Download

1 / 28

280 likes | 284 Views

Stay updated on the latest NFP (Not-for-Profit) reforms and compliance with MI (Member Incorporation) member standards. This seminar provides an overview of the reforms and their impact on charities, including the ACNC Act and statutory definition of charity. Learn about current obligations and future changes, as well as the proposed reforms for "in Australia" requirements and exempt foreign income. Please note: This seminar does not provide legal advice.

E N D

MI Member Compliance Charity reform update Compliance with MI Member Standards Time for questions Please note: This seminar does not provide legal advice

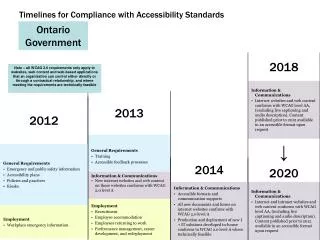

NFP Reforms – Overview • NFP Reforms – since 1995 • 15.5 Million words; 50,000 pages. • Gov’t commissioned 3,000 reports. • NFP Sector – 4,500 responses; 29,000 pages • Prof Myles McGregor Lowndes – CMA Conference 2013

NFP Reforms – Overview • ‘In Australia’ Legislation • ACNC Act • Statutory Definition of Charity • Governance Regulations • UBIT - scrapped

Other Reforms impacting charities • A multitude of Federal and State/Territory laws including: • Privacy • OH & S • Working with children • Fundraising etc

ACNC – Background • Charity Status determined by ATO • 3 December 2012 – ACNC became operative • Public information portal • Decider of charitable status but not tax concessions (ATO) • Minimum governance standards • Financial reporting framework • External conduct standards – not yet

ACNC – Current obligations • Good Governance • Five governance standards • Ensure objects in constitution are consistent with mission statement and practice. • Annual Information Statement • Keep records • Update details – constitution, responsible persons etc

ACNC – Future • To be abolished and replaced by Centre of Excellence • Options paper: • Self-reporting requirements – back to ASIC • Returning determination of charitable status to ATO • Charities required to maintain publically accessible website with names of responsible persons, details of all government funding, financial reports. • Nothing certain

Statutory Definition of Charity • Charities Act passed in June 2013 & Commenced 1 Jan 2014 • Definition previously based on common law • Gives certainty to ‘Advancing Religion’ as a statutory Head of Charity • Codifies many other purposes as charitable

“In Australia” Requirements - Background • The issues (1995): • Control of funds going off-shore – tax avoidance, anti-terrorism and money laundering. • International treaty obligations – regulate movement of money between countries. • Need to protect the integrity of charitable activity

“In Australia” Requirements - Background • The Answer: • Taxation law used as a control mechanism • Taxation Laws Amendment Act (No 4) 1997 • Income tax exempt charities barred from sending funds overseas unless they meet certain conditions.

“In Australia” Requirements - Current • To be endorsed by the ATO as income tax exempt, a charity must meet one of three tests: • “In Australia” test • Deductible Gift Recipient (DGR) test • Prescribed by law test • Missions Interlink and its Members are prescribed by law

“In Australia” Requirements – Reform • The issues: • Law below treaty obligations • Word Investments case • Government announced in 09/10 budget that it would amend the “in Australia” Special Conditions for tax concessions to better control those organisations passing money to overseas charities and other entities.

“In Australia” Requirements – Reform Process • July/August 2011 – first exposure draft & public consultation • April/May 2012 – second exposure draft & public consultation • August 2012 – Bill introduced to Parliament • June 2013 – Some of the provisions of 2012 Bill were enacted • August 2013 –2012 Bill lapsed at the dissolution of Parliament • December 2013 – Current Government announced it would proceed with reforming the “in Australia” requirements • March 2014 – new exposure draft & public consultation

“In Australia” Requirements – Proposed • The restated “in Australia” special conditions move away from expenditure-based test to allow consideration of a wide range of circumstances. • “Tracing” of money given to another enitity. • Stricter conditions on “disregarded amounts”. • Much more difficult and greater compliance required for organisations with overseas activities to meet “in Australia” conditions.

“In Australia” Requirements – Proposed • The exposure draft maintains the existing prescription of Missions Interlink and its Members, exempting them from the new “in Australia” requirements for income tax entities. • Wait and see……

Exempt Foreign Income – personal income tax • The issue (2009): • Australians earning large sums of money overseas not subject to Australian income tax. • “Better targeting the income tax exemption for Australians working overseas”. • Changes to Section 23AG of the Income Tax Assessment Act 1936 effective 2009/2010.

Exempt Foreign Income – personal income tax • Section 23AG: • Foreign income of personnel (Australian residents for income tax) • working continuously overseas for more than 91 days is exempt from Australian income tax if directly attributable to activities of a prescribed institution exempt from Australian income tax because it is pursuing objectives outside Australia. • Personnel of MI Accredited Members fit this exemption. • Income to be declared as “exempt foreign income”.

Missions Interlink Member • Compliance with MI Standards • Missions Interlink Standards Statement • Missions Interlink Member Accreditation Standards • MI Member log-in to www.missionsinterlink.org.au • Username: missions Password: Psalm145

Missions Interlink Member • Compliance with MI Standards • Missions Interlink Standards Statement • MI Member log-in to www.missionsinterlink.org.au • Username: missions Password: Psalm145

Missions Interlink Member • Compliance with MI Standards • Missions Interlink Member Accreditation Standards • MI Member log-in to www.missionsinterlink.org.au • Username: missions Password: Psalm145

Missions Interlink • Member Accreditation Standards • 1. An Australian organisation • MI Member log-in to www.missionsinterlink.org.au • Username: missions Password: Psalm145

Missions Interlink • Member Accreditation Standards • 2. Financial Standards • MI Member log-in to www.missionsinterlink.org.au • Username: missions Password: Psalm145

Missions Interlink • Member Accreditation Standards • 3. Governance and Accountability Structure • MI Member log-in to www.missionsinterlink.org.au • Username: missions Password: Psalm145

Missions Interlink • Member Accreditation Standards • 4. Tax Status • MI Member log-in to www.missionsinterlink.org.au • Username: missions Password: Psalm145

Missions Interlink • Member Accreditation Standards • 5. Accreditation Confirmation • MI Member log-in to www.missionsinterlink.org.au • Username: missions Password: Psalm145

Missions Interlink • Member Accreditation Renewal • 2014 Member Declaration • Use web link in renewal letter