given below. The Finance Act 1994 part V- speaks about “How to tax services”, when to tax etc in relation to the levy and collection of service tax. This is the machinery provision in the subordinate legislation. This is the consequential decision based on the principle decision of authorising to levy tax on services. 5. The 101st constitutional amendment Act is the foundation for the GST law. 6. Section 7 and 17 of the 101st constitutional amendment Act OMITTED Article 268A & Entry number 92 c. 7. The above said article 268A and entry number 92c was not repealed & fully OMITTED. The CGST Act Section 174 saves the machinery provision. But the Authorising provision in the constitution of India [To tax services by the central government in a monopolistic, standalone & in the old tax structure] was not saved or not repealed but simply omitted. Consequently, the machinery provision without authorising provision cannot enable the central government to continue to enjoy the power to tax services as per the old, abandoned tax structure. 8. The terms “OMITTED” and “repealed” gives two different meanings as per the decision of the Honourable apex court. Please see annexure-1 9. The OMITTED part of law cannot have any force after its deletion. (Even during the past period during which it was in force). It is full stop and not partial stop. This is as per the Honourable Supreme Court decision. 10. Demanding tax on service after deleting entry 92c and article 268A is an unauthorized act of the central government and consequently, an unauthorized act of officer of the central government also. 11. The already determined taxes by the orders passed by the department authorities are dues of government. They are concluded matters. Initiating a new proceedings & raising fresh demands after 101st constitutional amendment Act is unlawful, unreasonable, & un-constitutional. Under this situation, erroneously demanding service tax on exempted services is a great grievance to the public. It damages the Goodwill of the government. The constitution of India stopped the right of the central government to tax services in a monopolistic manner. This full stop provision is in section 7 and 17 of the 101st constitutional amendment Act. The constitution

prohibited the standalone Act for taxing services. The central government’s possession of power to tax service is the pre-condition for the fresh demanding of service tax after 1.7.17. The standalone power to tax services is none of the business of the central government after 101st constitutional amendment Act. The position Prior to 1.7.17: Article 268A + Entry No. 92c in union list + Finance Act 1994 part V = A constitutionally valid law to tax services. The position After 1.7.17: No article 268A + No Entry No92c in union list [only Finance Act 1994 saved provisions] = A constitutionally void law to tax standalone services only. The constitution of India started giving or has granted new joint power for the central government and state governments to tax goods and services. A consolidated Act for taxing goods and services is the only option available in the constitution of India without monopolistic power for the central government. [Except in exceptional circumstances] The parliament did not grant any power to tax goods or services in a standalone manner in Article 246A(1). The scheme of the new power is different from the old power. This prospective new power is granted by the section 2 of the 101st constitutional amendment Act. The very basic purpose of the 101st constitutional amendment Act is standalone Acts for taxing goods or services must end. Accordingly, the constitutional power to tax goods and services cannot be used to support the section 174(2) (d) & (e) of the CGST Act to make fresh demands. Article 246A(1) enables the GST law prospectively and not retrospectively. The Article 246A cannot occupy the place of the 268A & entry no 92c on the following reasons. 268A provided the Monopoly right to tax services (old law) for the central government. Article 246A provides a shared right to tax services (new law). Scheme & objective of the old and new laws are different. Constitution of India is supreme law. All other Acts of parliament are subordinate laws. The constitution law prevail over other laws. The tax payer relies on constitution law that the central government’s power to tax services in a standalone manner is prohibited. This must prevail over the CGST Act section 174(2) (d)&(e). Further, if two views in the law are available, then the beneficial view to the assesse must be followed as per the Supreme Court Ruling in vegetable product case law. On the top of everything the central government has announced in press information bureau on 22.7.17 that the past transactions are not to be checked. Conclusion: Whether the section 174 is really an enabler for making fresh demands on pre GST matters during post GST Period? [In spite of the section 7 & 17 of the 101st constitutional Amendment Act and in spite of central government announcement in PIB on 22.7.17 (past transactions are not to be checked under GST)] Ans: Section 174 must be read with section 7 & 17 of the constitutional Amendment Act. In such situation, anyone can understand that CGST Section 174 saves all past activities.

