Download

1 / 68

690 likes | 847 Views

Management Accounting: Information that Creates Value. Chapter 1. Introduction. Vincent Daniels, manager of the new retail outlet of Ikon Printing, wonders what financial and operating information he needs to manage the store. The store lines of business are: Printing Computing

E N D

Management Accounting:Information that Creates Value Chapter 1

Introduction • Vincent Daniels, manager of the new retail outlet of Ikon Printing, wonders what financial and operating information he needs to manage the store. • The store lines of business are: • Printing • Computing • Document preparation

Introduction • Fax services • Sales of office supplies • What information does Vincent need to improve processes? • Should he receive information about the quality and defects associated with each line of business? • This chapter will help you to…

Learning Objectives • Appreciate the important role that management accounting information plays in both manufacturing, service, non-profit, and governmental organizations. • Discuss the significant differences between management accounting and financial accounting.

Learning Objectives • Understand how different people in the organization have different demands for management accounting information. • Appreciate how management accounting creates value for organizations and how it relates to operations, marketing, and strategy.

Learning Objectives • Explain why management accounting information must include both financial and nonfinancial information. • Understand why activities should be the primary focus for measuring and managing performance in organizations. • Appreciate the behavioral and ethical issues faced by management accountants.

Learning Objective 1 Appreciate the important role that management accounting information plays in both manufacturing, service, non-profit, and governmental organizations.

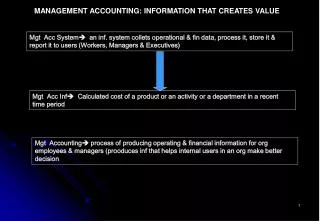

Management Accounting Information • What is management accounting information? • It is a value adding process of planning, designing, measuring, and operating nonfinancial and financial information systems that guides management action.

Management Accounting Information Operational and Financial Data Processing Actions

Management Accounting Information • What are some examples of management accounting information? • reported expenses of an operating department • calculated costs of producing a product • measurements of economic performance

Learning Objective 2 Discuss the significant differences between management accounting and financial accounting.

Financial Accounting • Financial accounting is constrained by mandated reporting requirements: • Financial Accounting Standards Board • Securities and Exchange Commission • International Accounting Standards Committee

Financial Accounting • Financial accounting provides information to external constituencies on past performance. Historically Oriented Rules Driven Objective and Aggregate Financial Measures

Management Accounting • Management accounting systems provide information to managers and employees within the organization. • Companies have discretion to design systems that provide information in order to make decisions about the organization’s financial, physical, and human resources.

Management Accounting • Management accounting provides information to internal constituencies. Current and Future Oriented No Regulations Subjective and Disaggregate Financial, Operational, and Physical Measures

Learning Objective 3 Understand how different people in the organization have different demands for management accounting information.

Diversity of Management Accounting Information • How does the demand for managerial accounting information vary among employees at different levels of the organization? • Operational level • Middle and upper management • Senior executives

Diversity of Management Accounting Information • At the operational level many repetitive activities are performed. • Management accountants develop information about the standards for labor time, machine time, and materials usage for repetitive tasks.

Diversity of Management Accounting Information • How much detail should be presented? • Disaggregate details • How frequent should information be provided? • Operational level information should be provided very frequently (usually daily).

Diversity of Management Accounting Information • What are the information needs of middle and upper management? • Middle and upper management need information to plan, supervise, and make decisions about financial and physical resources, products, services, and customers.

Diversity of Management Accounting Information • What type of information is used at the managerial level? • Resource utilization • Efficiency and quality of performance • Profitability

Diversity of Management Accounting Information • How much detail should be presented? • More aggregate than at the operational level. • How frequent should information be provided? • Managerial level information should be provided frequently (usually monthly).

Diversity of Management Accounting Information • What are the information needs of senior executives? • Senior executives need strategic information to assess overall performance, to monitor operating departments, and for benchmarking.

Diversity of Management Accounting Information • What type of information is used at the senior executives level? • Profitability • Customer loyalty and satisfaction • Market opportunities and threats • Technological innovations

Diversity of Management Accounting Information • How much detail should be presented? • More aggregate than at the managerial level. • How frequent should information be provided? • Executive level information should be provided less frequently than at the managerial level (annually or semi-annually).

Learning Objective 4 Appreciate how management accounting creates value for organizations and how it relates to operations, marketing, and strategy.

Functions of Management Accounting • What are the functions of management accounting information? • Operational control • Product costing • Customer costing • Management control

Functions of Management Accounting • What is operational control? • It provides feedback to employees and their managers about the efficiency of activities being performed. • What is product costing? • It measures and assigns the costs of the activities performed to design and produce individual products and/or services.

