Download

1 / 22

230 likes | 272 Views

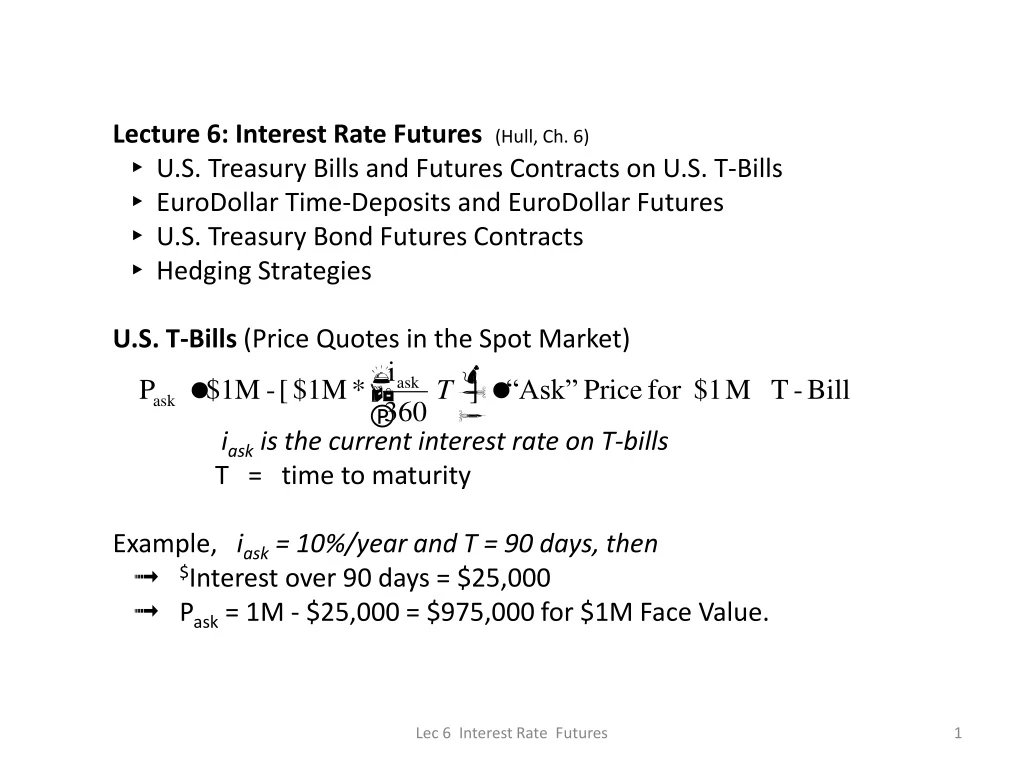

Lecture 6: Interest Rate Futures (Hull, Ch. 6) ▸ U.S. Treasury Bills and Futures Contracts on U.S. T-Bills ▸ EuroDollar Time-Deposits and EuroDollar Futures ▸ U.S. Treasury Bond Futures Contracts ▸ Hedging Strategies U.S. T-Bills (Price Quotes in the Spot Market)

E N D

Lecture 6: Interest Rate Futures (Hull, Ch. 6) ▸ U.S. Treasury Bills and Futures Contracts on U.S. T-Bills ▸ EuroDollar Time-Deposits and EuroDollar Futures ▸ U.S. Treasury Bond Futures Contracts ▸ Hedging Strategies U.S. T-Bills (Price Quotes in the Spot Market) iask is the current interest rate on T-bills T = time to maturity Example, iask = 10%/year and T = 90 days, then ➟ $Interest over 90 days = $25,000 ➟ Pask = 1M - $25,000 = $975,000 for $1M Face Value. Lec 6 Interest Rate Futures

