Download

1 / 2

20 likes | 24 Views

"Corporate Restructuring through amalgamation, arrangement, mergers, acquisitions, and takeovers has become vital to corporate strategy today. Corporate transact"<br>TaxGuru is a platform that provides Updates On Amendments in Income Tax, Wealth Tax, Company Law, Service Tax, RBI, Custom Duty, Corporate Lawu00a0, Goods and Service Tax etc.<br>To know more visit https://taxguru.in/goods-and-service-tax/treatment-gst-case-amalgamation-merger.html

E N D

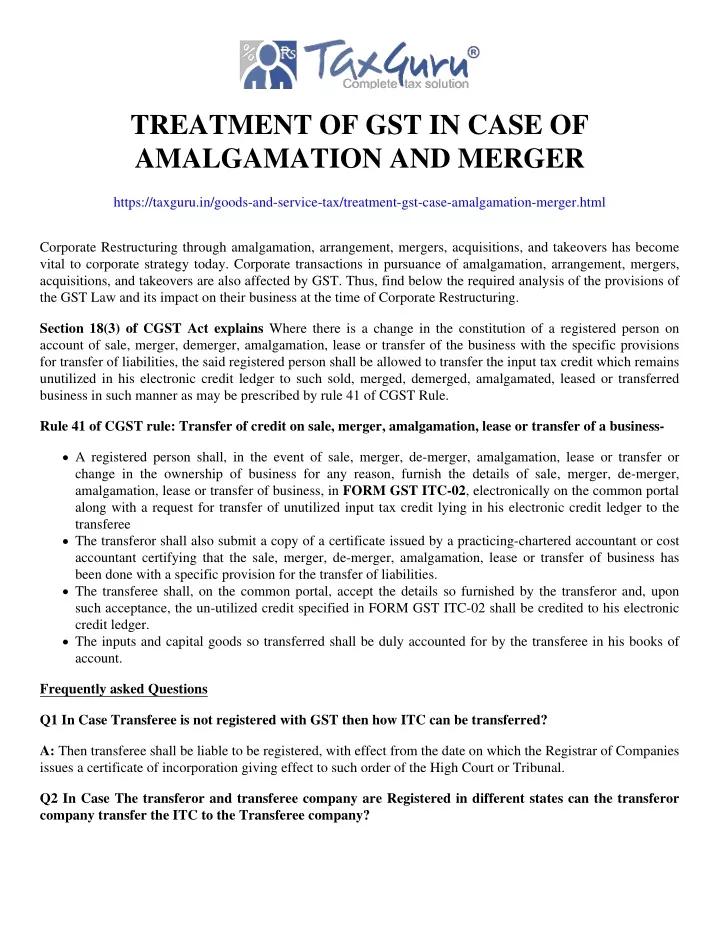

TREATMENT OF GST IN CASE OF AMALGAMATION AND MERGER https://taxguru.in/goods-and-service-tax/treatment-gst-case-amalgamation-merger.html Corporate Restructuring through amalgamation, arrangement, mergers, acquisitions, and takeovers has become vital to corporate strategy today. Corporate transactions in pursuance of amalgamation, arrangement, mergers, acquisitions, and takeovers are also affected by GST. Thus, find below the required analysis of the provisions of the GST Law and its impact on their business at the time of Corporate Restructuring. Section 18(3) of CGST Act explains Where there is a change in the constitution of a registered person on account of sale, merger, demerger, amalgamation, lease or transfer of the business with the specific provisions for transfer of liabilities, the said registered person shall be allowed to transfer the input tax credit which remains unutilized in his electronic credit ledger to such sold, merged, demerged, amalgamated, leased or transferred business in such manner as may be prescribed by rule 41 of CGST Rule. Rule 41 of CGST rule: Transfer of credit on sale, merger, amalgamation, lease or transfer of a business- A registered person shall, in the event of sale, merger, de-merger, amalgamation, lease or transfer or change in the ownership of business for any reason, furnish the details of sale, merger, de-merger, amalgamation, lease or transfer of business, in FORM GST ITC-02, electronically on the common portal along with a request for transfer of unutilized input tax credit lying in his electronic credit ledger to the transferee The transferor shall also submit a copy of a certificate issued by a practicing-chartered accountant or cost accountant certifying that the sale, merger, de-merger, amalgamation, lease or transfer of business has been done with a specific provision for the transfer of liabilities. The transferee shall, on the common portal, accept the details so furnished by the transferor and, upon such acceptance, the un-utilized credit specified in FORM GST ITC-02 shall be credited to his electronic credit ledger. The inputs and capital goods so transferred shall be duly accounted for by the transferee in his books of account. Frequently asked Questions Q1 In Case Transferee is not registered with GST then how ITC can be transferred? A: Then transferee shall be liable to be registered, with effect from the date on which the Registrar of Companies issues a certificate of incorporation giving effect to such order of the High Court or Tribunal. Q2 In Case The transferor and transferee company are Registered in different states can the transferor company transfer the ITC to the Transferee company?

