Download

1 / 38

390 likes | 404 Views

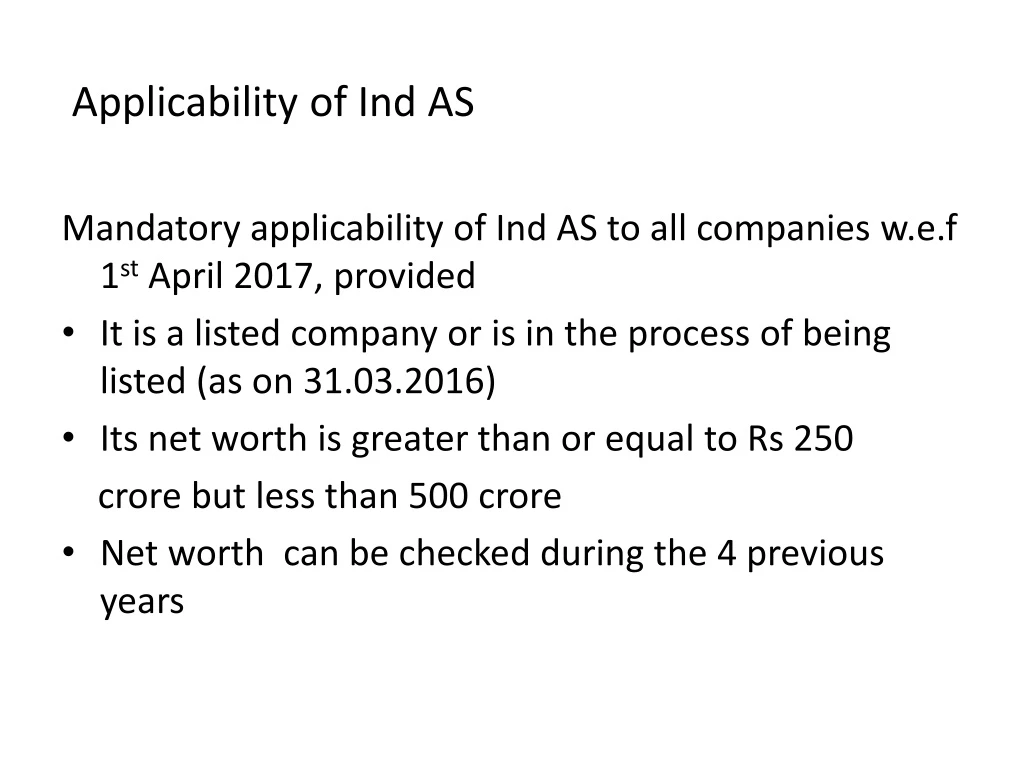

Applicability of Ind AS Mandatory applicability of Ind AS to all companies w.e.f 1 st April 2017, provided It is a listed company or is in the process of being listed (as on 31.03.2016) Its net worth is greater than or equal to Rs 250 crore but less than 500 crore

E N D

Applicability of Ind AS Mandatory applicability of Ind AS to all companies w.e.f 1st April 2017, provided • It is a listed company or is in the process of being listed (as on 31.03.2016) • Its net worth is greater than or equal to Rs 250 crore but less than 500 crore • Net worth can be checked during the 4 previous years

MCA notified following Ind AS to deal with accounting of financial instruments Ind AS 32 - Financial Instruments : Presentation Ind AS 109 - Financial Instruments Ind AS 107-Finacial instruments : Disclosures

Measurement of financial assets & financial liabilities Classificati on of financial assets & financial liabilities Classificati on of financial assets & financial liabilities Classificati on of financial assets & financial liabilities Classificati on of financial assets & financial liabilities Classificati on of financial assets & financial liabilities Classificati on of financial assets & financial liabilities IND AS 32 IND AS 109 IND AS 107 The trinity of financial instruments standards Classifi-cation as Liability v\s Equity offsetting Financial Asset& Financial liabity Recognition & de- recognition of financial assets & financial liabilities Classification of Financial Assets & Liabilites Measure- ment of financial Assets & Liabilities Hedge Accoun-ting Disclo-sures

Financial Asset Common Examples * Cash * Trade receivables * Investment in bonds and deposits * Investments in equity instruments * loans receivable ,etc.

Financial Liability Common Examples * Loans and borrowings * Payables for purchase of goods & services * Finance lease obligations * Redeemable instruments like preferences shares , debentures ,etc. * Guarantee given for repayment of debt upon borrower’s default

Equity * Equity instruments issued * Warrants to issue fixed number of shares at fixed price against each warrant * Others Instruments convertible into fixed number of equity Shares ,etc. also known as Derivaties Basis the above definition ,some of the key elements to understand * It includes currency and deposit of cash into bank/As it creates a contractual right to the depositor-medium of exchange Cash

Contractual right to receive cash or other financial asset Physical assets- plant and equipment leased assets intangible assets –Not financial Assets Prepaid expenses perpetual debt instruments are not financial assets

Contractual rights Examples * Trade receivables * Loans receivable * Deposits made; * Investment in bonds,etc. • A Contractual right or to satisfy a contractual obliagtions may be absolute or it may be contigent on occurrence of one or more future events ,not wholly within the control of either party to the contractual arrangements.A contingent rights and obligations meets the definition of financial asset and financial liabilities are not always recognized in the financial statements. For eg.: A lender may be recognized in the financial guarantee by a party (‘guarantor’) on behalf of borrower, entititling to recover the outstanding dues from the guarantor if the borrower were to default,etc.

