Download

1 / 0

0 likes | 147 Views

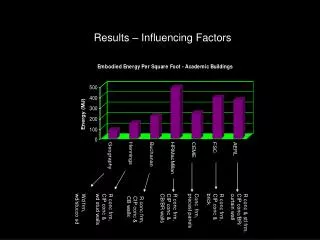

Factors influencing collegiate athletic department revenues. By: Chad D. McEvoy , Alan L. Morse, and Stephen L. Shapiro Presented by: Dion Doucet. NCAA Division 1 Revenue Generation. Median generated revenues increased about $13 million from 2004 – 2010

E N D