A: No, the credit Accumulated from the tax period to the one state govt can be used/setoff against the tax that is liable to be paid to another state govt, such an interpretation would be completely against the premise under the entire law drafted. The CGST Act and the Rules drafted thereof are implemented in such a way that there is no cross utilization of revenue between the states. It is for this very reason the form ITC-02 does not permit the transfer of Inter-state ITC and allows it only if the GSTIN of both the transferor and transferee belong to the same state. Therefore, in the case of transfer of the business of sale, Amalgamation, merger, demerger, etc. between entities located in two different states, the ideal way would be to terminate the registration in one state and get a refund of the unutilized ITC or cross charge the other entity and transfer the ITC. So, at the outset as per GST provisions, the transfer of ITC between two GSTINs can happen only if the transaction under section 18 occurs between two entities located in the same state and not otherwise. Q3 From when transferee company liable to pay tax under act. A: Section 87(1): – If 2 or more companies are amalgamated or merged in pursuance of the order of the Court or tribunal or otherwise and the order of amalgamation or merger will take effect from a date earlier to the date of the order. If there is any supply of goods or services or both take place between any two or more of such companies between the date of effect of such order and the date of the order, such supply and receipt will be included in the turnover or receipt of the respective companies and they shall be liable to pay taxes. Let’s Understand with an example Amalgamation takes place between A Pvt Ltd. And X Pvt Ltd. In pursuance of the order of the Court and such order is passed on 11th Aug 2022 but this order will be effective since 8th June 2021. A Pvt Ltd. Supplied goods of Rs. 500000 to Xyz Pvt Ltd on 15th September 2021. That supply has been made between 8th June 2019 and 11th Aug 2020. Such Supply will be considered as the turnover of A Pvt Ltd and receipt of Goods of X Pvt ltd. And accordingly, both A Pvt Ltd. And X Pvt Ltd will be liable to pay tax. Section 87(2): For the purpose of this Act, the said 2 or more companies shall be treated as distinct companies for the period up to the date of order and the registration certificate shall be cancelled with effect from the date of said order. Example: – In the above example the date of order is 11th Aug 2022 So A Pvt Ltd and X Pvt Ltd shall be considered as distinct persons till the date of order i.e. 11th Aug 2022. Q4 Is GST applicable on the transfer of Share by the transferor company to the transferee company? A: The usual mode is the acquiring of the company by making an offer by the transferee company to the shareholders of the transferor company to purchase their securities, in the transferor company, at a price stated for the purpose. The definition of goods, as well as services under the GST regime, do not cover the securities, therefore GST would not be levied on the sale of securities Disclaimer: The views expressed in this article are the personal views of the author. Neither the views nor the analysis constitute a legal opinion and are not intended to be advice