U.S. T-Bill Futures Contract Contract: 90-day U.S. Treasury bills Exchange: IMM at CME Delivery: Mar, Jun, Sep, Dec. Contract Size: $1M (FV) Example: Go long one Dec T-Bill futures at IMM index = 90.00 In English, I have agreed to: • Buy $1M (FV) of U.S. T-Bills with 90 days to maturity • actual trade will take place 3rd week in December • IMM index = 90.00 ➟ Forward Rate = (100-IMM index)/100 = 0.10 ➟ Futures Price = $1M { 1 – (0.10/360) x 90} = $975,000 Thus, the Index is like a price: Price of a zero coupon bond with Face Value = $100. if IMM index ↑ Long gains, if IMM index ↓ Long loses. Just like stocks. Lec 6 Interest Rate Futures

Daily Settlement (i.e., Daily Mark to Market) Lec 6 Interest Rate Futures

What Happens at Expiration? Suppose the last Settle IMM = 92.50 ➟ Forward Rate = 100-92.50 = 7.5% = Spot Rate ➟ Spot Price = Futures Price = $1M { 1 – (0.075/360) x 90} = $981,250 Cumulative Δ = $981,250 - $975,000 = + $6,250 ➟ Long gained $6,250, ➟ Short lost $6,250 A. Long Buys T-Bills thru futures. ▸ Long receives $1M (FV) of T-Bills from short. ▸ Long pays $981,250 to short. ▸ But, Long gained $6,250 in the futures market. Therefore Actual cost = 981,250 - 6,250 = $975,000. (Just as originally agreed) Lec 6 Interest Rate Futures

B. Close futures position, and buy in the spot mkt ▸ Go Short 1-Dec-futures at 92.50 (to close long position). ▸ Long pays $981,250 in the spot market. ▸ But, Long gained $6,250 in the futures market. Therefore Actual cost = 981,250 - 6,250 = $975,000. (Just as originally agreed) Lec 6 Interest Rate Futures

Euro$ Time Deposits ▸ U.S. Banks (e.g., BoA) will accept only US dollars for deposits ▸ Banks in London will accept US$ deposits: Euro$ Deposits ▸ LIBOR is the interest rate on these funds Euro$ Futures Contract Contract: 90-day EuroDollar Time Deposit Exchange: IMM at CME Delivery: Mar, Jun, Sep, Dec. Settlement in Cash Contract Size: $1M (FV) Notes 1. The underlying asset is a 90day Eurodollar deposit with FV = $1M 2. Daily “Mark to Market” is exactly the same as for US T-Bill futures 3. At expiration, Euro$ Futures are settled in cash. 4. Futures contracts range in maturity from 1-month to 10 years. Lec 6 Interest Rate Futures

Hedging Example 6.8: Use Euro$ Futures to Hedge Interest Rate Risk ▸ UTC needs to borrow $15M for 3-months (May, June and July). Interest paid monthly. ▸ Monthly interest rate (set at the beginning of each month) = LIBOR + 1% ▸ On April 30, LIBOR = 0.08/yr. ➟ interest due on May 30 = $15M*(0.08+0.01)/12 = $112,500 LIBOR ➀ 0.08 Borrow $15M ➀ $112,500 June Interest = ? July = ? |–––––––––––––––––|–––––––––––––|–––––––––––––––| 0 1 2 3 Apr 30 May 30 Jun 30 July 30 Problem: As of time 0, June and July LIBOR rates are unknown and random. Lec 6 Interest Rate Futures

For example, Assume LIBOR will evolve as follows: • ➁ 0.088 ➂ 0.094 ➀ $112,500 ➁ $122,500 ➂$130,000 • |–––––––––––––––|–––––––––––––––|––––––––––––––––| • 0 1 2 3 • Apr 30 May 30 Jun 30 July 30 • Under this scenario, interest payments will go UP • ➁ June 30 • At t=1 (Beginning of June) monthly LIBOR = 0.088/yr • Interest Pmt due June 30 = $15M*(0.088+0.01)/12 = $122,500 • ➂ July 30 • At t=2 (Beginning of July) monthly LIBOR = 0.094/yr • Interest Pmt due July 30 = $15M*(0.094+0.01)/12 = $130,000 • What to do? Set up a hedge strategy. How? Lec 6 Interest Rate Futures