WhatIs a Financial liability ? A financial liability is an liability that is : (a) A Contractual obligation : (i) To deliver cash or other financial asset to another entity ; or (ii) To exchange financial assets or financial liabilities with another entity under conditions that are potentially unfavourable to the entity ; Or (b) A contract that will or may be settled in entity’s own equity instruments and is : (i) A non derivative for which the entity is or may be obliged to deliver a variable number of entity’s own equity instruments ; or (ii) a derivative that will or may be settled other than by the exchange of a fixed amount of cash or another financial asset for a fixed number of the equity’s own equity instruments.

WHAT IS AN EQUITY INSTRUMENT ? - Per Ind AS 32.11 – An equity instrument is any contract that evidences a residual interest in the assets of an entity after deducting all of its liabilities. - Per Ind AS 32.16 - An instrument is an equity instrument if , and only if , both conditions (a) and (b) below we met: (a) The instrument includes no contractual obligation : (i) to deliver cash or another financial asset to another entity; or (ii) To exchange financial assets or financial liabilities with another entity under conditions that are potentially unfavourable to the issuer. (b) If the instrument will or may be settled in the issuer’s own equity instruments ,it is : (i) a non derivative that includes no contractual obligations for the issuer to deliver a variable number of its equity instruments ;or (ii) a derivative that will be settled only by the issuer exchanging a fixed amount of cash or another financial asset for a fixed number on its own equity instruments .for this purpose,rights,options or warrants to acquire a fixed number of the entity’s own equity instruments for a fixed amount of any currency are equity instruments if the entity offers the rights,

a fixed number of the entity’s own equity instruments for a fixed amount of any currency are equity instruments if the entity offers the rights, options or warrants pro rata to all of its existing owners of the same class of its own non –derivative equity instruments. Also , for these purposes the issuer’s own equity instruments do not include instruments that have all the features and meet the conditions described in paragraphs 16A and 16B or paragraphs 16C to 16D ,or Instruments that are contracts for the future receipts or delivery of the issuer’s own equity instruments. A contractual obligation , including one arising from a derivative financial instrument, that will or may result in the future receipt or delivery of the issuer’s own equity instruments , but does not meet conditions (a) and (b) above , is not an equity instrument.

Non derivative contract to deliver variable no . of equity shares Contractual obligation to deliver cash/financial asset Yes Yes No No Equity Liability Liability Equity Carried at ‘cost’ Fair Value Amortised cost Carried at ‘cost’ • Cost recorded in income statement • Impact on net profit/OCI All transactions recorded directly in equity

No Contractual obligation The Key Characteristics of an equity instrument have been further explained as follows: Equity instruments do not carry in the contractual obligations Puttable instruments are exception to this - If it gives rise to the company the right to buy back or redemption

Puttable instruments • Puttable instrument” is a financial instrument that gives the holder: • the right to put the instrument back to the issuer for cash or another • financial asset, OR • is automatically put back to the issuer on the occurrence of an uncertain • future event or the death or retirement of the instrument holder. • Phrase “put back to the issuer” = redemption of the instrument • For example - mutual funds and unit trusts, wherein the redemption amount is • equal to a proportionate share in the net assets of the entity Settlement in own equity instruments

Settlement in own equity instruments If equity carries an obligation for repayment in cash or other financial asset –Financial Liability Example : forward contract to buy back fixed number of own shares is financial liability

Ind AS 32 – objective, rationale and scope Objective: Lays down the principles for classification of financial instruments into equity, financial liability or both Scope : Only standard which deals with accounting for equity instruments Core principle : Emphasis on contractual rights and obligations arising from the terms of the instrument Probabilities of those contractual rights and obligations leading to an outflow of cash/ other resources are disregarded Key definitions : Equity instrument, financial liability and financial asset

Definition – Financial Instrument • Financial instrument is • any contract • that gives rise to • a financial asset of one entity and • a financial liability or equity instrument of another entity.

