Download

1 / 5

50 likes | 54 Views

We are full service firm focuses in domain of Business Setup in India, FEMA, Expatriates Taxation, Accounting Outsource, International Taxation, Auditing, Transaction advisory and so on.<br><br>Underpinned by our values and with our global presence, we serve on FDI advisory, cross-border accounting, International tax planning and Management consulting needs of our overseas clients all over the world.

E N D

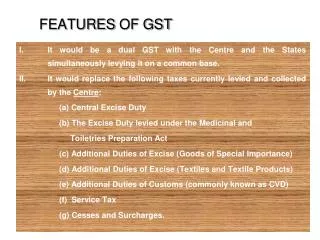

Clubbing of GST refund claims across two financial years is allowed

Circular for GST refund claims across two financial years • As per the recent circular, the amendment quoted reference from the M/S Pitambra Books Private Limited petition in Delhi High Court. M/S Pitambra Books Private Limited is one of our most valued clients. We are proud to say that our professional assistance and advice is something that has helped M/S Pitambra Books to file the Writ Application in Delhi Hight Court against the error in the circular restricting our client from claiming a GST refund.

1. Clubbing of GST refund claims across Financial Years is allowed • Refund process under GST has been clarified through Master Circular No. 125/44/2019-GST dated 19th November 2019 wherein earlier GST circular No. 37/11/2018-GST dated 15th March 2018 got subsumed. • In both circulars, the restriction was present on clubbing of tax period across financial years for claiming a refund. However, clubbing of tax periods in the same financial years was possible. • In the matter challenged before Hon’ble High Court of Delhi in case of our client M/s Pitambra Books Pvt Ltd., Hon’ble High court held that Circulars could supplant but not supplement the law. Circulars may mitigate harshness given in law and can grant reliefs beyond what is given in relevant statute. However, the Government has not got the empowerment to withdraw any benefits or impose any stricter conditions, which is not part of the law itself

2. No Refund of accumulated input tax credit (ITC) on account of the reduction in GST Rate • Issue about GST refund claims across two financial years: • Section 54(3)(ii) of the Central Goods and Service Tax Act, 2017 provides for a refund of ITC accumulated on account of inverted duty structure or inverted tax structure. • However, the Board has noticed that some of the applicants have claimed a refund of ITC accumulated due to the reduction of GST rates on the same goods under an inverted duty structure. E.g. a trader purchased good “X” attracting GST @ 18%. However, subsequently, the rate of GST on “X” reduced to 12%. In the given case, such a trader claimed a refund of ITC accumulated due to such reduction of rate under section 54(3)(ii) of the CGST Act, 2017.