Hedging Strategy for June: ▸ At t=0 (in April) Short 5 June futures @ IMM_L Index = 91.88 ➟ Forward Rate= (100-91.88)/100 = 8.12% ➟ Notional Value = $1M[ 1 - {0.0812/360} *90 ] = $979,700 ▸ May 30 buy back these 5 contracts.Suppose IMM_L Index = 91.12 ➟ Forward Rate=(100-91.12)/100 = 0.0888 ➟ Notional Value = $1M[ 1 - {0.0888/360} *90 ] = $977,800 Gain/Loss on 5 Futures = - 5(977,800 - $979,700) = + $9,500 Therefore, Unhedged Interest Pmt for June (paid June 30) = $15M*(0.0880+0.01)/12= $122,500 Hedged Interest Pmt = $122,500 - $9,500 = $113,000 ➟ Gains on short futures offset higher Interest Pmt. Lec 6 Interest Rate Futures

Hedging Strategy for July: ▸ At t=0 (in April) Short 5 September futures@ IMM_L Index = 91.44 ➟ Forward Rate= (100-91.44)/100 = 8.56% ➟ Notional Value = $1M[ 1 - {0.0856/360} *90 ] = $978,600 ▸ June 30 buy back these 5 contracts.Suppose IMM_L Index = 90.16 ➟ Forward Rate=(100-90.16)/100 = 0.0984 ➟ Notional Value = $1M[ 1 - {0.0894/360} *90 ] = $975,400 Gain/Loss on 5 Futures = - 5(975,400 - $978,600) = + $16,000 Therefore, Unhedged Interest Pmt for July (paid July 30) = $15M*(0.094+0.01)/12= $130,000 Hedged Interest Pmt = $130,000 - $16,000 = $114,000 ➟ Gains on short futures offset higher Interest Pmt. Lec 6 Interest Rate Futures

In sum: Q: in this example why short 5 contracts? Lec 6 Interest Rate Futures

Hedging Interest Rate Risk Def’n: Duration measures the sensitivity of the bond Price (B0) to changes in interest rates (Δy). This relationship applies to Bond futures also. ⇨ ΔF = - (DF x F0 ) x Δy To immunize a bond portfolio against changes in interest rates, Set ΔB + NF (ΔF) = 0 Lec 6 Interest Rate Futures

In our example, Interest rate changes monthly. ➟ Duration of the $15M bond (loan) =1/12 = 0.0833 years. Duration of the Futures Contract: 90/360 = 0.25 For June Hedge F0= Notional Value (as of April 30) = $979,700 ➟ ΔF = - (DF x F0 ) x Δy = - (0.25 x $979,700) x Δy ➟ ΔB = - (DB x B0 ) x Δy = - (0.0833 x $15M) x Δy Set NF such that [ Δ Bond Portfolio Value ] + NF (Δfutures) = 0 - (0.0833 x $15M) x Δy - NF (0.25 x $979,700) x Δy = 0 NF = - 5.1 Short 5 contract For July Hedge F0 = Notional Value (as of April 30) = $978,600 - (0.0833 x $15M) x Δy - NF (0.25 x $978,600) x Δy = 0 NF = - 5.1 Short 5 contract Lec 6 Interest Rate Futures

US Treasury Bonds : Spot (Cash) Market ▸ Prices in the spot market are quoted as 117-16 ➟ 117+16/32 = $117.50 (per $100 FV) ▸ Cash Price = Quoted Price + AI (seller wants cash for AI) Example: Spot Price is 117-16. CI = $5.50 (per $100) on Jan 10 and July 10 (181 days apart) if you buy this bond March 5, then Invoice Price =117.50+(5.50/181)*54 = $119.14 per $100 If you buy this bond June 30, and Spot Price is still 117-16 Invoice Price = 117.50+(5.50/181)*171 = $122,696 per $100,000 FV Lec 6 Interest Rate Futures