Section 7 and 17 of CAA overrides the section 174 while starting fresh disputes [fresh Show Cause Notice] under service tax law [section 73 of the finance Act 1994] after 30.6.17. The parliament ordered to STOP complicated old tax structure by way of omitting the old, monopolistic “power to tax services” by the union government in the constitution of India. The parliament further ordered to START new, simplified tax structure as enabled in Article 246A. Under this article it is not possible to tax services alone under separate Act and separate charging section; then, goods alone under the separate Act and separate charging section. There should be a common charging section to tax goods and services. Such a common charging section alone gives power to tax by union & state governments. Hence, the officers of the union government must STOP the new demands after 1.7.17 under the old tax structure by using section 174 CGST Act. They cannot override the constitution of India and the intentions of the parliament to STOP the old tax structure. Accordingly, the CGST Act section 174 powers are given to handle the pending proceedings. This is the harmonious, reasonable & only possible interpretation of law. After 1.7.17, a court may order for the remand of case to the adjudicating authority and that adjudicating authority may have to “re do” his job. In such circumstances section 174 powers can be used. Old proceedings is not affected by new law is the intention of section174. There is no wording in the section 174 for empowering the authorities to commence new proceedings after 1.7.17 in spite of Constitutional constraints. The abandoned provisions (article 268A and entry number 92c that is deleted provisions) disabled fresh demands after 101st constitutional amendment Act. The new provision Article 246A does not give retrospective power to raise fresh demands under the old & monopolistic tax structure. Either this way (retrospective effect in 246A) Or that way (Repeal of old 268A & entry 92c way) the central government did not retain the power to Tax services in a standalone & monopolistic manner in the old tax structure. The authority to tax on services has gone constitutionally. The standalone tax on services is not the function of the central government after 30.6.17. Hence on 22.7.17 the central government in PIB has announced that the past transactions are not to be checked under GST. Under these circumstances, there is no way to raise fresh demands in service tax after constitutional amendment Act. Unfortunately, based on the erroneous understanding of the law, some GST Department officials issue show cause notices and orders using inappropriate section 174 of the CGST Act contrary to the intentions of the law and in the unconstitutional manner. The intention of parliament is to remove the power of Central government to Tax services in a standalone manner. Consequently, Article 268A and Entry number 92c were omitted without savings. The intention of parliament is that the central government should not use the power to Tax services retrospectively. Therefore the Article 246A does not give the retrospective power to the central government. The ultimate intention of the parliament is that the central government should not have the power to Tax services prior to 1.7.17 so as to prevent the fresh demands after 1.7.17 in a standalone manner based on old tax structure. Contrary to the intention of parliament the central government cannot use the power to tax services in any other manner also by circumventing the law. The intention of parliament and central government was expressly made

in the announcement in the press information bureau, of Government of India on 22.7.17. The Government believes in voluntary compliance. The tax payer asks the officer to show which part of constitution of India empowered the central government to tax services in standalone manner after omission of article 268A and entry No92C in the union list. The old tax structure [Finance Act 1994 – service tax part] is like an unusable, torned, fade shirt. The new tax structure is like a new shirt. The parliament wants that the central government must wear the new shirt only. The officers of the central government cannot override parliament and government announcement in PIB on 22.7.17. The sabka Vishwas legacy dispute resolution scheme was introduced with a view to dispute reduction and to close old disputes. [The Sabka Vishwas Scheme, 2019 is a scheme proposed in the Union Budget, 2019, and introduced to resolve all disputes relating to the erstwhile Service Tax and Central Excise Acts] Contrary to this good intention of the government, CBIC is on the unwarranted new dispute creation mode on the matters relating to pre GST period. New proceedings were initiated contrary to Law and facts by the mere comparison of direct tax returns with indirect tax returns after normal limitation period. It is not the comparison of comparable. Both returns were designed for different purposes. The meaning of different terms in indirect tax law and direct tax law differ. Both were not designed for the comparison purpose. The direct tax return and indirect tax returns both are in the hands of the finance ministry. In such situation, it is not possible for the finance ministry to accuse the income tax payer as he suppressed facts and thereby invoking the extended period of limitation. The comparison of direct tax returns with indirect tax returns – to create a dispute on pre GST matters is and ill thought and poorly conceived (apart from contrary to law and contrary to the policy of the government). A person who wants to suppress the facts from the finance ministry would not give the same facts to the finance ministry in his income tax return. The following phrase appearing in section 174 2 d “May become due” & The following phrase appearing in section 174 2 e of CGST Act “…and any such investigation, inquiry, verification (including scrutiny and audit), assessment proceedings, adjudication and other legal proceedings or recovery of arrears or remedy may be instituted, continued or enforced, and any such tax, surcharge, penalty, fine, interest, forfeiture or punishment may be levied or imposed as if these Acts had not been so amended or repealed” … causes a mistaken notion that these phrases are enabling provisions to start a fresh proceedings in service tax matters on pre-GST matters in the post GST period. The constitutionality of these two phrases is disputed by the tax payers. The enabling the future operation is not enabled in the constitution. These provisions may be used without Let down of the constitutional provisions in 101st constitutional amendment Act section 7 and 17 in a harmonized manner.. These provisions maybe of use for doing re assessment as per the direction of any court to “re do” the adjudication on the proceedings originally started prior to 1.7.17.

