Download

1 / 7

70 likes | 169 Views

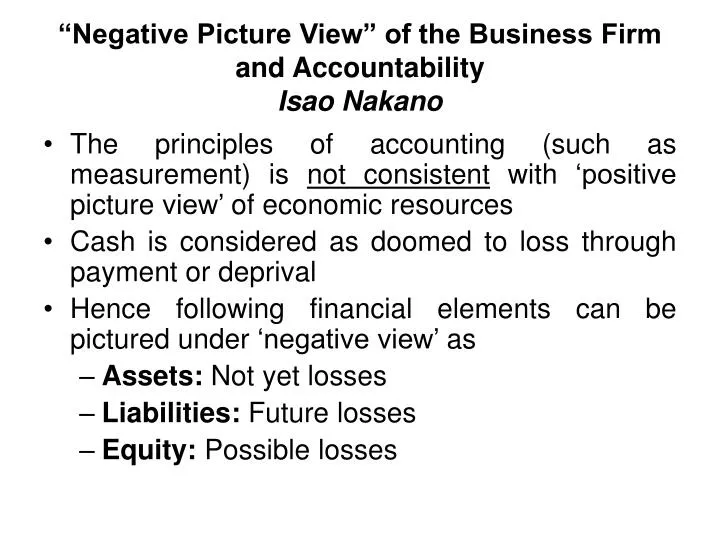

“Negative Picture View” of the Business Firm and Accountability Isao Nakano. The principles of accounting (such as measurement) is not consistent with ‘positive picture view’ of economic resources Cash is considered as doomed to loss through payment or deprival

E N D

“Negative Picture View” of the Business Firm and AccountabilityIsao Nakano • The principles of accounting (such as measurement) is not consistent with ‘positive picture view’ of economic resources • Cash is considered as doomed to loss through payment or deprival • Hence following financial elements can be pictured under ‘negative view’ as • Assets: Not yet losses • Liabilities: Future losses • Equity: Possible losses

“Negative Picture View” of the Business Firm and AccountabilityIsao Nakano • Hence following financial elements can be pictured under ‘negative view’ as (Contd..) • Expenses: Not yet losses under stationeriness • Revenue: Compensated losses • Net Income: An increase in compensated losses

“Negative Picture View” of the Business Firm and AccountabilityIsao Nakano • Assets are considered as ‘not yet losses’ as they are destined for loosing by consumption, utilization, transfer of forfeiture • This theory says that • Positive economic forces have to be debited • Negative forces is to be credited

“Negative Picture View” of the Business Firm and AccountabilityIsao Nakano • Hence, this theory has an impact on Double Entry system as well • E.g. Acquisition of Inventory • + Not yet losses (e.g. Inventory) DR • - Not yet losses (e.g. Cash) CR • E.g. Issues of Share Capital • + Not yet losses (e.g. Cash) DR • - Possible losses (Capital) CR

Evolution in Management Accounting • Following four stages are recognized • Stage I: Prior to 1950. Focused on cost determination and financial control through budgeting and cost accounting technologies • Stage II: By 1965, the focus shifted from provision of information for mgt planning and control, through the use of decision analysis and responsibility accounting

Evolution in Management Accounting • Following four stages are recognized (contd..) • Stage III: By 1985, Focused on reduction of waste of resources in business processes through process analysis & cost mgt techniques • Stage IV: By 1995, Attention shifted to the generation or creation of value through the effective use of resources, technologies for identifying drivers of customer value, SH value and innovation

Evolution in Management Accounting • Following four stages are recognized (contd..) • Stage I: Technical • Stage II: Management Activity (Staff Role) • Stage III & IV: Integral part of management process