Download

1 / 23

240 likes | 438 Views

ICFI. The Weighted Average Cost of Capital. By : Else Fernanda, SE.Ak., M.Sc. Valuation Method. Valuation Method. Market Comparable. Dividend Discount Model. DCF : Discounted Cash Flow Method. Other Method.

E N D

ICFI The Weighted Average Cost of Capital By : Else Fernanda, SE.Ak., M.Sc.

Valuation Method Valuation Method Market Comparable Dividend Discount Model DCF: Discounted Cash Flow Method Other Method • Comparing the firms with public company in the related industry, comparable size and relevant firms characteristic; • Examples: • PBV: Price to Book Value • EV/EBITDA: Enterprise value to EBITDA • PER: Price Earning Ratio • Discounting the future expected dividend; • Only recommended for company who has stable operation and stable dividend in the past history; • Most commonly used in corporate finance; • Based on comprehensive financial model; • Value is derived from future free cash flow... • ...discounted with cost of capital; • Value is very sensitive toward cost of capital & growth; • EVA: Economic Value Added. Used to be very popular in the 90s; • In principle, similar with DCF method;

Valuation Method Market Comparable Dividend Discount Model DCF: Discounted Cash Flow Method • See through the eyes of investors; • Simple and straight forwards; • Simple; • Detail and tailor-made; • Accommodate uniqueness, future strategy, and corporate action; Advantage • Can not be used if there is no comparable public companies; • Neglect firms uniqueness; • Oversimplify the real condition; • Only applicable for mature firm with stable income and operate under stable economic landscape; • Lengthy process; • Open ended bias.....wrong assumption on growth rate and discount factor; Drawback

Market Comparables PER • PER: Price Earning Ratio; • Very fluctuate, but easy to calculate and to understand; • Subject to financial engineering; Market comparable, normally only used for sanity check, to ensure if the valuation using DCF valuation is make sense or inline with market practice PBV • PBV: Price to Book Value; Very stable; • Less forward looking, doesn’t take into account future prospect; • Suitable for company who rely on assets as well as has less variability of profit margin in compare to peers in the sector; EV/EBITDA • EV/EBITDA: Ratio between Enterprise Value & EBITDA; • EBITDA is relatively difficult to manipulate; • Taking into account future prospect;

Market Comparable - Example Company D is excluded, since the number is so much difference with the others. It is an outlier. AVERAGE comes from A, B, and E only Value of XXX is: Rp 1,681 – Rp 2,196 bn Personally, I prefer to use EV/EBITDA • 1,681 = 3.36 x 500 • 1,838 = 6.13 x 300 • 2,196 = 2.20 x 1,000

Dividend Discount Model (DDM) • Valuing a firm, using dividend as free cash flow; • The drawback of DDM: (1) DPS is difficult to measure and tend to fluctuate; (2) Sensitive to Discount Rate; DDM DPS Value of Stock: -------- R - G DPS: Expected Dividend during next year; R: Required rate of return for equity investors; G: Growth rate in dividend forever; R: is equivalent with Re (Return on equity) Re = Rf + β(Rm – Rf) Rf = Risk free rate; β = Betha, slope between Rm and Re Rm = Return market

DDM: Multi Stages Mature & stable Transition Preliminary DPS Value 3 : ----------- (Re – G) D2n Value 2 : ------------ (1+Re2)n D1n Value 1 : ------------ (1+Re1)n

Dividend Discount Model (DDM) DDM • Valuing a firm, using dividend as free cash flow; • The drawback of DDM: (1) DPS is difficult to measure and tend to fluctuate; (2) Sensitive to Discount Rate; DPS Value of Stock: -------- R - G DPS: Expected Dividend during next year; R: Required rate of return for equity investors; G: Growth rate in dividend forever; R: is equivalent with Re (Return on equity) Re = Rf + β(Rm – Rf) Rf = Risk free rate; β = Betha, slope between Rm and Re Rm = Return market G: calculated as (1-DPR) x ROE DPR = Dividend Payout Ratio

Discounted Cash Flow (DCF) • Calculate Invested Capital (including debt); • Calculate Value Driver (revenue, cost, etc); Analyze historical Performance Forecast Performance • Understand strategic position, market share, cost composition; Calculate Free Cash Flow; • Check overal forecast reasonableness, using common size analysis; Estimate Cost of Capital (WACC) • Calculate cost of debt, cost of equity and WACC; • Be careful on debt to equity ratio...should be reasonable; Estimate Perpetual Value • Select appropriate technique and estimate horizon; • Discount perpetual value to present; Calculate and interpret Result • Run the calculation, double check if it is unreasonable; • Compare with market comparable valuation method;

