Download

1 / 15

150 likes | 248 Views

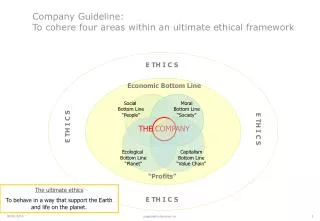

Branding for Bottom-Line Results Chicago-Kent College of Law Bell, Boyd & Lloyd LLC October 25, 2001. Aron Levko IP Practice Leader, Partner - Chicago. Growth of Intellectual Asset Value. 12. 80%. 10. 76%. 78%. 8. 74%. 6. 68%. 4. 65%. 58%. 2. 0. 1998. 1994. 1996. 1997. 1999.

E N D

Branding for Bottom-Line ResultsChicago-Kent College of LawBell, Boyd & Lloyd LLCOctober 25, 2001 Aron Levko IP Practice Leader, Partner - Chicago

Growth of Intellectual Asset Value 12 80% 10 76% 78% 8 74% 6 68% 4 65% 58% 2 0 1998 1994 1996 1997 1999 2000 1995

Recent Changes in Accounting Standards • The Financial Accounting Standards Board (FASB) has recently issued new rules for how companies record intangible assets in a purchase and also how to account for the treatment of the intangible assets over time. • FASB Statement 141 ‘Business Combinations’ • FASB Statement 142 ‘Goodwill and Other Intangible Assets’ • FASB Disclosure Draft ‘Improving Disclosure of Intangible Assets’

FASB Statement 141 ‘Business Combinations’ • FASB Statement 141 improves the transparency of the accounting and reporting for business combinations • The purchase method must be used for business combinations initiated after June 30, 2001. • Companies can no longer use the pooling-of-interests method of accounting for business combinations in which the companies combined balance sheet line items. • Some intangible assets can now be recognized apart from goodwill in a business combination on the balance sheet. • Businesses will have to determine the ‘value’ of their intellectual assets at the time of purchase.

FASB 142 - Accounting for Brand Value • As intellectual assets do not ‘depreciate’ based upon definite useful lives as compared to tangible assets, a company must instead recognize when and if these assets have been damaged or impaired over time. • For example, a big brand that suffers a safety recall must account for the damage to the brand value. • Companies will now have to assign a value to intangibles on an annual or interim basis when such events exist. • Operating cash flow losses • Decline in market share • Significant cost increases • Product recalls

A Context for Valuation • Given the growing importance of intellectual assets, the question now becomes one of a determination of value. However, before deciding the proper technique to determine value, its context must be considered. • Perspectives of valuation context include

Valuation Methodologies The three most prevalent techniques to determine an intellectual asset’s value include: • The Cost Approach • The Market Approach • The Income Approach The usefulness and applicability of each approach is dependent upon the characteristics of the intellectual asset being valued and the purpose of the analysis.

Market Approach - Comparable Licenses Considerations • Exclusivity • Field of Use • Geographic restrictions • Relative strengths of trademark • Market share • Nature of market • Co-Promotion/marketing rights • Manufacturing rights

License Survey: Consumer Products Industry Distribution of Royalty Percentages 100 90 80 70 # of Agreements 60 50 40 30 20 10 0 1%-5% 6%-10% 11%-15%

Income Approaches • Excess Earnings • Premium profits (Income Differential) • Relief from Royalty • Real Options

Relief from Royalty Example • Product team proposes to purchase a brand for a new drug to treat the common cold • Management applies a 2% royalty rate, 30% discount factor and a terminal value capitalization of 12% A Sample Calculation:

Comparison of Valuation Methodologies Discounted Cash Flow Relief from Royalty Cost Market • Strengths • Market considerations • Future Cash Flows • Strengths • Ownership • Future Cash Flows • Strengths • Ease of Use • Applicability • Strengths • Ease of Use • Applicability • Issues • Future potential • Market Considerations • Issues • Aggregation problems • Additional Investments • Issues • Comparables • Special considerations • Issues • Impact of discount rates • Additional Investments

Benefits of Licensing • Awareness- through licensing of properties onto synergistic products companies can raise awareness of their core brand without the expensive advertising campaigns. • Income - licensing can provide companies with significant revenue streams through royalties. • Protection - by using a brand actively in the market place, companies can protect themselves from infringers or challenges to their trademarks.

A Final Note If you can ‘visualize’ your technology or brand value, you can measure it. If you can measure your technology or brand value, you can manage it. If you can manage it, you can realize optimum value.