US Treasury Bond Futures Contract: U.S. T-Bond with 15 years to maturity, and 6% CI rate Exchange: CBOT Contract Size: $100,000 Face Value Delivery: Mar, Jun, Sep, Dec. Any day during delivery month Example: Go long one Dec T-Bond futures at 97-18, In English, I have agreed to: • Pay 97+18/32 = $97,562.50 for a U.S. T bond with $100,000 (FV), 15 yrs to maturity and 6% CI • Short will decide the actual delivery day in Dec and the actual bond to sell. Lec 6 Interest Rate Futures

Daily Mark to Market Lec 6 Interest Rate Futures

What Happens at Expiration? Close futures position before Dec 1. Buy Bonds in the spot market. OR (You may Skip the rest below) B. Buy T-Bond thru the futures. Then, Long must pay the following price: Invoice Price = Futures Price*Conversion Factor + AI Explanations: Suppose the last settle Futures price is 94-15. Then, the Futures Price = 94,468.75 Lec 6 Interest Rate Futures

What exactly is a Conversion Factor? Short must deliver bonds with $100,000(FV), 6% CI AND 15 yrs Time to maturity Most likely, Short cannot find one! What to do? Solution: CBOT allows delivery from a wide variety of US T-Bonds. Any coupon rate is okay. Only requirement: 15 or more YTM. For example, consider these two bonds (CI paid semiannually) Bond A: 6% CI (semiannual, FV = $100,000 and 15 YTM. (a long Futures position is the obligation to buy this bond) Bond B: 10% CI rate, FV = $100,000 and 20 years to maturity Lec 6 Interest Rate Futures

Assume a discount rate of 6%/yr. Then, PriceA = $3,000 [PVIFA, 0.06/2, 15yrs*2 ] + + $100,000[PVIF, 0.06/2, 15yrs*2 ] = $100,000 PriceB = $5,000 [ PVIFA, 0.06/2, 20yrs*2 ] + $100,000 [ PVIF, 0.06/2, 20yrs*2 ] =$146,230 Suppose Short wants to deliver Bond B. Should Long pay $100,000 or $146,230? Clearly, Long should pay $146,230 ➟ $146,230 = (same as) 1.4623 * $100,000 Lec 6 Interest Rate Futures

Definition of Conversion Factor Co Fac = {Value of deliverable bond priced to yield 6%} / {Value of underlying bond (Bond A) priced to yield 6%} = = 146,230/ 100,000 = 1.4623 NOTE: The Conversion Factor is just a mechanical formula. It converts a bond with any coupon and any Term to Maturity into Bond A, Assuming a YTM of 6%. Lec 6 Interest Rate Futures

One more complication: Cheapest to Deliver Bond At time of delivery, short has the option to deliver any long term bond. Example: Suppose 3 bonds are available Quoted (spot) Bond Bond Price Conversion Factor X $99.50 1.0382 Y $143.498 1.519 Z $119.75 1.2615 At delivery, to buy any bond in the spot market Short must pay: Invoice Price = Quoted Bond Price + AI To settle the futures, Short delivers this bond and receives: Invoice Price = Futures Price*Conv. Factor + AI Suppose the last Settle Futures Price = 94.46875. Then, the net CF for short is: Net CFX = - $99,500 + ($94,468.75*1.0382) = - $1,423 Net CFY = -$143,498 + ($94,468.75*1.5190) = $0 Net CFZ = -$119,750 + ($94,468.75*1.2615) = - $578 Short will buy and deliver $100,000 FV of bond Y Lec 6 Interest Rate Futures

Thank You (a Favara) Lec 6 Interest Rate Futures