Discounted Cash Flow (DCF) FCF1 FCF2 FCF3 FCF4 FCF5 FCF6 FCF7 FCF8 FCF9 FCF10 Perpetual Value or Terminal Value Present Value of FCF • Firm/Enterprise value is the accumulation of Present Value of Free Cash Flow (FCF) and Present Value of Perpetual Value; • Equity Value = Enterprise Value – Debt • Market Capitalization = Enterprise Value Present Value of Terminal Value Firm Value

Component of DCF Enterprise Value Financial Projection WACC Terminal Value • Create financial projection, could be full model or cash flow only; • Determine Free Cash Flow To Firm for the next 10 years (could be more or less); • Calculate WACC (Weighted Average Cost of Capital); • WACC is the discount rate to calculate Present Value of Free Cash Flow and Terminal Value • Calculate Terminal Value or Perpetual Value.... • ....using market comparable at year XX (say 10), or assuming the company operate perpetually; We have learned this

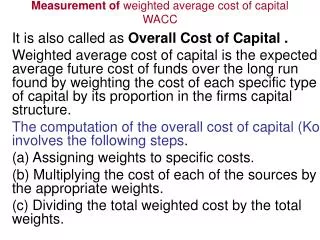

WACC: Cost of Financing & Risk Free WACC: • WACC: Weighted Average Cost of Capital; • Capital = Debt + Equity • Wd = proportion of debt = Debt / Total Capital • We = proportion of equity = Equity / Total Capital • Cost of Debt (Rd) = Interest Rate of the Debt x (1 – tax rate); • Cost of Equity (Re) = Rf + β (Rm – Rf) Cost of Debt • Debt is cheaper than equity. Rd < Re; • Why we should multiply Rd with (1- Tax Rate)?.... • .....because the interest we paid will reduce the taxable income (interest is part of non operating income).... • .....the higher the interest rate, the lower the tax we should pay; Risk Free Rate • Risk Free Rate: using SBI rate; • Current rate is around 6.5%;

WACC: Cost of Equity • Cost of Equity (Re) = Rf + β (Rm – Rf) • Rf = Risk free rate.....the return of risk free investment, such as government bond, SBI, etc; • Rm = Return market, in this case....we use IHSG return; • β is the association or slope of return between Rm and Re..... • ....pls refer to CAPM principle Cost of Equity Re β Re = Rf + β (Rm – Rf) 1 Rf Rm

WACC: Calculating ß Return: IHSG vs. Stock A β = 1.86 Re 1 Rm The slope between Rm and Re is 1.86. This slope is called Betha Usually, Betha is calculated using 3 years historical data;

WACC: Calculating WACC Re Rf β Rm Rf • Risk Free Rate; • Using SBI; • Around 6.4% • The slope between Rm & Re • Depend on industry or sector or companies; • For our discussion, we use 1.86 (see previous slides) • Market return; • The annual return of IHSG; • For this case we us 11.68% • Risk Free Rate; • Using SBI; • Around 6.4% 16.2% 6.4% 1.86 11.68% 6.4%

WACC: Calculating WACC Data • Cost of Equity = 16.2% (Re) • Cost of Debt = 12% (Rd) • Tax rate = 30% • Debt amount = Rp 400 bn; proportion = 40% (Wd) • Equity amount = Rp 600 bn; proportion = 60% (We) WACC: • WACC = We x Re + Wd x Rd x (1 – Tax) • WACC = 60% x 16.2% + 40% x 12% x (1 – 30%) • WACC = 9.7% + 3.4% • WACC = 13.1% • We use 13.1% as the discount factor

Free Cash Flow Free Cash Flow to Firm Free Cash Flow to Equity FCF To Firm = EBIT (1-Tax rate) + Depreciation – Capital Expenditure – Increase in inventory – Increase in receivable + Increase in payable FCF To Equity = Free Cash Flow To Firm – Interest (1 – Tax Rate) – Principal repaid + New Debt isssue – Preferred Dividend FCF To Equity = Net Income + Depreciation – Capital Expenditure – Increase in inventory – Increase in receivable + Increase in payable – Principal repayment + New Debt isssue – Preferred Dividend Present Value of (FCFF + Terminal Value) = EV Present Value of (FCFE + Terminal Value) = Equity Value Enterprise Value = Debt + Equity Value

Perpetual of Terminal Value • Perpetual Value or Terminal Value is the Value of Continuing Firm; • We assume that the firm will survive forever.... • ....or will be sold at a certain year (i.e. year 11) Definition • Free Cash Flow (year 11) • Perpetual Value (year 11) = --------------------------------- • (WACC – G) • G = Perpetual Growth = (1 – DPR) x ROE • DPR = Dividend Payout Ratio = Dividend / Net Income • ROE = Return on Equity = Net Income / Equity Calculation (1) • Assuming the company will be sold at year 11; • Perpetual Value = EBITDA x (EV/EBITDA) • EBITDA....use EBITDA at year 11; • EV/EBITDA.....use market comparable; Calculation (2)