Download

1 / 4

40 likes | 110 Views

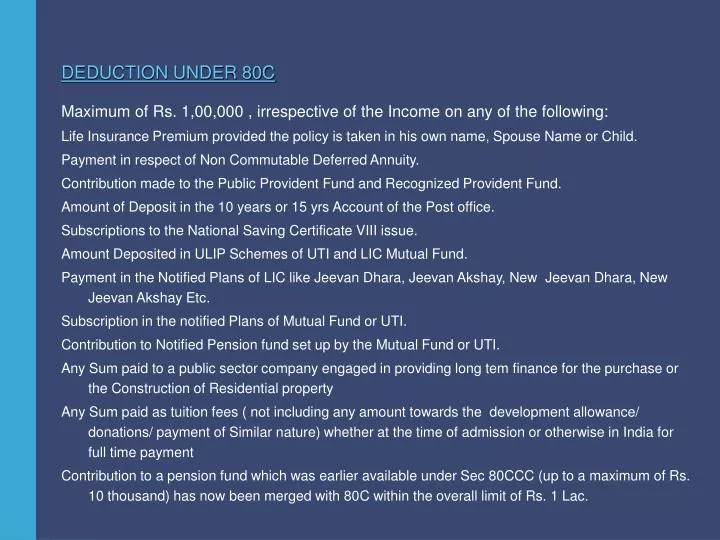

DEDUCTION UNDER 80C. Maximum of Rs. 1,00,000 , irrespective of the Income on any of the following: Life Insurance Premium provided the policy is taken in his own name, Spouse Name or Child. Payment in respect of Non Commutable Deferred Annuity.

E N D

DEDUCTION UNDER 80C Maximum of Rs. 1,00,000 , irrespective of the Income on any of the following: Life Insurance Premium provided the policy is taken in his own name, Spouse Name or Child. Payment in respect of Non Commutable Deferred Annuity. Contribution made to the Public Provident Fund and Recognized Provident Fund. Amount of Deposit in the 10 years or 15 yrs Account of the Post office. Subscriptions to the National Saving Certificate VIII issue. Amount Deposited in ULIP Schemes of UTI and LIC Mutual Fund. Payment in the Notified Plans of LIC like Jeevan Dhara, Jeevan Akshay, New Jeevan Dhara, New Jeevan Akshay Etc. Subscription in the notified Plans of Mutual Fund or UTI. Contribution to Notified Pension fund set up by the Mutual Fund or UTI. Any Sum paid to a public sector company engaged in providing long tem finance for the purchase or the Construction of Residential property Any Sum paid as tuition fees ( not including any amount towards the development allowance/ donations/ payment of Similar nature) whether at the time of admission or otherwise in India for full time payment Contribution to a pension fund which was earlier available under Sec 80CCC (up to a maximum of Rs. 10 thousand) has now been merged with 80C within the overall limit of Rs. 1 Lac.

POSITIVE CHANGE IN TAX RATES Up to Rs. 100,000 Nil Rs. 100,001 to Rs. 150,000 10.2% Rs. 150,001 to Rs. 250,000 20.4% Rs. 250,001 to Rs. 1,000,000 30.6% Above Rs. 1,000,000 33.66% * Income Slab Proposed effective rate (including surcharge and education cess) In case of a resident woman below the age of sixty five years, the basic exemption limit is increased to Rs. 125,000 In case of a resident individual of the age of sixty five years or above, the basic exemption limit is increased to Rs. 150,000/- Where the income exceeds Rs. 1,000,000, surcharge @10 per cent would be leviable on the total tax payable. * Marginal relief on the excess of income over Rs 1,000,000

DEDUCTION UNDER SECTION 80 L Financial Year 2004 -2005 Rs. 12,000 allowed as deduction under Sec 80 L on account of Interest income from specified securities, bank deposits, dividend from co-operative society etc. Additional amount of Rs. 3,000 available on the Interest form Government Securities. This Section is proposed to be withdrawn, the amount would be taxable under Maximum marginal Rate. Associates are requested to declare the Income from other sources so as avoid delays in the deposit of Tax and the Interest thereon.

OTHER IMPORTANT POINTS IMPACTING PERSOAL TAX • Additional Tax benefit (Rs. 5,000) previously available to the Females under Sec 88C is withdrawn. • Standard Deduction (maximum Rs. 30,000) Not Available • Limits on Surcharge Rates (@ 10%) now increased to Rs. 10 Lacs. • Deductions which were previously available to the Individual which have not changed in the budget proposals • Interest paid on housing loan for Self Occupied property. (Maximum amount allowable Rs. 1.5 lacs • Medical Insurance Premium under Sec 80D (Subject to a Maximum of Rs. 15,000) • Maintenance and Medical treatment of a handicapped dependent under Sec 80 DD. • Deduction for Medical treatment of self or dependent under Sec 80DDB. • Deduction to a person with Disability under Sec 80U.