Download

1 / 18

190 likes | 301 Views

A Survey on Portfolio Optimisation with Metaheuristics. Prisadarng Skolpadungket Keshav Dahal School of Informatics University of Bradford, UK. Outline. Introduction. Portfolio Optimisation Problems. Realistic Constraints Metaheuristic Methods and Results

E N D

A Survey on Portfolio Optimisation with Metaheuristics Prisadarng Skolpadungket Keshav Dahal School of Informatics University of Bradford, UK

Outline • Introduction. • Portfolio Optimisation Problems. • Realistic Constraints • Metaheuristic Methods and Results • Conclusion and Future works

Introduction • Portfolio optimisation objective: to find minimum risk a given expect return . • A portfolio manager task: to select K assets from a universe of N assets (K <= N) (e.g. all listed companies’ stocks) to form an equity portfolio. • 2 relevant characteristics of any assets • 1) Expected return • 2) Risk profile. • Risk is a relatively vague concept thus can be quantitatively represented by many definitions.

Introduction (Cont.) • The most popular representations of risk • Variance of return (or Standard Deviation) • Value at Risk (VaR). • Variance and VaR of a portfolio not equal to plain summation of the assets’ returns • Assets’ returns may be correlated thus portfolio’s return less than the plain summation. • The more un-correlated, the less risk the portfolio. • The choices of assets in combination affect • weight average expected return • non-linear and inter-related risk

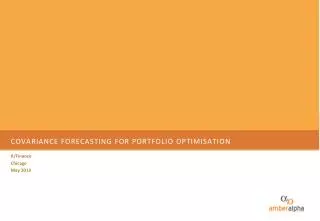

Portfolio Optimisation Problems The general model of portfolio optimisation (modified Markowitz model by Black) is • xi are selection variables, short-sale allowed. • xi can be negative (short position of asset i). • If xi are all continuous and differentiable then the model has • a closed form solution (solved by standard calculus). • a Portfolio Frontier represents the set of portfolio optima .

Portfolio Frontier rp (Return) r (Return)

Portfolio Optimisation Problems (Cont.) • The original Markowitz model has no short-sell • xi cannot be negative. • Non-negative constraint is added into the general model • This model cannot be solved by calculus. • But by some specialised techniques • e.g. interior point algorithms, branch and cut approaches, other numerical techniques using structures of the co-variance matrix.

Realistic Constraints • Realistic constraints arise • Regulations • Market institution • investment policies • economic (cost) reasons etc. • Integer constraints: every asset includes in the portfolio must be rounded normal trading lot). • Cardinality constraints: the maximum number and minimum number of assets to include in the portfolio

Realistic Constraints (Cont.) • Floor and ceiling constraints: lower and upper limits on the proportion of each asset held. • Turnover constraints: upper bound for variations of the asset holding from one period to the next. • Trading constraints: limits on buying and selling tiny quantities of assets • Transaction costs: associate with purchases and sales of assets incorporated in the realistic models.

Metaheuristic Methods and Results • With realistic constraints: • Portfolio optimisation became Non-Polynomial Hard problems (NP-Hard). • Integer and cardinality constraints: • The problems become combinatorial optimisation problems with factorial time complexity (O (C (N, k)) ). • Two ways to cope with the NP hard problems. • Approximate Models • Approximate Algorithms • Heuristics are Approximate Algorithms. • Simple heuristics: tend to end their searches in local minima. • Metaheuristics: • Heuristics with mechanisms to escape local minima. • Allowing temporary moves to inferior points. • Two categories of Metaheuristics: • Local search metaheuristics (LSMs) • Evolutionary algorithms (EAs).

Simulated Annealing • The oldest among the metaheuristics. • Allowing moves toward worse solutions to escape from local optima. • The probability of worse moves diminishs like molecules slowing down as the temperature cooling down. • Crama and Schyns (Crama 2003) • With floor, ceiling, turnover, trading and cardinality constraints. • Approximated the optimal portfolio frontier (medium size problem with 151 assets) within acceptable time. • Could handle more classes of constraints than classical approaches. • Versatile to apply to different measures of risk. • Needs to customize and fine tune parameters for different classes of constraints.

Tabu List X X X X X X X X X • Tabu Search • Keeps lists of previous searches (tabu list) • Forbids moves toward tabu list. • Used to avoid local optima • To implement an explorative search strategy (Blum 2003.) • Busetti (Busetti 2000) • Used Tabu Search/Scatter Search • Compared with Genetic Algorithms (GA) • Found that tabu/scatter search is unsuitable for cardinality constraint problem (40 assets) • Concluded that GA is better than tabu/scatter search

Ant Colony Search • Imitation ants’ findind shortest path between food sources and their nest. • Ants deposit pheromone on the ground. • Decide the direction based on the concentration of pheromone. • Maringer (Maringer 2005) applied ant colony algorithms for small portfolios (with cardinality constraints). • Similar to Knapsack problems with some modifications. • The “value” of asset depends on the overall structure of portfolio. • Has to decide jointly • to include an asset or not • the amount of the asset. • Found that AC is more efficient for smaller K (=3) and with pheromone evaporation

Hybrid Local Search • Maringer (Maringer 2003, 2005) • Applied hybrid local search. • Combine population based with local search. • A crystal-like structure represents a portfolio of assets. • All of the crystals represent the population. • The iterations consist of three stages; • Modification of crystal (portfolio) structure • Evaluation and ranking of the modified structure • Replacement of the poorest crystal in the population. • Test the algorithm against SA and SA with a group of isolated crystals (GSA). • Results: • HLS (best) >> GSA >> SA (worst) • Conclusion: • Evolutionary strategies improve metaheuristic algorithms for portfolio optimisation

Genetic Algorithms • GA are population based heuristic algorithms • Imitating the natural selection of survival of the fittest. • Represented as chromosomes • breed by crossover • modified by mutation • Busetti (Busetti 2000) compared GA with tabu search • Found that GA performs better. • Streichart et al. (Streichart 2004a) applied the Multi-Objective Evolutionary Algorithm (MOEA) • Use 2 binary bit-string based genotypes • Gray-code encoding • Real-valued genotype (32 bits) • Compare: • GA with and without Lamarckism (can be modified not only being removed from the population) • Knapsack GA (KGA) with and without Larmarckism. • With constraints: cardinality and integer (discrete) constraints

Genetic Algorithms (Cont.) • The reults: • with constraints, KGA produced better results and converged faster than ordinary GA. • without constraints, both GA and KGA perform almost the same. • GAs without Larmarckism tend to be premature convergence and trapped in local minima. • The real value coding performed worst • Bit gray-coding and Larmarckism was the best • Intrepretations: • The mutation and crossover operators are more effective in the gray code representation. • Larmarckism adds performance due to its ability to remove neutrality in the search space.

Conclusion Future Works • A portfolio optimisation with realistic constraints is a NP hard problem. • Pure search metaheuristics tends to be trapped in local optima. • Population based metaheuristics tends to be time inefficient. • Uses of hybrid algorithms can improve the situations. • A clear trend is heading toward hybrid models. • Our future work will be toward improving hybrid and novel metaheuristic implementations. • We also plan to extend the techniques to implement on other portfolio selection models with • Different definition of risk and return, • Estimations of the volatility and of the returns.

The End Thank You !