Functions of Management Accounting • What is customer costing? • It is assigning marketing, selling, distribution, and administrative costs to individual customers so that the cost of serving each customer can be calculated. • What is management control? • It is providing information about the performance of managers.

Origins of Management Control • Many innovations in management accounting systems occurred in the early decades of the 20th century. • Senior executives at DuPont Corporation devised techniques to develop operating budgets and capital budgets. • Donaldson Brown, the CFO of DuPont, developed the return on investment performance measure.

Origins of Management Control • The return on investment calculation gave DuPont executives a single number to evaluate the performance of their operating divisions. • Profitability Measure • Return on Sale = Operating Income ÷ Sales • Asset or Capital Utilization Measure • Sales ÷ Investment

Origins of Management Control • Return on Investment • ROI = Operating Income ÷ Investment • The senior managers at DuPont used the ROI measure to help them decide which of their divisions should receive additional capital to expand capacity.

Origins of Management Control • Around 1920, Brown left DuPont to become CFO for General Motors under its chief executive officer, Alfred Sloan. • General Motors introduced many management accounting initiatives to accomplish the company’s operating philosophy of “centralized control with decentralized responsibility”.

Origins of Management Control • Corporate managers received periodic financial information about divisional operations and profitability. • The General Motor’s management accounting system enabled the organization to plan, coordinate, control, and evaluate the operations of multiple operating divisions.

Origins of Management Control • Sloan’s and Brown’s initiative played a critical role during the 1920 to 1970 time period. • However, during the past few decades, demands by external constituents led many organizations to place more emphasis on external reporting.

Origins of Management Control • Management accounting information stagnated and proved inadequate for the changing and challenging competitive, technological, and market conditions of the late 20th century.

Learning Objective 5 Explain why management accounting information must include both financial and nonfinancial information.

Management Accounting in Service organizations • The major changes in the demand for management accounting information experienced by manufacturing companies in recent years have also occurred in service organizations.

Management Accounting in Service organizations Characteristics of Service Organizations Provide a service, no product More direct contact with customers No inventory, per se Quality hard to control in advance

Management Accounting in Service organizations • Management accounting systems in most service organizations allowed managers to budget expenses by operating department and to measure and monitor actual spending against these functional departmental budgets.

Changing Competitive Environment • During the last quarter of the 20th century, the competitive environment for both manufacturing and service companies has become more challenging. • Today’s companies demand different and better management accounting information.

Changing Competitive Environment • Starting in the mid 1970s, manufacturing companies encountered severe competition from foreign companies that offered higher-quality products at lower prices. • A company could prosper only if its cost, quality, and product capabilities were as good as those of the best companies in the world.

Changing Competitive Environment • Companies will need both financial and nonfinancial information to succeed. • The deregulation movement since the 1970’s also changed the ground rules under which many service companies operated. • Managers of service companies now require accurate, timely information to improve the quality, timeliness, and efficiency of the activities they perform.

Government and Non-Profit Organizations • Government and non-profit organizations are feeling the pressures for improved performance. • In 1990, the U.S. Congress passed the Chief Financial Officers Act. • This act requires each major federal agency to have a CFO responsible for developing and reporting cost information.

Government and Non-Profit Organizations • It also requires the systematic measurement of performance. • The Government Performance and Results Act of 1993 (GPRA) requires that each federal agency: • establish top-level agency goals and objectives and annual program goals. • define how it intends to achieve those goals.

Government and Non-Profit Organizations • demonstrate how it will measure agency and program performance in achieving those goals. • Also, in 1993, Vice President Al Gore recommended an action to require the Federal Accounting Standards Advisory Board (FASAB) to issue a set of cost accounting standards for all federal activities.

Government and Non-Profit Organizations • In 1995, the FASB issued a document of “Managerial Cost Accounting and Standards for the Federal Government”. • This document specified that in managing federal programs cost information is essential in five areas:

Government and Non-Profit Organizations • Budgeting and cost control • Performance measurement • Determining reimbursements and setting fees and prices • Program evaluations • Making economic choice decisions

Government and Non-Profit Organizations • Demand for cost information in government will be essentially identical to those in for-profit manufacturing and service companies. • Managers of non-profit organizations of all types are looking to adapt management accounting procedures in order to satisfy the demands on them for accountability and performance measurement.

Learning Objective 6 Understand why activities should be the primary focus for measuring and managing performance in organizations.