In the case of repugnancy, the harmonious construction must be followed. Section 7 and 17 of the 101st constitutional amendment Act read with the Honourable Supreme Court Ruling is in favor of the tax payer. [Given in annexure] The Article 246A is not having retrospective. This is also in favor of the tax payer. The government announcement on 22.7.17 in press information bureau is also in favor of the tax payer. The government policy which is the basis for sabka Vishwas 2019 (believing in voluntary compliance) is also in favor of the tax payer. Though CGST Act section 174 is in favor of the department, it must be used in exceptional and essential situations only so as to give effect to the constitutional provisions as said above. The difference between the old tax regime and the GST regime [from 1.7.17] can be explained as follows with an example. The taxes paid after dispute cannot be shifted to service recipients [due to long time gap] and even if shifted the recipients cannot take ITC as there is no enabling provisions in the transition law. The taxes paid for the old regime cannot be used as ITC in the GST regime. In general, if service provider pays tax, then the service recipient should be able to get input tax credit. This is the basic in indirect tax value added tax system. Hence, the constitution of India disabled fresh disputes on pre GST matters in post GST period. Example: A tax payer provided exempted services [non-taxable as per the notification 25/2012] and submitted income tax return. He is not liable to submit the ST 3 Return and hence, he did not submit it. In such situation, the adjudicating officer by mentioning some invalid reasons, contrary to law and contrary to facts demanded service tax merely based on sales amount in the income tax return. This is very unfortunate. The commissioner [appeals] does not have the judicial responsibility to protect the tax payer rights as per the law in many occasions. There is no such effective law to fix responsibility. Hence, the appeal commissioners confirm the order of the adjudicating authority in a mechanical manner. Now, this tax payer must bear the entire tax burden. He cannot: 1. Shift the tax burden to the service recipient. 2. He cannot get the Input Tax Credit [ITC] and 3. He cannot give ITC as there is no enabling provision and it is not practically possible also. This would be contrary to the principles of the Indirect tax. This amounts to economically killing that person. Therefore, the new tax structure [GST regime] does not have the constitutional authority to start a new service tax dispute after 30.6.17 on the pre GST matters. This 30.6.17 is the cut-off point; beyond this point new disputes on old tax regime matters cannot be initiated. Request to the CBIC: We request the CBIC to issue suitable instructions circular to Adjudicating authorities in the following manner.

Dispute management guidelines – Service tax demands raised on Pre-GST matters during post GST. Disputes or demands raised based on comparison of income tax records and ST3 service tax returns – (Demands raised under section 174 of CGST Act read with section 73 of the finance act 1994)- In this type of cases, service tax exemption [As per Notification 25/2012] may be allowed on self-declaration basis at any stage of proceedings (including Appeal before the commissioner). In this type of cases, in the assessee’s appeal before CESTAT or in High court, the department side need not raise objection against allowing of the assessee’s appeal. The CBIC welcome the voluntary payment of taxes; however pressing the service tax demands made after 1.7.17 would not be appropriate in view of the omission of article 268A and entry number 92c of the union list without savings. (The constitutional amendment was made with view to stop the old tax structure and start the GST tax structure). I have submitted the above views and the requested in public interest & the department can avoid actions which will “only yield disputes” and not revenue. The views expressed herein are personal views. It is necessary to take professional advice before taking any decision.