Equity • Any contract that evidences a residual interest in net assets of an entity • Examples • Ordinary shares • Share warrants • Mandatorily convertible preference shares in other words, contracts that are not liabilities

Definition – Financial Liability • Financial liability is • A contractual obligation • to deliver cash or other financial assets to another entity • to exchange financial assets/ liabilities under potentially unfavourable conditions; or • a contract that will or may be settled in the entity’s own equity instruments and is: • a non-derivative for which the entity is or may be obliged to deliver a variable number of • the entity’s own equity instruments; or • a derivative that will or may be settled other than by the exchange of a fixed amount of cash or another financial asset for a fixed number of the entity’s own equity instruments

Equity and liability classification • Financial instrument is an equity instrument only if both criteria are met: • There is no obligation to deliver cash or another financial asset or to exchange financial • assets or financial liability; and • The issuer will exchange fixed amount of cash or another financial asset for a fixed • number of its own equity instruments. Does the entity have an unavoidable contractual obligation? Equity Liability

Ind AS 32 - Equity or liability distinction Why does it matter? • Presentation in statement of financial position • Initial and subsequent measurement (scope of Ind AS 109) • Treatment of payments, • repurchases etc

Settlement in entity's own equity instruments • A contract is not an equity instrument solely because it may result in the receipt • or delivery of the entity's own equity instruments. • If an entity has: • a contractual right or obligation • to receive or deliver • a number of its own shares or other equity instruments • that varies • so that the fair value of the entity's own equity instruments to be received or • delivered equals • the amount of the contractual right or obligation • such a contract is a financial liability

Settlement in entity's own equity instruments “Fixed for fixed rule”

Obligation to deliver cash • Subject to certain exceptions, • if an entity does not have • an unconditional right • to avoid delivering cash or another financial asset • to settle a contractual obligation • the obligation meets the definition of a financial liability. • Lack of access to funds or the need to obtain approval for payment from a regulatory authority, does not negate the entity's contractual obligation or the holder's contractual right under the instrument and hence does not affect its classification

Examples – obligation to deliver cash • Type of instrument Liability Liability Equity • Non-redeemable shares with discretionary dividends YES ('ordinary shares') • Shares that are redeemable at the option of the holder YES ('puttable shares' ) • Shares that are redeemable at the option of the issuer YES ('callable shares') • Irredeemable preference shares with contractual dividends payable @4% p.a. • Redeemable shares with discretionary dividends ('ordinary shares')

UNIT 4: RECOGNITION AND DERECOGNITION OF FINANCIAL INSTRUMENTS yes Consolidate all subsidiaries (See note 1 below) Determine whether the derecognition principles are applied to a part or all of an asset(or group of similar assets) (see note 2 below) Have the rights to the cash flows from the asset expired? (see note 3 below) Derecognise

Obligations arising on liquidation • Certain instruments create an obligation only on liquidation of the entity • Liquidation may be certain to occur and outside issuer’s control or uncertain to occur and at the option of holder. • For example - Limited life entities like special purpose vehicles (SPV) for • execution of an infrastructure project • As per the ordinary definition of "financial liability", puttable instruments and instruments mentioned above shall always be classified as financial liabilities. But, there is an exception.

Issuer of a non-derivative financial instrument to evaluate the terms of the financial instrument to determine whether it contains both a liability and an equity component. If such components are identified, they must be accounted for separately as financial liabilities, financial assets or equity, and the liability and equity components are shown separately on the balance sheet.

Convertible Debt Convertible Debt Compound instruments – Separation + Liability :Fair value using rate for non-convertible debt Convertible Debt Equity: Balancing Figure

Of setting of Financial asset against financial liability is practical and can be done

Financial Assets measured at Amortised Cost Fair value through other Comprehensive income Fair Value through profit or loss If below conditions are met FA is held with BM whose objective is to hold financial assets in order to collect contractual cash flow FA are accounted at FVTPL if: (a) Any asset which is not measured at amortised cost and not measured at FVOCI ; or • FA shall be measured at FVOCI if below conditions are met • (a) FA is held with BM whose objective is achieved both by collecting contractual cash flows and selling FA • * Any equity instruments for which the entity makes an irrevocable elections to carry at fair value through OCI

'split accounting' 'split accounting' Liability component • Instrument whose terms indicate that it contains both a liability and an equity component Compound instruments ‘Split accounting’ Equity Component • must meet the definition of • equity • calculated as a residual

UNIT 4:RECOGNITION AND DERECOGNITION OF FINANCIAL INSTRUMENTS No Yes Consolidate all subsidiaries( see note 1 below) Determine the derecognition principles are applied to a part or all of an asset(or group of similar assets) (see note 2 below) Have the rights to the cash flows from the assets expired?(see note 3 below) Derecognise the assets

Has the entity transferred its right to receive cash flows?(see note 4 below) No Yes No No Yes Has the entity assumed a contractual obligation to pay the cash flows in an arrangement that needs 3 conditions?(see note 5 below) Continue to recognise the assets Has the entity substantially all risks and rewards?(see note 6 below) Derecognise the assets

Has the entity retained substantially all risks and rewards?(see note 6 below) Continue to recognise the asset No yes No No Has the entity retained control of the asset(see note 7 below) Derecognise the asset Continue to recognise the asset